The quiet half of the infrastructure trade

When investors think about infrastructure, they usually think about the building of it – the cranes, the ribbon cuttings, the multi-billion-dollar contracts to construct new highways, fibre networks, and water treatment plants.

What is often overlooked is the quieter, less glamorous component: maintenance. Someone has to inspect the pipes, fix the leaks, upgrade the substations and respond when a storm takes down a network. None of it is headline-grabbing. All of it keeps the country running.

Service Stream (ASX: SSM) is one of Australia’s largest essential network services companies, delivering operations and maintenance work across telecommunications, utilities, transport, and (as of February 2026) defence.

We have owned Service Stream at various points of different cycles. Today, Service Stream is in an absolute sweet spot. It has significant earnings upside over the next three years, a valuation that does not appropriately reflect this, and, on top of this, a net cash balance sheet that gives it optionality to take acquisition opportunities that arise.

Not just another ‘bad contractor’

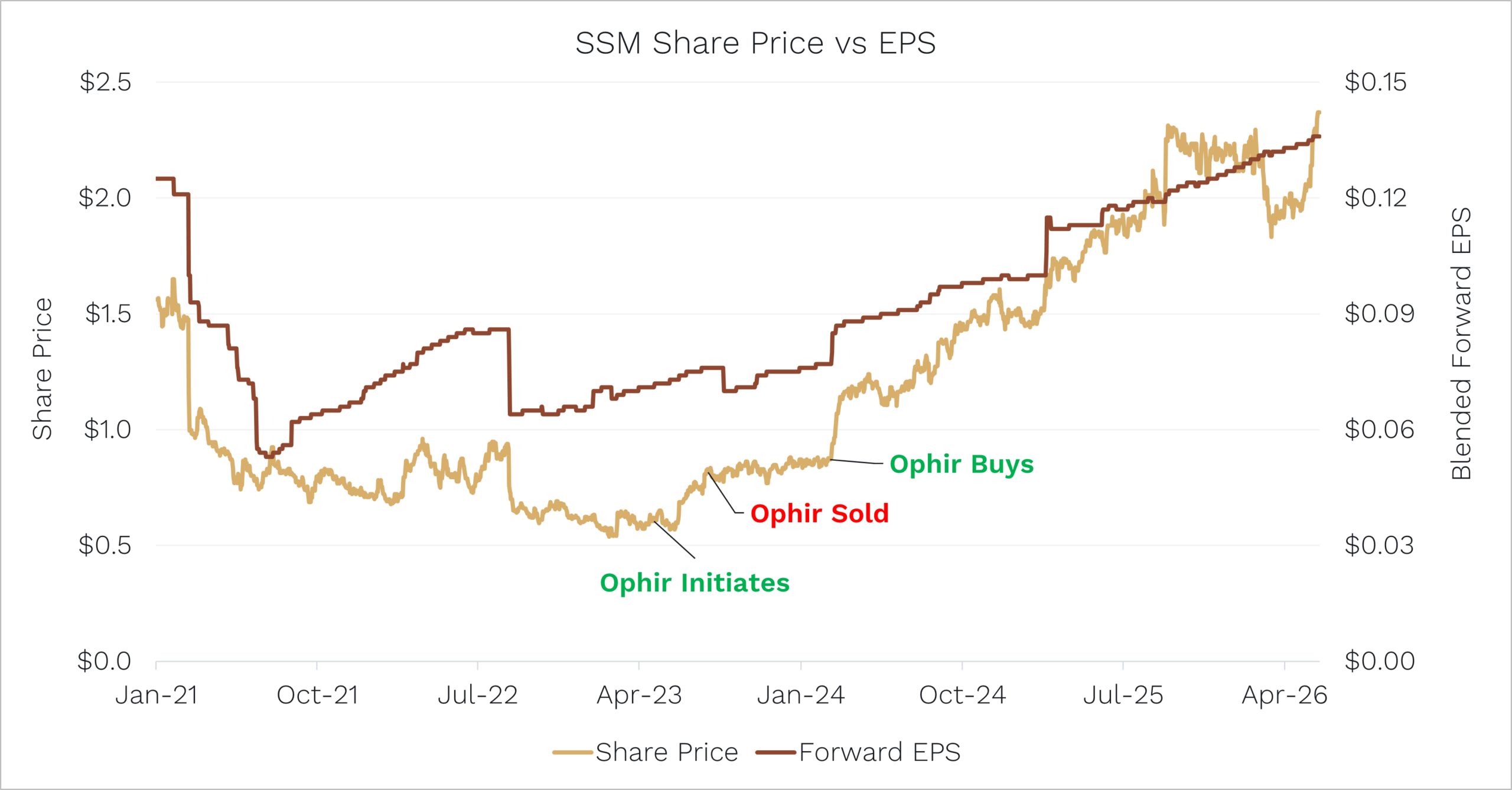

We initially bought into Service Stream in 2023. At the time, the company had taken on several utilities contracts that were poorly priced and poorly risk-managed. Margins collapsed, the stock derated heavily, and the market wrote the business off as a typical ‘bad contractor’ story.

