In our Investment Strategy Note we review the mammoth outperformance of stocks over the long run versus bonds and cash, including why we expect this to continue in the future despite calls by some of excess equity market valuations.

Even before the onset of the Covid-19 pandemic, investors faced significant challenges building long-term wealth.

With a muted outlook for economic growth and inflation, equity investors were unlikely to earn the double-digit percentage annual returns that they had become accustomed to.

At the time many analysts believed that risk-adjusted sharemarket returns over the next decade were likely to be half of those achieved in the past 20 years, an outlook that may have forced investors to revise their portfolio strategy.

But despite that outlook, and despite concerns that equities are now ‘overvalued’ after strong post-Covid rallies, investors’ asset allocation decision hasn’t changed drastically.

That’s because, compared with other asset classes, equities are still offering investors the most compelling investment case in our opinion, and the most compelling chance to build long-term wealth and maximise their lifestyle in retirement.

Clear and unequivocal outperformance

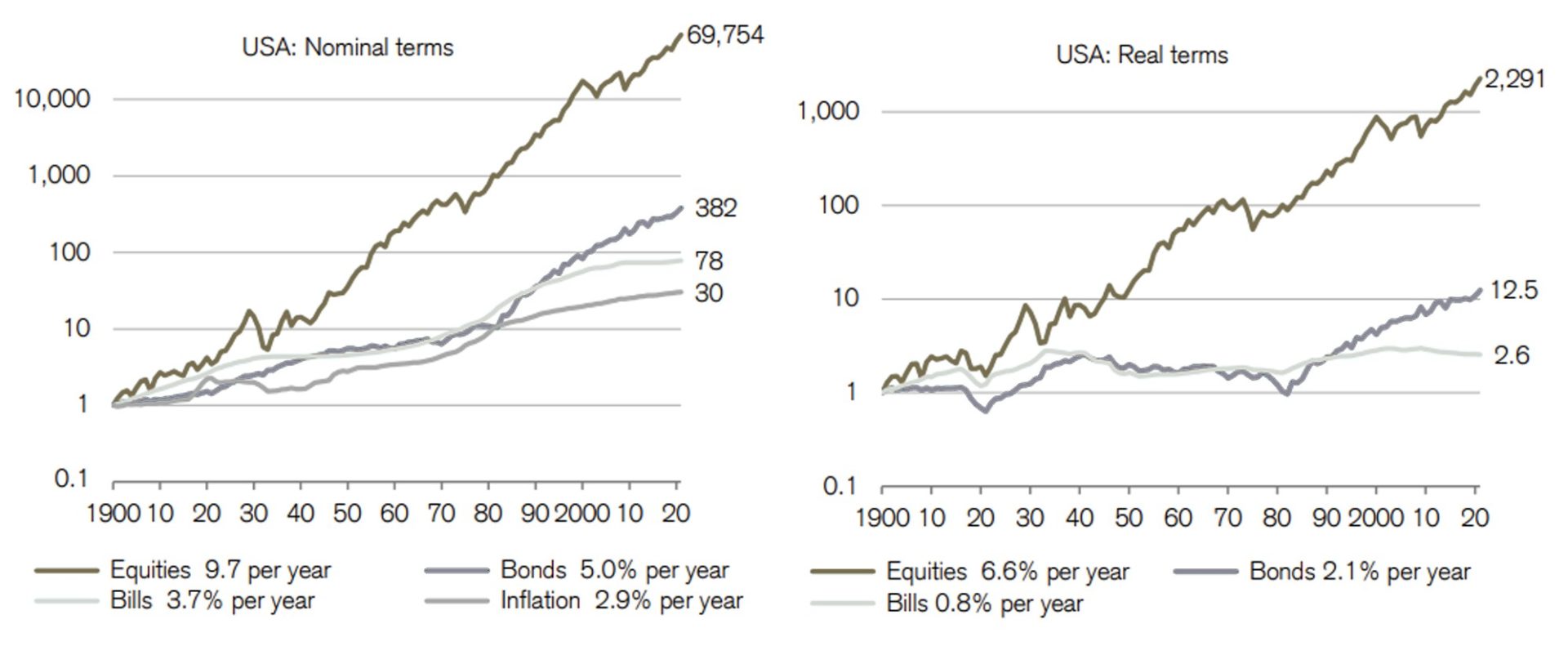

Through the decades, equities have by far and away been the top-performing asset class. The charts below show the cumulative total returns in the US market over the last 121 years from stocks, bonds, bills (i.e., cash), and inflation. Equities performed best, returning 9.7% per year versus 5.0% on bonds, 3.7% on cash, and inflation of 2.9% per year.

