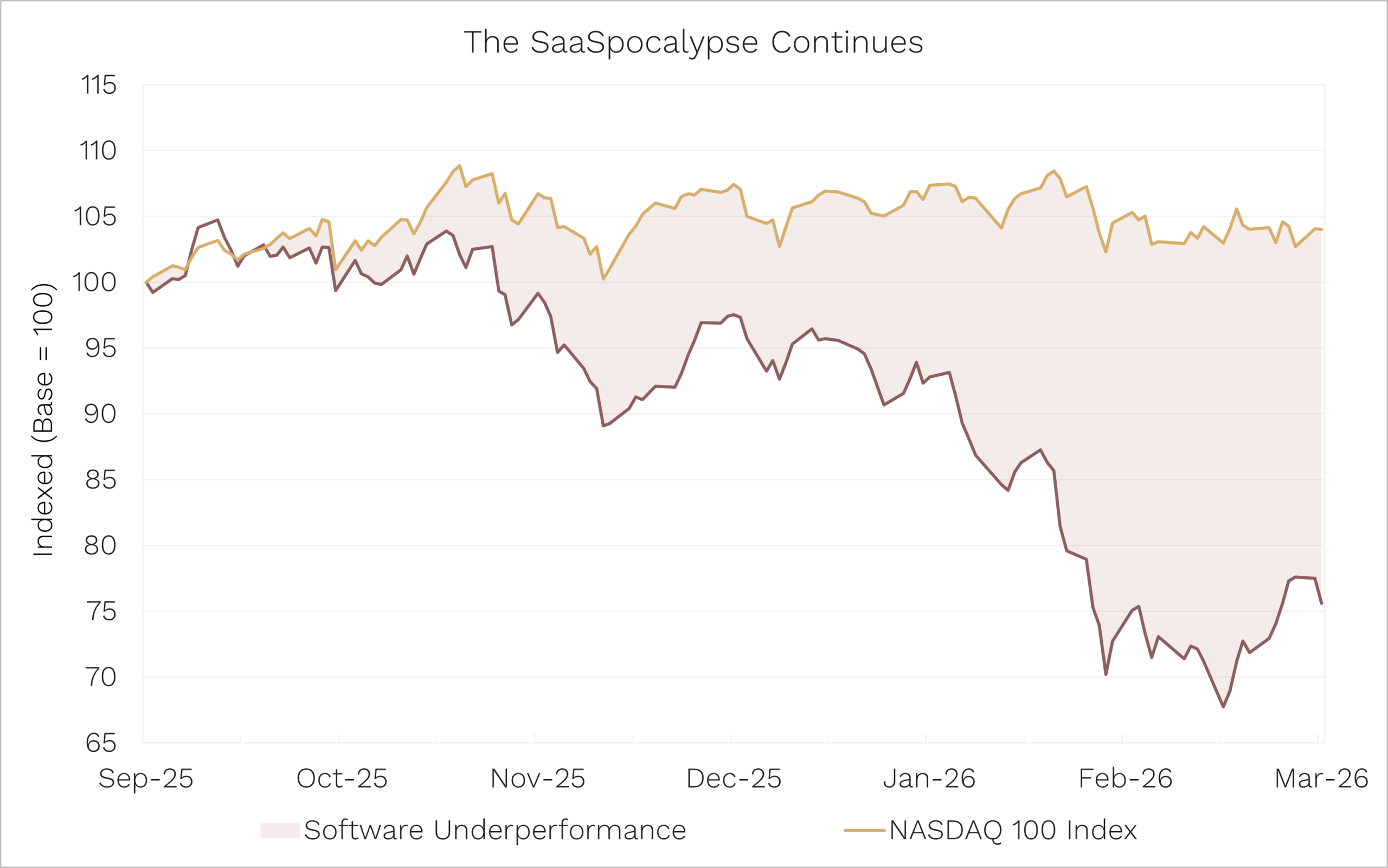

There is no doubt the SaaSpocalypse (the savage sell-off of software stocks) was bad. But since we published our piece on the topic last month, titled SaaSpocalypse Now!, the AI disruption debate has intensified further, and the sell-off has broadened well beyond SaaS.