Source: Ophir, Bloomberg. Data as at 31 May 2026.

However, we could see the opposite was true. The contracts in question were finite. The management team had evolved. Pricing discipline was being restored. And the underlying franchise, multi-year operations and maintenance (O&M) contracts with blue-chip utilities and telcos, was inherently a high-quality annuity business once the legacy issues were worked through.

The share price has obviously increased a long way since then. But we believe the market is still underestimating the upside of the company.

There are three reasons we have been adding to the position over the past year, and all point to the same thing: earnings upside.

-

The utilities margin recovery has further to run

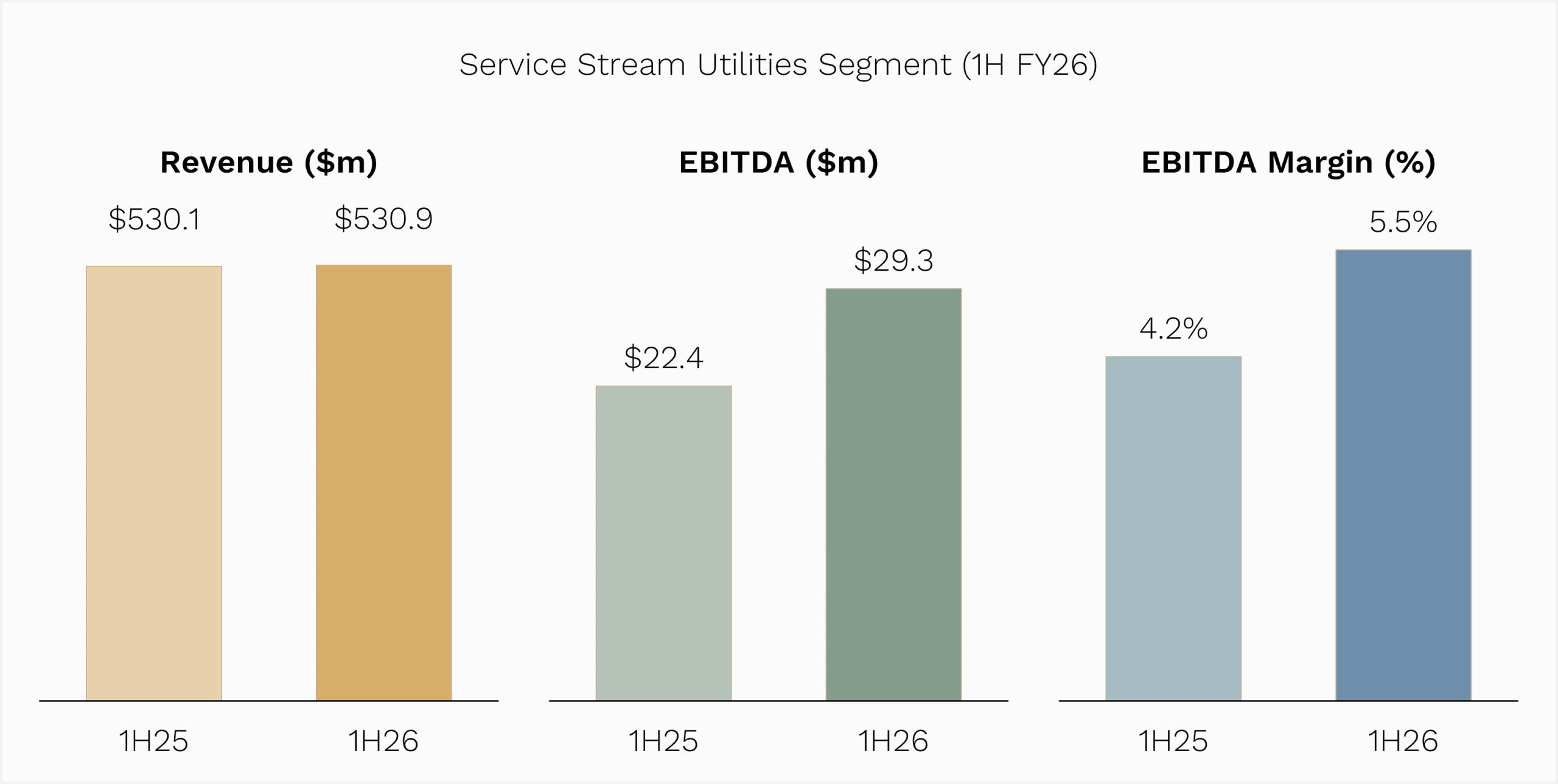

Service Stream’s utilities division was the heart of the original problem back in 2022. Over the past 24 months, the team has methodically restructured pricing, exited unprofitable scopes, and rebuilt the discipline around contract risk.

The result is now becoming visible in the numbers. The 1H26 result showed a step-change in utility EBITDA margins to 5.5%, up 130 basis points on the prior corresponding period and ahead of the segment repositioning target of 5.0%. Management has indicated that it is targeting further incremental margin expansion.