Cummulative returns of US asset classes, 1900-2020

Source: Dimson, Marsh & Staunton, Global Investment Returns Yearbook CS 2021

The extent to which equities outperformed the other asset classes is clear and unequivocal. Furthermore, this study captures some notable setbacks: two world wars, the great depression, an OPEC oil shock,the GFC and COVID-19. In each case, equities eventually recovered and reached new highs.

Why fixed income and cash now do nothing for wealth creation

When thinking about future asset class returns, we must acknowledge how exceptionally low interest rates now are.

Short-term interest rates in Australia, the US and most other developed economies are near zero, or in some cases negative! Central banks seem intent on maintaining this support, with interest rate futures factoring low rates to remain for at least the next four years.

Although inflation is soft and likely to be contained, it still sits at a level above both short and long-term interest rates. Because of this, rates in Australia are negative in real terms.

This means that investment dollars sitting in these cash and fixed income asset classes are generally losing value after inflation.

For investors seeking long-term wealth creation, government bonds offer nothing to an investor, and should only be considered in a portfolio for diversification purposes. Meanwhile, cash holding should be kept to the bare minimum, purely as a means to facilitate liquidity.

Real interest rates – Australia

Source: Refinitiv

The shrinking equity risk premium

So what does this mean for equities? The answer is: a lot. The return investors seek on equities need to be related to the returns on such supposedly ‘safe’ assets such as Government bonds.

Because they are riskier (more volatile) than Government bonds, investors demand to earn more from equities to justify owning them. This relationship is known as the ‘equity risk premium’ — the excess return investors expect from equities over the returns on risk-free government bonds.

Although this premium cannot be measured directly, since it only exists in investors’ minds, it can be inferred from historical experience.