This was driven by several new tool releases from Anthropic, but it culminated when Citrini Research released a thought experiment titled, “The 2028 Global Intelligence Crisis”, on the 22nd of February. The piece imagines an AI automation shock that sees human workers replaced so rapidly that it ultimately tips the economy into a demand and credit spiral.

Source: Ophir, Bloomberg, data as at 10 March 2026. Software measured by S&P North American Technology Software Index.

We believe there are three things investors need to be doing to navigate this uncertainty:

- Firstly, they need to understand that the debate around agentic AI disruption is more nuanced than doomsday scenarios suggest.

- Secondly, they also need to bucket which companies will be best protected from AI disruption and will become opportunities when the debate settles.

- And they also need to look beyond the AI noise for compelling opportunities. (One we’ve found is Artivion, our brief case study.)

Below, we examine each of these.

The Doomsday Scenario Misses Real-World Offsets

First up, we take AI disruption risk seriously. But the AI doomer fanfiction disregards the frictions, constraints, and offsets that matter in the real economy.

We don’t believe AI agents will create as much disruption as the Global Intelligence Crisis suggests for several reasons:

-

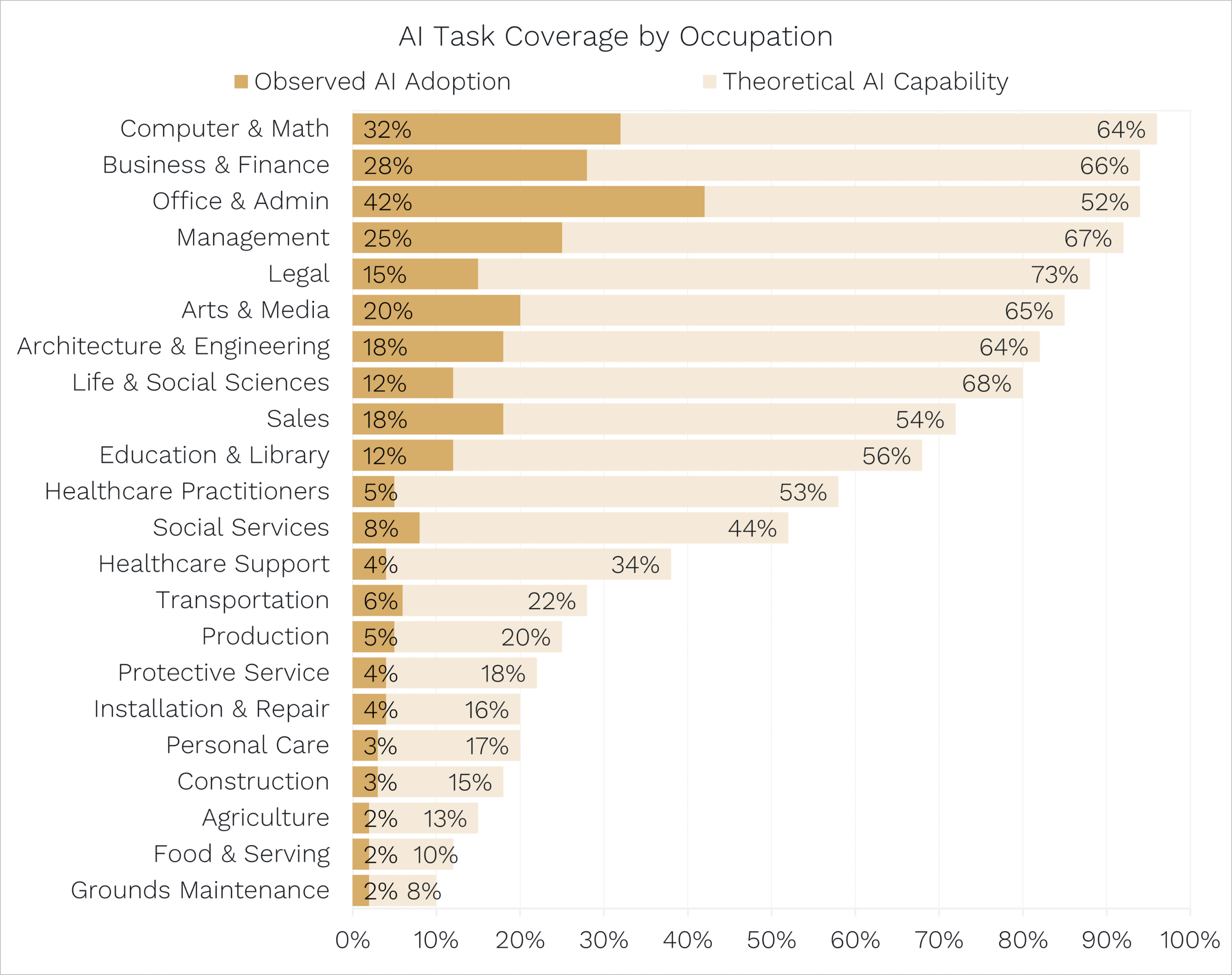

Adoption is not the same as capability

Even if the capability of AI models improves quickly, it doesn’t mean that enterprises can roll out their use quickly. Real-world deployment is challenging – it runs into process change, integration risk, legal liability, governance, and regulatory constraints. Capability can move fast. Implementation is slow, expensive, and messy.

Source: Anthropic: Labor market impacts of AI, 5 March 2026.

-

Physical constraints create a speed limit

For large-scale displacement of SaaS to happen, it would require vast infrastructure: chips, data centres, energy, and connection to the grid. If the supply of compute – the processing power needed for AI – can’t keep up with demand, its marginal cost rises. It will become less appealing for enterprises to switch to compute-intensive AI agents and substitution will slow. There is, therefore, a real possibility that infrastructure bottlenecks will limit the pace of near-term displacement.

