Your Distribution Guide – the decision that compounds.

PDF | OPH ASX Announcement

At Ophir, we seek to compound investor capital.

Over the long run, we’ve done exactly that, returning (as at 31 May 2026):

- +23.0% p.a. in the Ophir Opportunities Fund (since August 2012)

- +12.1% per annum in the Ophir High Conviction Fund (since August 2015)

- +18.7% per annum in the Ophir Global Opportunities Fund (since October 2018)

- +14.3% per annum in the Ophir Global High Conviction Fund (since September 2020)

all net of fees and assuming reinvestment of distributions. Past performance is not a reliable indicator of future performance.

Under Australian managed-fund rules, we’re required to pass through net realised gains and income to unitholders each year.

Some years that means a meaningful distribution, some a modest one, and occasionally none at all. When there is one though, the mechanics can confuse some investors. The choice of what to do with the cash is often one of the most consequential investment decisions they’ll make all year.

This piece covers three things:

- How a distribution actually works: what you’ll see, and why.

- The cost of taking cash: the long-term impact on your investment.

- The practical bits: FY26 distribution estimates for the Ophir Funds, key payment and statement dates, and what to do before 1 July.

What is a distribution, exactly

A distribution is your share of the year’s profits: the income and realised gains your fund has earned, paid out in proportion to how many units you hold. For our funds, that typically includes:

- Dividends from the companies we own

- Interest on any cash holdings

- Net realised capital gains from holdings we’ve sold during the year

That last one is what swings most year to year. Some years we crystallise a lot of gains, some years we don’t, and some years prior-year losses are still absorbing gains before they reach you.

Why your unit price falls on 30 June

In the weeks after a distribution, like clockwork, we get an influx of concerned investors asking what on earth happened to the fund in June for the unit price to drop. And the reassuring answer is usually, nothing! We just paid you a distribution.

Imagine your unit price starts FY26 at $2.50, and through the year the fund earns $0.50 per unit that must be distributed. That money doesn’t sit in a separate pot; it increases your unit price over the year. By 30 June 2026, the unit price is $3.00: your original $2.50, plus the $0.50 waiting to be paid out. On 30 June, that $0.50 gets paid out as a cash distribution, and the unit price retreats to $2.50, exactly where it started.

Look at the price alone and you’d swear you made nothing all year, a 0% price return. But the $0.50 is in your pocket. Add it back and your total return is 20% ($0.50 ÷ $2.50). Note: generally it’s not 100% of any rise in the unit price throughout the year that is paid out as a distribution – we have just simplified the example here.

But, this is where the jargon trips people up. That $3.00 is the cum-price, the unit with the income still inside it. The $2.50 is the ex-price, after the cash has been handed out. The gap between them isn’t a loss. It’s your distribution.

The price didn’t fall. It just stopped carrying cash that’s now yours.

The cost of cash

Everyone loves a Brucey bonus. There’s something satisfying about seeing cash hit the bank from an investment, and to be clear, it’s your real profit from the stocks we hold.

The only question is: what taking it as cash costs you, compared to leaving it in the fund.