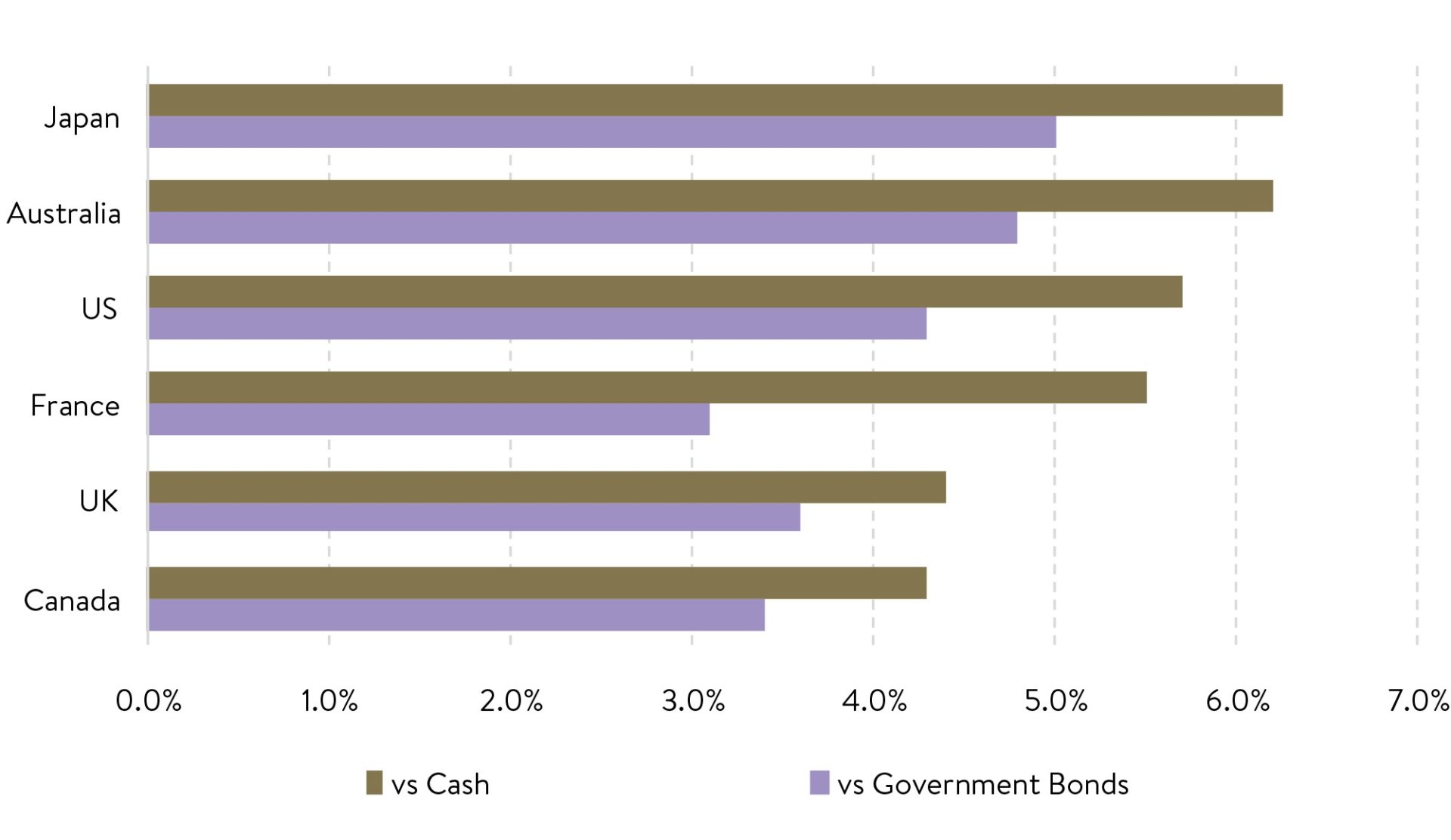

Elroy Dimson of the London Business School estimates the excess return on world stocks over bonds at 3.2 percentage points between 1900 and 2020. The excess is estimated at 4.8 percentage points for Australia; and for the US, at 4.4 percentage points.

Equity risk premiums (annualised) 1900 to 2020

Source: Dimson, Marsh & Staunton, Global Investment Returns Yearbook CS 2020

There are reasons to believe, however, that the risk premium demanded by equity investors may now be lower than the historical average. Corporate governance has improved dramatically over the last 50 years, while policymakers have smoothed the business cycle through shrewd inflation targeting.

Still beating bonds

But with interest rates cemented close to zero, equity returns need not be outstanding to maintain their relative appeal.