We think this is achievable. The company is now in a position to selectively pursue minor capital works at higher margins, and the broader contracting environment is supportive. As a result, utilities can continue to grow organically at high single digits, with EBITDA margins expanding towards 6.5% over the next two years.

Source: Service Stream FY26 Half Year Results Presentation.

-

Defence is a genuine step-change in the addressable market

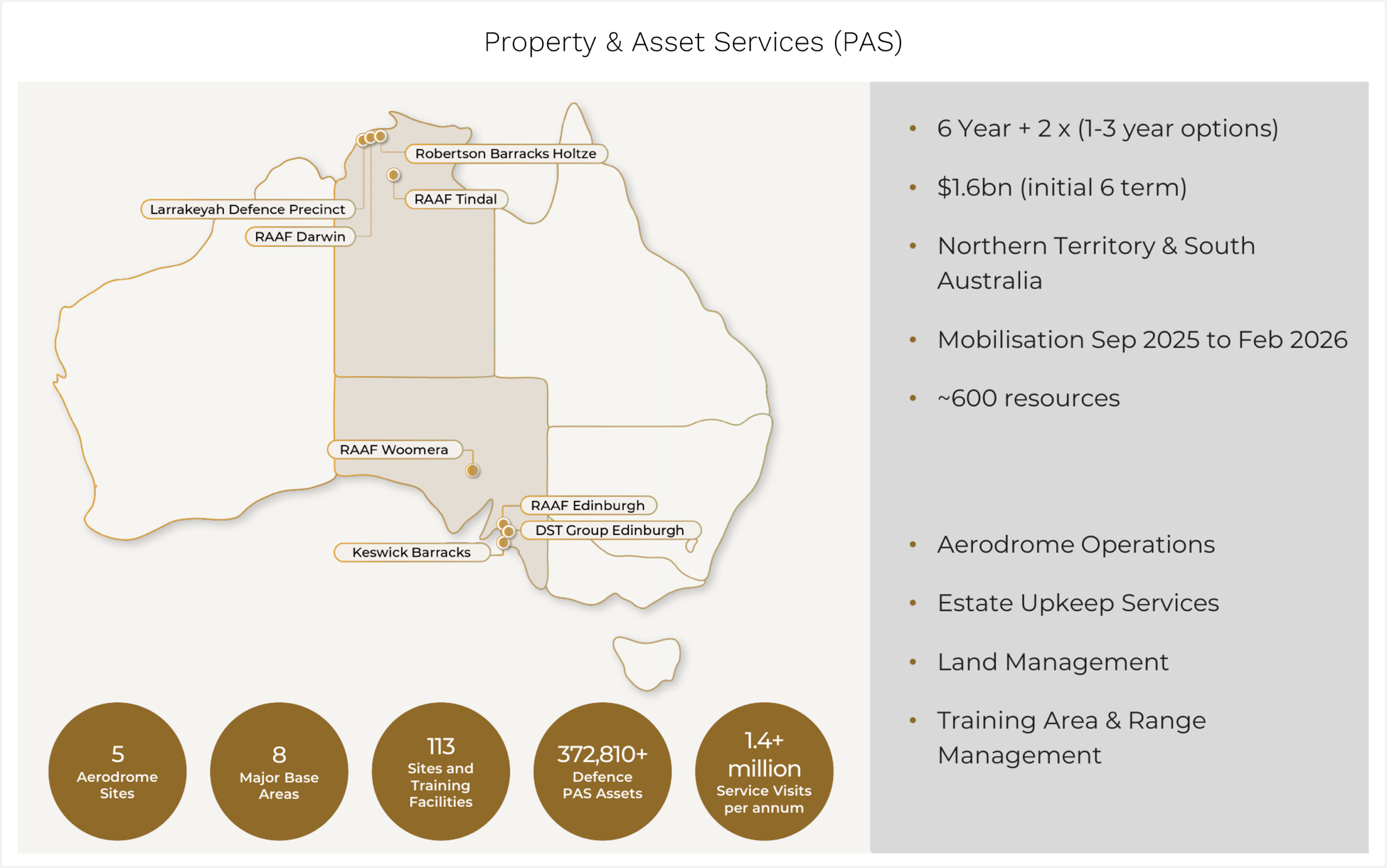

In FY26, Service Stream achieved a long-term strategic objective when it was appointed as a Tier 1 Defence contractor. The win was a six-year Property & Asset Services agreement with the Department of Defence covering the Northern Territory and South Australia, with two 1- to 3-year extension options. Initial contract value is $1.6 billion over the first six years.

Source: Service Stream FY26 Half Year Results Presentation.

This is genuinely significant for two reasons. First, it represents a major expansion of the Group’s addressable market – Defence facilities maintenance has historically been a duopoly dominated by Ventia and Downer. Service Stream is now part of that conversation. Second, the contract mobilised on 1 February 2026 and is expected to contribute meaningfully to earnings from FY27 onwards.