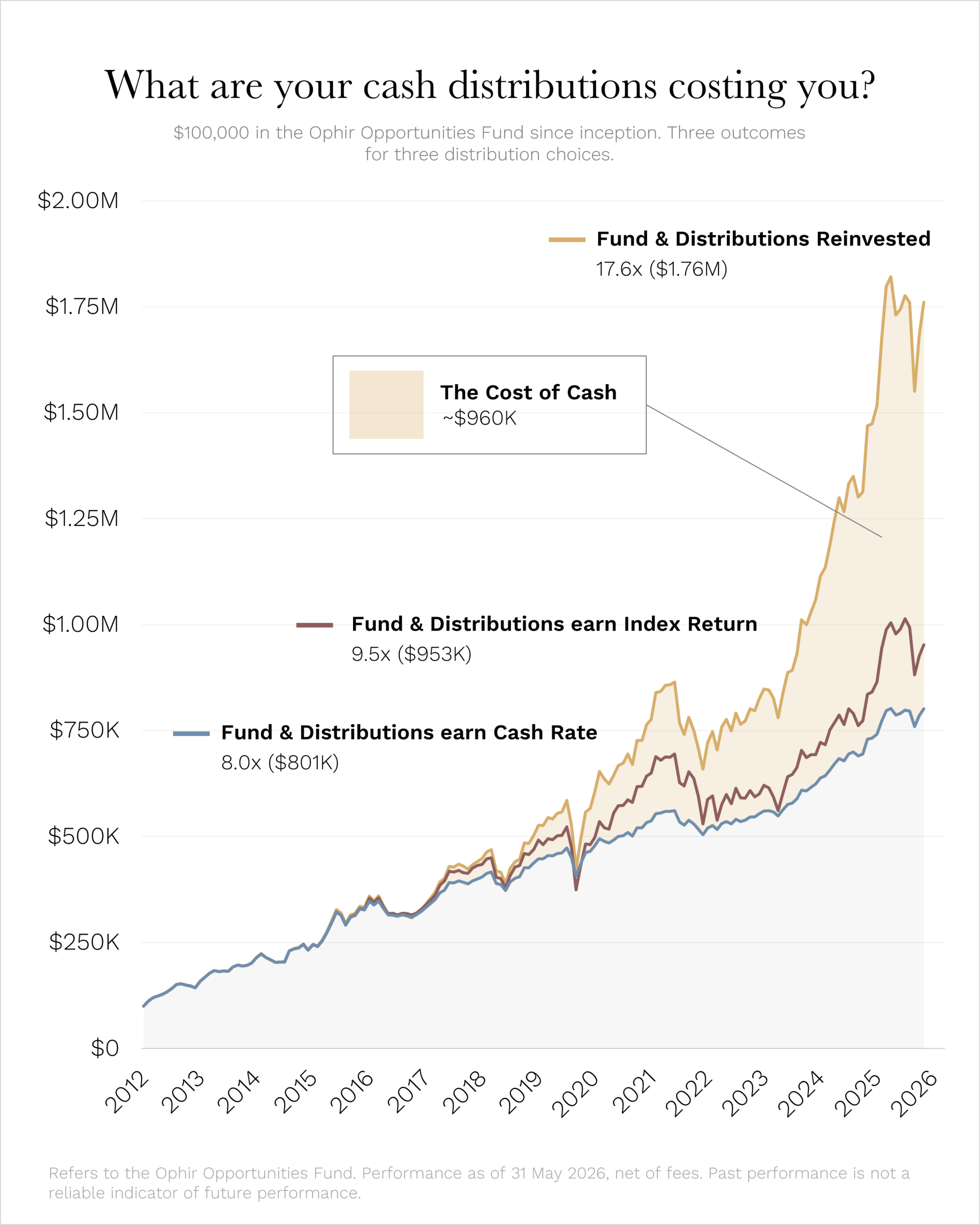

Here’s the answer in dollars. Put $100,000 into the Ophir Opportunities Fund at inception in August 2012. The chart below shows what you’d have as at 31 May 2026: the value of your holding, plus whatever you did with each distribution along the way.

Source: Ophir, Bloomberg. Note: Index refers to ASX Small Ordinaries Index Total Return.

Tick the DRP box at inception and your $100,000 is worth $1.76 million today (after fees and before tax). Take every distribution as cash and let it sit earning the cash rate, and you have $801,000. That’s around $960,000 difference.

But what if you’d got around to reinvesting it yourself, putting every cash distribution into the Australian small cap index along the way? You’d have $953,000. Better, but still over $800,000 short of the DRP investor.

Both numbers tell the same story, and it isn’t about the index, the cash rate, or the maths. It’s that cash rarely gets a plan. The first distribution lands, you ponder what to do with it, you sit on your hands waiting to “buy the dip”, while the market it came from has continued compounding without it.

These figures are illustrative only, based on the fund’s actual past returns and a calculated cash rate over the period shown. Outcomes will depend on how distributions are used. Holding cash or reinvesting into different assets may lead to different results. Past performance is not a reliable indicator of future performance.

Don’t Retire your Profits (DRP)

But officially? The Distribution Reinvestment Plan.

The case for reinvesting is the oldest one in investing: compounding. As Warren Buffett put it, “Life is like a snowball. The important thing is finding wet snow and a really long hill.”