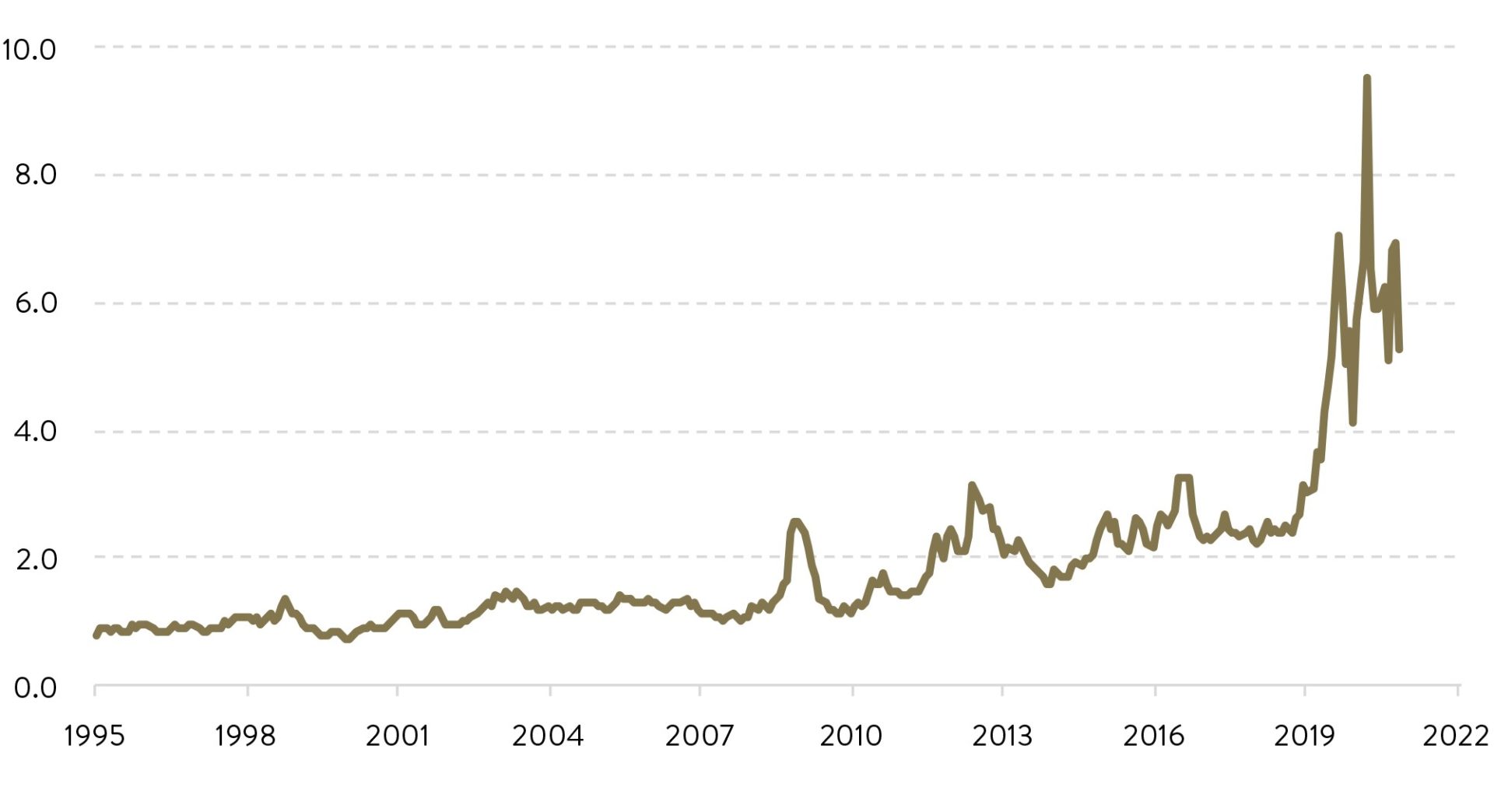

The most striking way to illustrate superiority of equities as an investment class is to compare its earnings yield with the yield on government bonds. Even following their 40% rally since late March, the chart below shows this yield premium on offer from equities at still-near-record levels.

Earnings Yld (AUS equities) / Bond Yld (Aus)

Source: Refinitiv

The same point can be made by flipping this comparison into price-earnings multiples. The Australian equity market’s current PE of around 20x is often pointed out as expensive and a sign of poor future returns. But this 20x multiple – which implies a yield of 5% — looks cheap compared against the 55x multiple investors are effectively paying when buying Australia’s government bonds that currently yield just 1.8%.

So, although traditional PE measures show equities to be expensive versus their own history, they are still cheap versus bonds.

It is for this reason that overall asset allocation preference remains firmly in favour of equities. At the same time, it is conceivable that equity multiples could expand further. For example, the heavily quoted cyclically adjusted PE, or CAPE, of the ASX top 200 is not expensive on long-run measures.

Returns that build real wealth

If we accept that equities are one of the few asset classes that offers investors scope to grow real wealth going forward, what sort of returns can be expected?

In our opinion, when you combine earnings growth, dividends, and the boost from franking credits, a 10% annual return from the Australian share market overall should be achievable over the long term. We acknowledge though that over the next few years it might be lower than this.

In terms of raw returns, international equities markets probably will not outpace Australian equities once franking credits are taken into account domestically. Global stocks do, however become competitive on risk-adjusted measures once market diversification and currency impacts are considered.

Some investors may be worrying that equities are overpriced given they are hitting fresh highs. But even though many equity markets are at, or near, all-time highs, we do not see this as an obstacle to further share market gains. Even after record highs, subsequent 12-month returns from equities have generally been strong.

Furthermore, while buying into the market slowly in dribs and drabs (dollar-cost averaging), can help mitigate investors’ fears of bad market timing, history suggests that investing all at once into the sharemarket generates higher returns than dollar-cost averaging on average.

Outperforming with stock selection

While equities are still promising strong returns, it is important to remember that at Ophir, internally we target 15% per annum total returns over the long term (5+ years) across all our equity strategies.

That means our investment team is seeking to outperform the market benchmark for each of our funds through stock selection.

This is a hurdle we have more than achieved historically and one we hope that means we can continue to under promise and over deliver.