The market is currently using a ~5% margin assumption for this work, which we think is conservative. In time, the team will scale, optimise operations, and start winning the minor capital works that typically accompany the incumbent facilities maintenance contractor. We believe Defence could generate over $250 million of annual revenue for Service Stream at margins north of 5%.

Source: Service Stream FY26 Half Year Results Presentation.

-

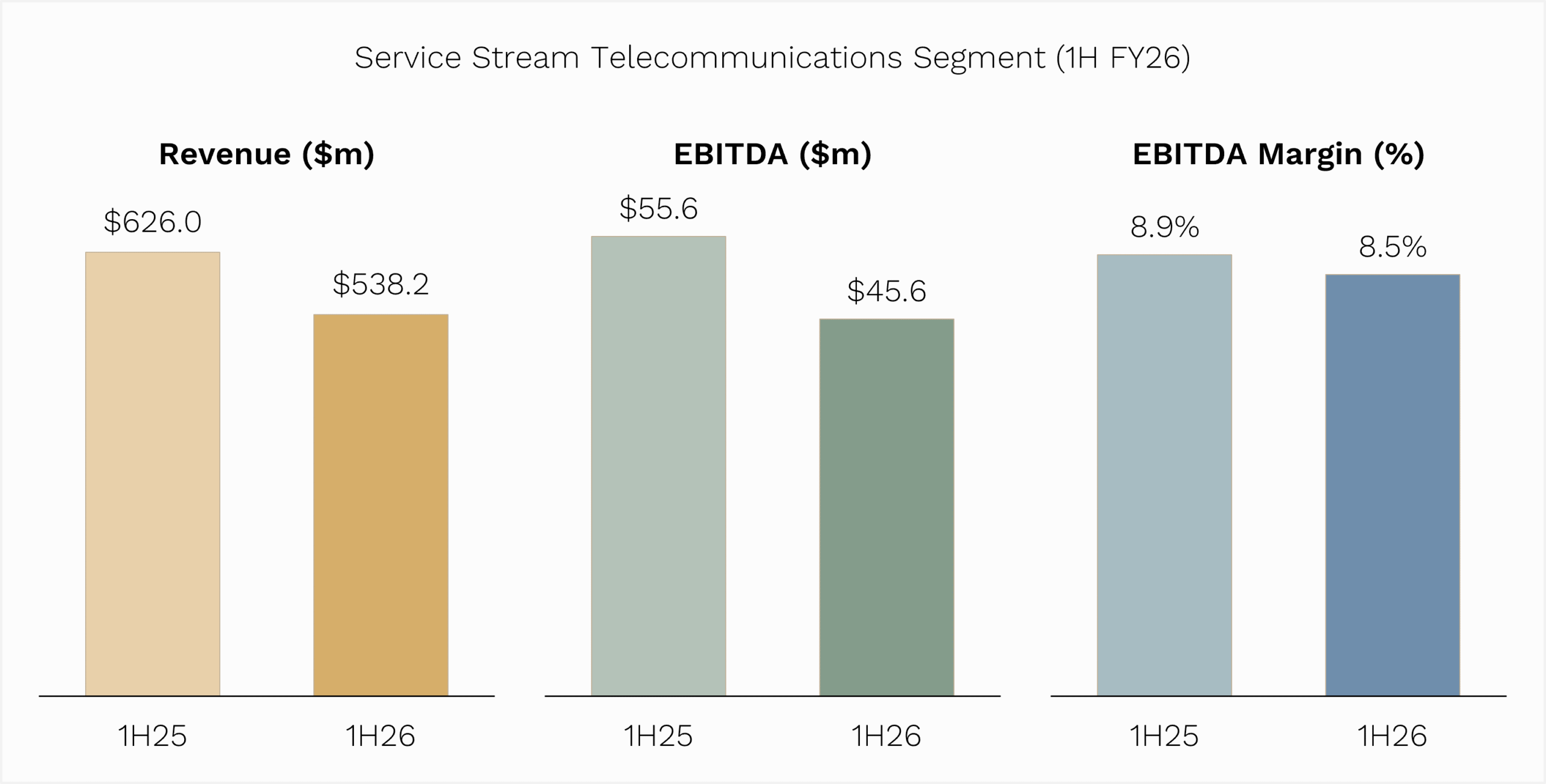

Telecommunications remains a steady earner with embedded growth

The telco segment has cycled off a strong period (the 1H25 comparable was inflated by programs that have since rolled off), but the underlying franchise is in good shape. Most notably, Service Stream has:

- Successfully transitioned to a new NBN Field Services contract with exclusive coverage of VIC, SA, WA & NT.

- Commenced initial mobilisation on the new NBN fibre upgrade in QLD, NSW and ACT.

- Signed a new five-year strategic partnership with Telstra.

- Secured a new program supporting Optus HFC decommissioning.

These are all multi-year, annuity-style contracts that underpin the segment for the next 3-5 years. We believe Service Stream’s telco segment can grow revenue 3-5% next year at margins of around 9%.

Source: Service Stream FY26 Half Year Results Presentation.