The DRP hands you both. The wet snow is a fund with strong long-term returns. The long hill is the time horizon that lets compounding do its work.

Here’s how it rolls. Reinvest your distribution and you receive new units, issued at the ex-price, with no transaction costs. Those units earn next year’s distribution, which buys more units, which earn the year after. Each year your slice gets a little bigger. Gentle at first, quietly remarkable by year ten, genuinely transformative by year twenty (based on the historical returns).

That’s the snowball. The DRP is how you keep it rolling.

Four things to know about the DRP

- Free: No transaction costs or buy/sell spreads.

- Flexible: Reinvest fully, partially, or not at all. Change your mind any time.

- Tax-neutral. Same tax either way. Your distribution is assessable in the year it’s earned regardless of whether you take cash or reinvest. Reinvesting doesn’t defer or reduce the tax.

- Set-and-forget. Elect once. It runs in the background until you stop it.

The DRP isn’t for everyone. If you rely on your distribution for income, take the cash. But if you don’t need the cash right now and you’re investing for the long term, reinvestment is the simplest decision you can make to compound your position.

Based on their own circumstances, the investors in our funds who’ve quietly reinvested for the last decade didn’t make a difficult decision once. They made an easy decision once and left the snowball alone.

The above is general information only, not personal financial advice. Market conditions, cash flow needs and tax outcomes may affect long-term results, and outcomes are not guaranteed. Consider seeking licensed financial or tax advice for your circumstances.

FY26 distribution estimates

Below are our estimated distributions per unit (DPU) for each fund and unit class, based on portfolio data as at 30 April 2026:

| Fund |

Class |

Estimated DPU |

| Ophir Opportunities Fund |

Ordinary Class |

$0.7587 |

| Ophir High Conviction Fund (ASX: OPH) |

Ordinary Class |

$0.3517 |

| Ophir Global Opportunities Fund |

Class A |

$0.1379 |

| Ophir Global Opportunities Fund |

Class B |

$0.0580 |

| Ophir Global Opportunities Fund |

Class H (Hedged) |

$0.1350 |

| Ophir Global High Conviction Fund |

Class A |

$0.00 |

| Ophir Global High Conviction Fund |

Class B |

$0.00 |

Please note: for all Ophir funds, the ex-distribution date is 30 June 2026, and the record date is 1 July 2026.

Estimates only, based on portfolio data as at 30 April 2026. Final distributions are calculated after 30 June 2026 and may differ materially. Do not rely on these figures for tax purposes.

Why OPH works differently

The Ophir High Conviction Fund (OPH) is our listed investment trust (LIT), so its Distribution Reinvestment Plan works differently to our unlisted funds.

In the unlisted funds, your reinvested distribution simply becomes new units, created at the ex-price. Because OPH units trade on the ASX, our current DRP policy is to use your distribution to buy OPH units on-market through our broker, rather than issuing new units. In plain terms, an on-market buyback.

That’s good news for you. The buyback can never pay more than the end of financial year reported NAV per unit, and when OPH trades at a discount, as it does today, you pay less.

Note: because the buyback takes time to complete and settle, OPH’s distribution and tax statements arrive a few weeks later than the unlisted funds, typically mid-to-late August. For more details please refer to the ASX announcement (link) and the terms and conditions of the DRP (link here).

A note for Global High Conviction Fund holders

Our Global High Conviction Fund (Class A and Class B units), based on current estimates, may not pay a distribution this year.

The fund had built up carry-forward losses from prior years. This financial year to date, the fund has produced strong returns, and those carry-forward losses have done exactly what they’re designed to do: absorb the realised gains the fund made so far during FY26. The capital losses have been fully recouped, and the remaining gains have been offset by some leftover carried-forward revenue losses.

Based on current estimates, the expected outcome is a $0 distribution, with the value the fund has generated staying in your unit price rather than being paid out.

If that estimate holds, GHCF holders won’t receive a distribution statement or an AMMA tax statement (the document you’d normally use at tax time) for FY26.