-

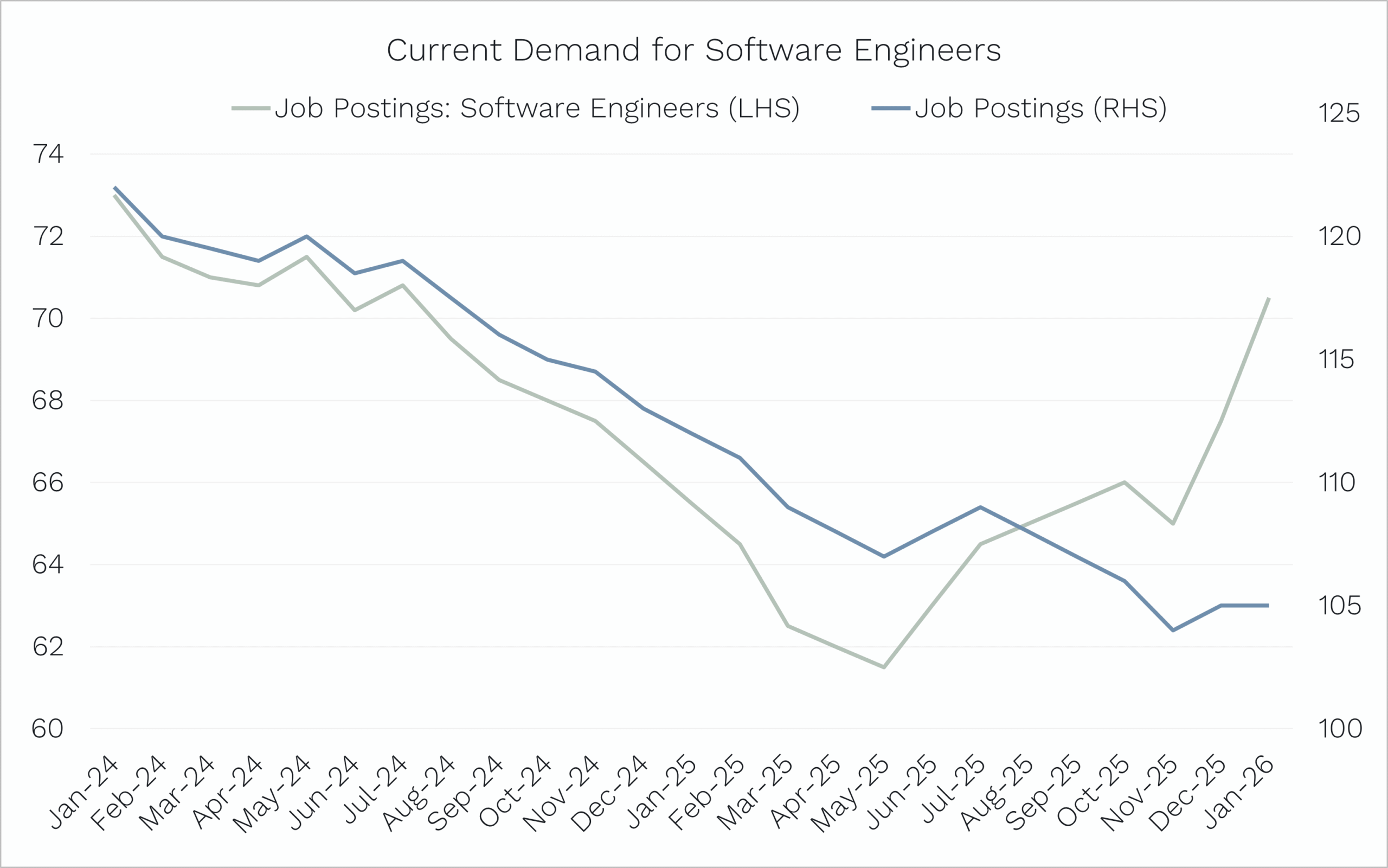

The labour market is not yet showing collapse

So far, the data does not support ‘systemic’ displacement. In their own rebuttal piece, Citadel Securities pointed to still-low unemployment and continued demand for software engineers as evidence that the feared feedback loop is not present today. While there has been an increase in tech companies pointing to AI as the reason for layoffs, there is a strong case to be made that many of these businesses had bloated work forces following hiring sprees during the COVID period. While AI is clearly driving efficiency, there is likely an element of it being used as an excuse for these businesses to right-size their work force.

Source: Citadel Securities, Indeed. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

-

AI is, mechanically, a supply shock

Finally, automation is fundamentally a productivity shock, which historically lowers marginal costs and expands the frontier of what can be produced and consumed. An economic collapse scenario requires extra assumptions layered on top: failed redistribution of wealth, no reinvestment of capital income generated by AI, and a sudden absence of new categories of demand. While this is possible, it’s highly unlikely this would occur.

The Real Debate: Speed of Absorption

That being said, we are not arguing that AI won’t disrupt white-collar jobs. It almost certainly will (see Wisetech, Block and Atlassian). To us, the real question is: How quickly the system can absorb that disruption?

If AI enables firms to do the same work with fewer people, labour displacement could occur faster than wages, policy, and new job categories can adjust. That’s the scenario that creates genuine macro risk – not the existence of automation itself.

History suggests new technologies eventually create new industries and new demand, but the transition is rarely smooth. The adjustment path matters enormously. Will we see a gradual reallocation over years, or a sharper reset over quarters?

And if the transition is too abrupt, the stabilisers will come. Government support could become an important offset – whether that’s targeted wage subsidies, retraining programs, or tax reform. Or will the productivity enhancement be so significant that we see what Elon Musk has been advocating for: Universal Basic Income (UBI)?

The point isn’t to predict the policy mix. It’s to recognise that society doesn’t just accept a sudden income shock without a response.

In our view, the AI disruption debate is not about ‘doom versus boom’. It’s a question of timing, friction, and policy reaction – and the market needs those variables to become clearer before terminal values and multiples are revised materially higher.