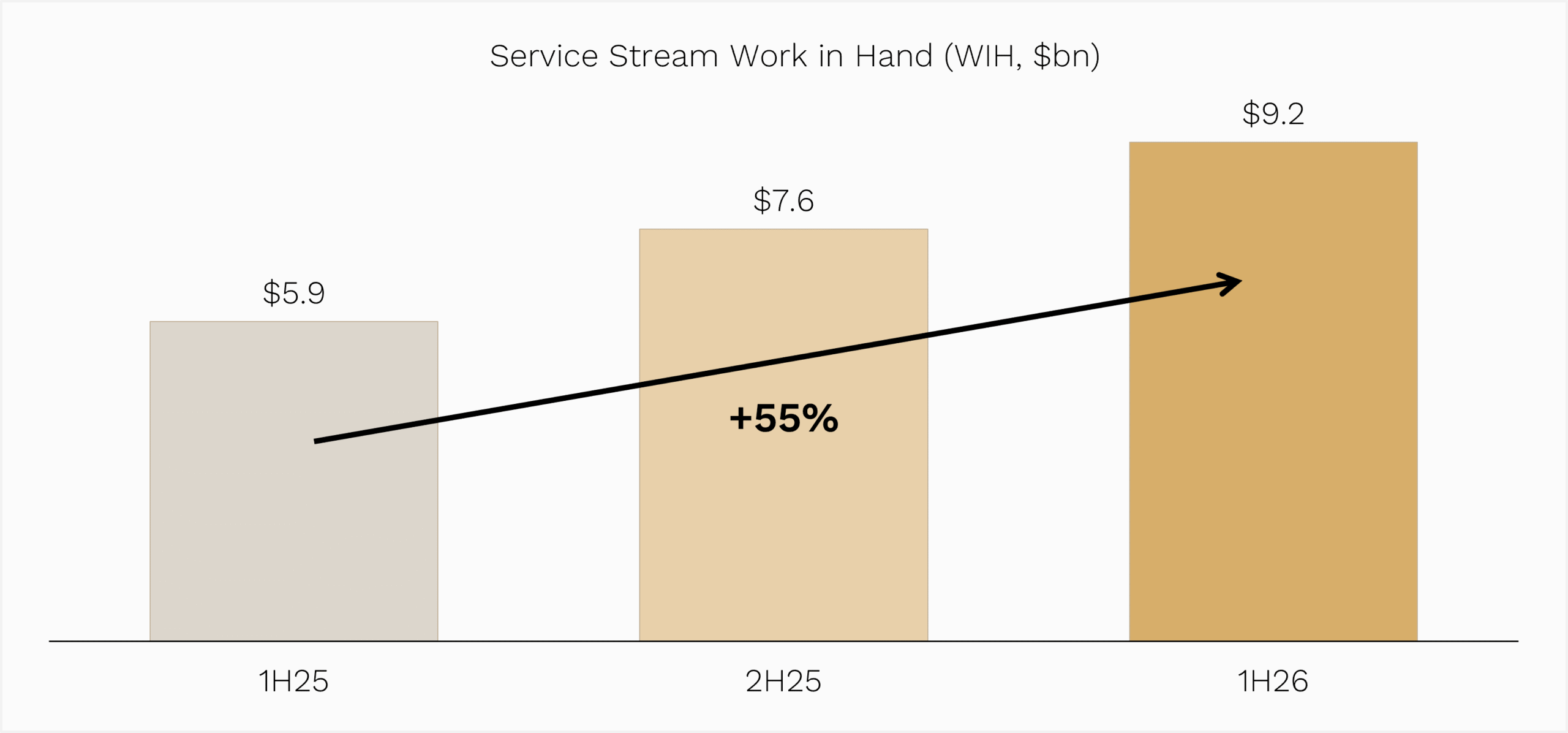

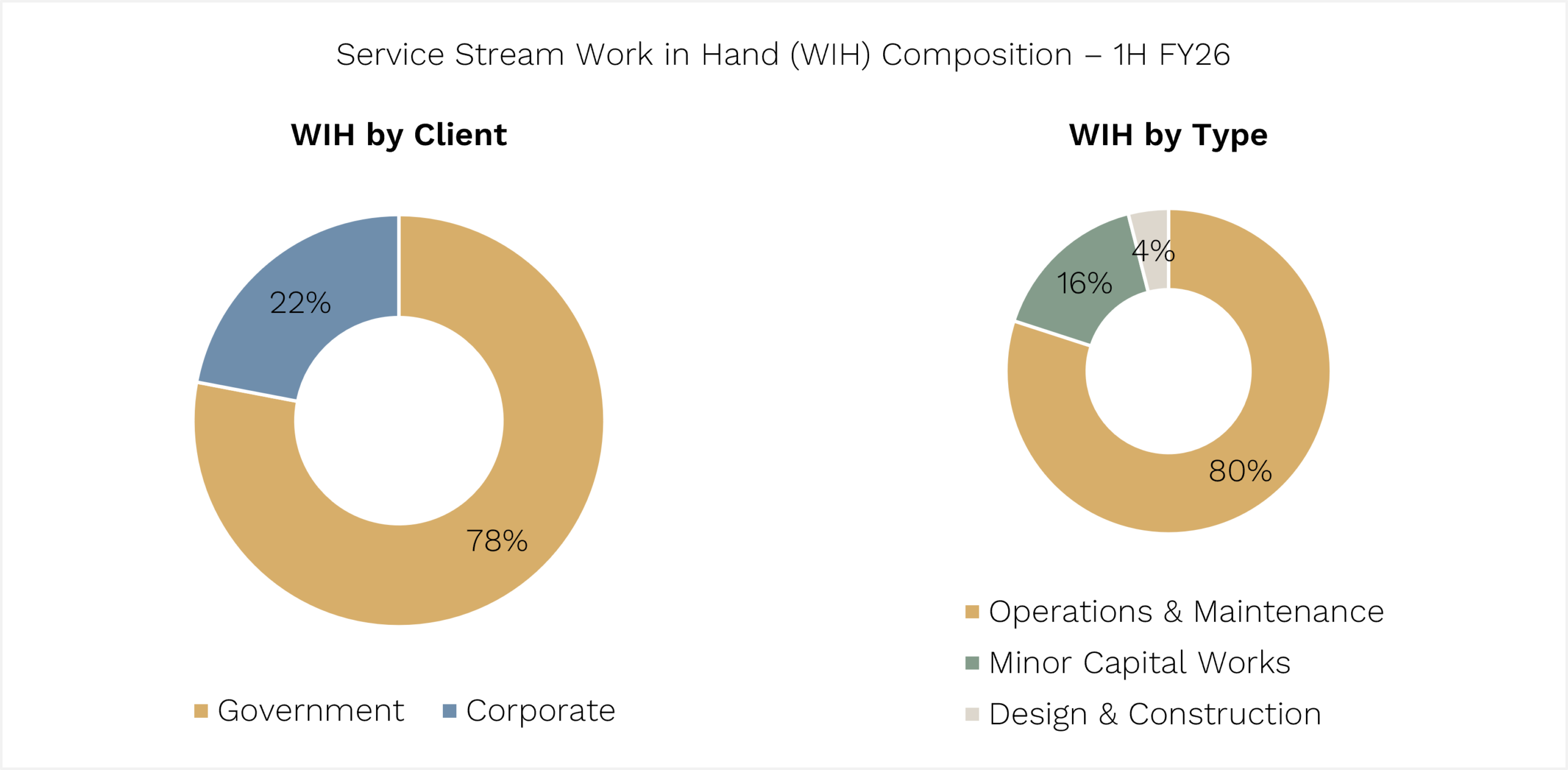

A hidden order book

What gives us particular confidence in the company’s earnings trajectory is the rate at which Service Stream has been securing new work.

In 1H26 alone, the company secured $2.2 billion of new multi-year operations and maintenance (O&M) agreements and strategically renewed 93% of existing contracts that proceeded to market. Total Work in Hand (WIH) has grown 55% on the prior corresponding period to $9.2 billion, with an additional $6 billion in extension options on top.

Source: Service Stream FY26 Half Year Results Presentation.

Average contract tenure is now 17.5 years.

Since the 1H result, Service Stream has continued to add to that order book. Recent announcements include:

- A nine-year, $405 million contract with Yarra Valley Water under its Maintenance Services Delivery Partners program (mobilisation October 2026),

- Two contracts with Millmerran Operating Company at its Queensland power station worth a combined ~$50 million over three years.

These wins illustrate exactly what a diversification strategy is designed to deliver: more water, more industrial, more power.

In a contractor, Work in Hand growth of this magnitude doesn’t show up in the P&L immediately. It shows up over the following 2-3 years as new contracts mobilise and existing ones extend at improved margins.

Source: Service Stream FY26 Half Year Results Presentation.

The market is treating Service Stream’s headline FY26 numbers (revenue down 5.8% on previous corresponding period due to the 1H25 telco skew) without giving credit for the order book that sits behind them.

Optionality on top

Management has indicated they continue to actively assess M&A opportunities to expand service offerings, capabilities, and addressable markets.

Past acquisitions have focused on quality and have been bedded down well. With ~$100 million of net cash expected to be available outside of leases by FY27, a sensibly priced bolt-on at ~8x EV/EBIT would add another ~9% to earnings on top of the organic upgrade we already see.