Your 30 June statement will arrive later

Because the final ex-distribution unit price can’t be confirmed until after the distribution is calculated and audited, your 30 June 2026 holding statement arrives once everything is finalised. It comes bundled with your distribution and AMMA tax statements: late July to early August for the unlisted funds, and the second half of August for OPH.

| Fund |

Distribution Payment |

June Holding Statement |

Distribution Statement |

AMMA Tax Statement |

| Ophir Opportunities Fund |

Fri 24 Jul |

Fri 24 Jul |

Fri 24 Jul |

Mon 3 Aug |

| Ophir Global Opportunities Fund |

Wed 22 Jul |

Wed 22 Jul |

Wed 22 Jul |

Wed 29 Jul |

| Ophir Global High Conviction Fund |

N/A |

Thu 23 Jul |

N/A |

N/A |

| Ophir High Conviction Fund (OPH) |

Mon 17 Aug |

Mon 17 Aug |

Mon 17 Aug |

Mon 24 Aug |

Dates are estimates only. All statements will be sent via our unit registry Automic Group and will be made available in the Automic Investor Portal.

Withdrawing?

Unitholders who lodged a redemption request during the June cycle remain entitled to their FY26 distribution. As the final distribution calculation is still being completed, payment of redemption proceeds will be delayed and is expected to be made at approximately the same time as distribution payments. We appreciate your patience while this process is finalised.

What to do now

Three things between now and 30 June:

- Check your DRP preference. If you want to reinvest your FY26 distribution, or change your existing election, log in to the Automic Investor Portal (link), follow Automic’s step-by-step DRP guide (link), or use the paper DRP form (link) and email a copy to ophir@automicgroup.com.au. For the unlisted funds, elections must be received by close of business 30 June 2026. For OPH, in line with the ASX timetable, DRP elections close on 2 July 2026 (the first business day after the record date).

- Check your bank account details. Important: missing or out-of-date details means you may be deemed to have elected DRP by default.

- Final figures and statement timing will be confirmed in our late-July follow-up.

As always, if you’d like to chat to us about any of the Funds, please feel free to call us on (02) 8188 0397 or email us at ophir@ophiram.com.

Thank you for entrusting your capital with us.

Kindest regards,

Andrew Mitchell & Steven Ng

Co-Founders & Senior Portfolio Managers

Ophir Asset Management

This document has been prepared by Ophir Asset Management Pty Ltd (ABN 88 156 146 717, AFSL 420082) (“Ophir”) and contains information about one or more managed investment schemes managed by Ophir (the “Funds”) as at the date of this document. The Trust Company (RE Services) Limited ABN 45 003 278 831, the responsible entity of, and issuer of units in, the Ophir High Conviction Fund (ASX: OPH), the Ophir Global Opportunities Fund and the Ophir Global High Conviction Fund. Ophir is the trustee and issuer of the Ophir Opportunities Fund.

This is general information only and is not intended to provide you with financial advice and does not consider your investment objectives, financial situation or particular needs. You should consider your own investment objectives, financial situation and particular needs before acting upon any information provided and consider seeking advice from a financial advisor if necessary. Before making an investment decision, you should read the relevant Product Disclosure Statement (“PDS”) and Target Market Determination (“TMD”) available at www.ophiram.com or by emailing Ophir at ophir@ophiram.com. The PDS does not constitute a direct or indirect offer of securities in the US to any US person as defined in Regulation S under the Securities Act of 1993 as amended (US Securities Act).

All Ophir Funds are deemed high risk within their respective Target Market Determination documentation. Ophir does not guarantee the performance of the Funds or return of capital. An investment may achieve a lower than expected return and investors risk losing some or all of their principal investment. Past performance is not a reliable indicator of future performance. Any opinions, forecasts, estimates or projections reflect our judgment at the date of this was prepared, and are subject to change without notice. Rates of return cannot be guaranteed and any forecasts, estimates or projections as to future returns should not be relied on, as they are based on assumptions which may or may not ultimately be correct.

Actual returns could differ significantly from any forecasts, estimates or projections provided.

The Trust Company (RE Services) Limited is a part of the Perpetual group of companies. No company in the Perpetual Group (Perpetual Limited ABN 86 000 431 827 and its subsidiaries) guarantees the performance of any fund or the return of an investor’s capital.