Our Framework: Disrupted, Protected, Native

To navigate this regime shift, we’ve been grouping AI exposure into three buckets:

- AI Disrupted – Traditional seat-based SaaS and other business models where AI can plausibly substitute the paid workflow.

- AI Protected – Businesses with stronger moats: regulatory barriers, proprietary data, network effects, infrastructure positioning, mission-critical integration, and switching costs.

- Native AI – Unlisted, early-stage, or not yet created.

The issue today is that Buckets 1 and 2 have been sold off together. The market is not yet consistently distinguishing between ‘disrupted’ and ‘protected’.

And while our Funds haven’t been immune from this disruption via some software, ad-tech, and AI-adjacent holdings, we resisted the temptation to ‘double-down’ by increasing the weights in these names while the debate continues.

Our view is that Buckets 2 and 3 are the long-term winners, which means Bucket 2 should recover once markets regain confidence in certain competitive moats that will protect those businesses from disruption.

That is the set-up we are watching for before we materially increase weights in selected ‘protected’ software names trading on lower multiples.

Looking beyond the AI noise

Amidst the uncertainty, many investors have been seeking security in themes such as AI infrastructure/semis and defence. While we have exposure to these thematics, we are conscious of crowding. Similarly, we are not piling into cyclicals or going maximum overweight healthcare.

While we do have exposure to AI infrastructure and defence, we’re complementing it with names across a diversified range of sectors that have been overlooked and offer compelling return profiles at attractive valuations. And we’re actively seeking less GDP-sensitive names where revenue is not closely tied to the macro cycle.

Over the past two months, therefore, we’ve added a broad range of companies spanning:

- Countercyclical consumer beneficiaries

- Highly resilient industrials

- US medtech

Medtech Compounder: Artivion (NYSE: AORT)

One recent addition that illustrates how we’re finding compelling opportunities away from the AI noise is Artivion, a ~US$2bn medical device company headquartered near Atlanta, Georgia.

Artivion is focused exclusively on aortic disease – a highly specialised area of cardiac and vascular surgery. Their product portfolio spans four key areas:

- Aortic stent grafts

- The On-X mechanical heart valve

- Surgical sealants (BioGlue)

- Implantable human tissues.

They sell into more than 100 countries worldwide.

We’ve been deeply engaged in Artivion for several years and followed the company through multiple product cycles, clinical readouts, and management meetings. The work we’ve done leads us to believe the company will experience a product-led growth acceleration into 2027 and beyond.

The stock recently pulled back after the market got ahead of itself when it priced in the expectation that some of this product-led growth acceleration could be pulled forward into 2026. When the timeline reverted to the original 2027 trajectory, the share price gave back those gains.

For us, this was the opportunity because the fundamental thesis hadn’t changed. We now believe we’ve been able to buy a high-quality, accelerating growth story with over 20% three-year EBITDA compound annual growth rate (CAGR) at a ~50% discount to standard sector takeout multiples.

Source: Ophir, Bloomberg, data as at 11 March 2026.

Artivion is exactly the kind of name we’re drawn to right now: a medtech compounder with product-cycle driven growth, limited GDP sensitivity, and a valuation that reflects neither the clinical pipeline nor the margin expansion runway.

It doesn’t need a resolution to the AI debate to work. It just needs its products to keep performing – and so far, they are.

The debate continues

We also have a deep pipeline of potential investments in active, high-return opportunities across healthcare, industrials, financials, and – of course – AI winners and defence names.

We will continue, however, to maintain high hurdle rates due to crowding risks.

When it comes to AI, while the worst of the rotation appears to be over and AI-disrupted baskets of stocks have recently had some reprieve, we still don’t see an imminent resolution to this debate.

This will limit the extent to which beaten-up names can re-rate, with multiples likely to remain depressed compared to historical levels.

Meanwhile, the market is likely to keep oscillating between ‘doom’ and ‘boom’ narratives as new tools launch and macro confidence shifts.