The offshore lens

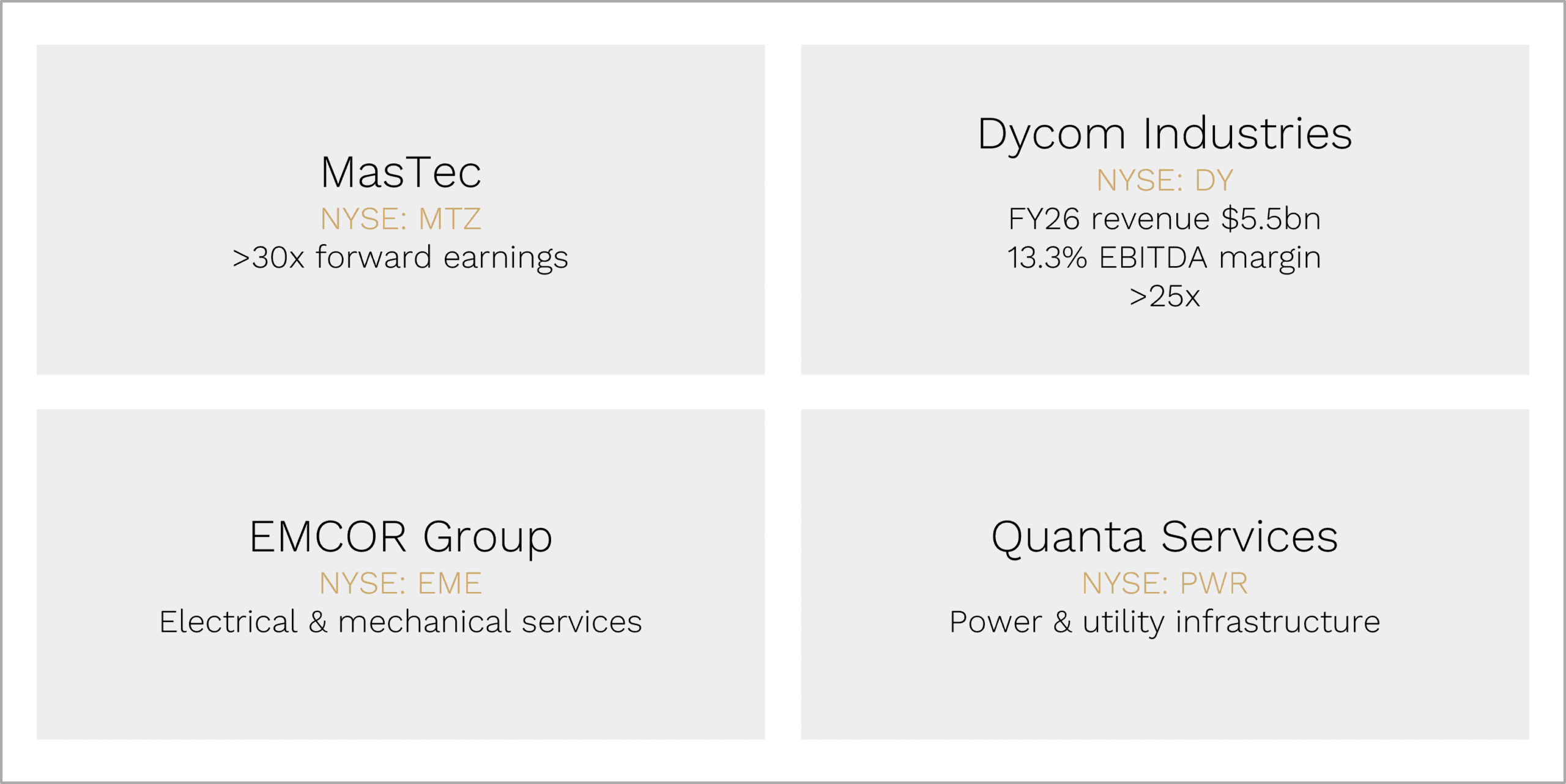

It is worth stepping back and putting Service Stream in the context of its global peers, because the Australian market does not always price contractors the way the US market does.

In the US, the listed network and infrastructure services contractors – Dycom Industries (NYSE: DY), MasTec (NYSE: MTZ), EMCOR (NYSE: EME), and Quanta Services (NYSE: PWR) – trade on materially higher multiples than their Australian counterparts.

Dycom, for example, has just reported FY26 revenue of US$5.5 billion at 13.3% adjusted EBITDA margins, with a backlog of more than US$8 billion, and trades on more than 25x forward earnings. MasTec sits even higher at around 35x.

Source: Ophir, Bloomberg.

The drivers are not identical to Service Stream, US peers benefit more directly from fibre-to-the-home buildouts, data centre construction, and the AI-driven power infrastructure cycle. But the structural features investors are paying premium multiples for, long-dated O&M contracts with blue-chip customers, recurring revenue, net cash balance sheets, and operating leverage from incremental volume, are exactly the features Service Stream now has. And who knows … maybe data centres are next for Service Stream!

The US private market reinforces the point. ITG Communications, a private US network services provider, has been on an aggressive acquisition spree (Quasar in December 2025, Advantage Utilities in November 2025, and others), backed by global alternatives firm Oaktree Capital. Private capital is paying up to consolidate this category, even as Australian listed peers in the same category trade at material discounts to global comps.

Looking ahead: arguably a higher-quality earnings stream

Service Stream’s management has guided earnings growth in FY26, with a traditional 2H bias driven by the mobilisation and scaling of new operations including Defence.

We believe consensus FY27 EBITDA of ~$180 million is too low. We see upside risk to earnings as utilities margins continue to expand, telco grows modestly, and Defence begins to contribute meaningfully.

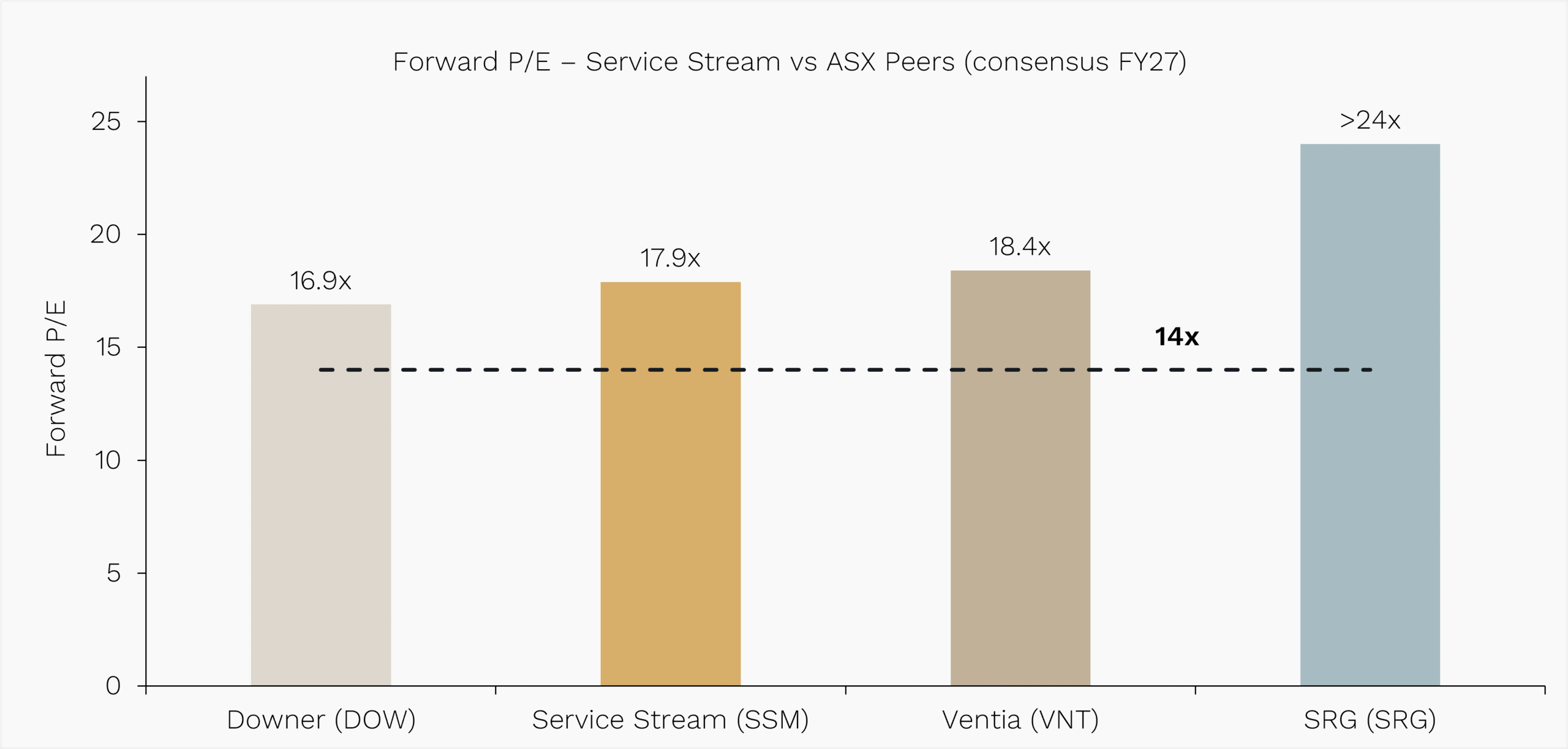

Service Stream is currently trading on around 18x consensus FY27 earnings, which, given our earnings expectations, is overstated and should be closer to ~14x.

For reference, Ventia trades on ~18x, Downer on ~17x, and smaller specialist contractor SRG well above 24x. It could be argued that Service Stream has a higher-quality earnings stream than some of these. More annuity, less Design & Construct, with a net cash balance sheet and clearer earnings upgrades ahead.

Source: Ophir, Bloomberg.

Why it fits this environment

In a market consumed by the AI debate, where every software business is being asked whether its cash flows are durable at all, Service Stream is the other side of the coin.

Its earnings are tied to ageing infrastructure that has to be maintained, telecommunications networks that have to be operated, water assets that have to keep flowing, and defence sites that have to stay functional. None of this changes if AI model capability doubles next year. None of it changes if the macro slows. The work simply has to happen.

It is, in short, the kind of compounder that doesn’t need a benign macro to work. It just needs the infrastructure of modern Australia to keep running – and that, increasingly, runs through Service Stream.