In our Investment Strategy Note we discuss why we see small caps as the best place to pick stocks.

Companies in the Australian small cap index are generally young, nimble and have the potential for high growth. However, among these small cap stocks, there is a significant degree of variability in both quality and valuation, which leaves many of these companies under-appreciated and misunderstood.

In this note we will outline three key reasons which make the small cap universe prone to inefficiencies and why small cap investing provides an ideal ground for our team to identify the companies most likely to generate consistent long-term returns

1. Unloved and Under-owned

There are many more small cap stocks than large cap stocks, and the vast size of the small cap stock universe presents a significant dilemma for large investment managers and sell-side analysts. Many of the traditional investment managers, who pride themselves on deep analysis of individual companies and management teams, no longer have the ability to effectively cover the full breadth of the small cap universe. Sell side research analyst are suffering from a similar lack of resources, with 70% of the companies in the small cap universe having fewer than three analysts covering them, and nearly 50% having no analyst coverage at all. Given the investment community has less and less time to focus on individual stocks, the focus for many has shifted toward the largest, most liquid names.

The inefficiencies and mispricing which come from a lack of coverage, have been exacerbated by a lack of ownership. Large institutional investors value liquidity and being able to make investments in size. They therefore tend to largely ignore companies in the small cap universe.

2. A Mix of Diamonds and Duds

Another aspect where the small cap universe differs sharply with the large cap space is on measures of profitability and quality. At any given time, roughly 20% of the companies in the ASX small cap index are non-revenue or profit generating. This reality should immediately signal to investors the need for actively managing this exposure. By contrast, consistent profitability and viability is a de-facto prerequisite for member companies of the large cap universe, and even more so for the blue-chip stocks. Avoiding corporate blow-ups has been shown to be one of the best strategies towards generating strong returns.

What this means, is that investment managers with skills in picking stocks are much more valuable across small cap portfolios.

3. Inefficiencies Create Opportunity

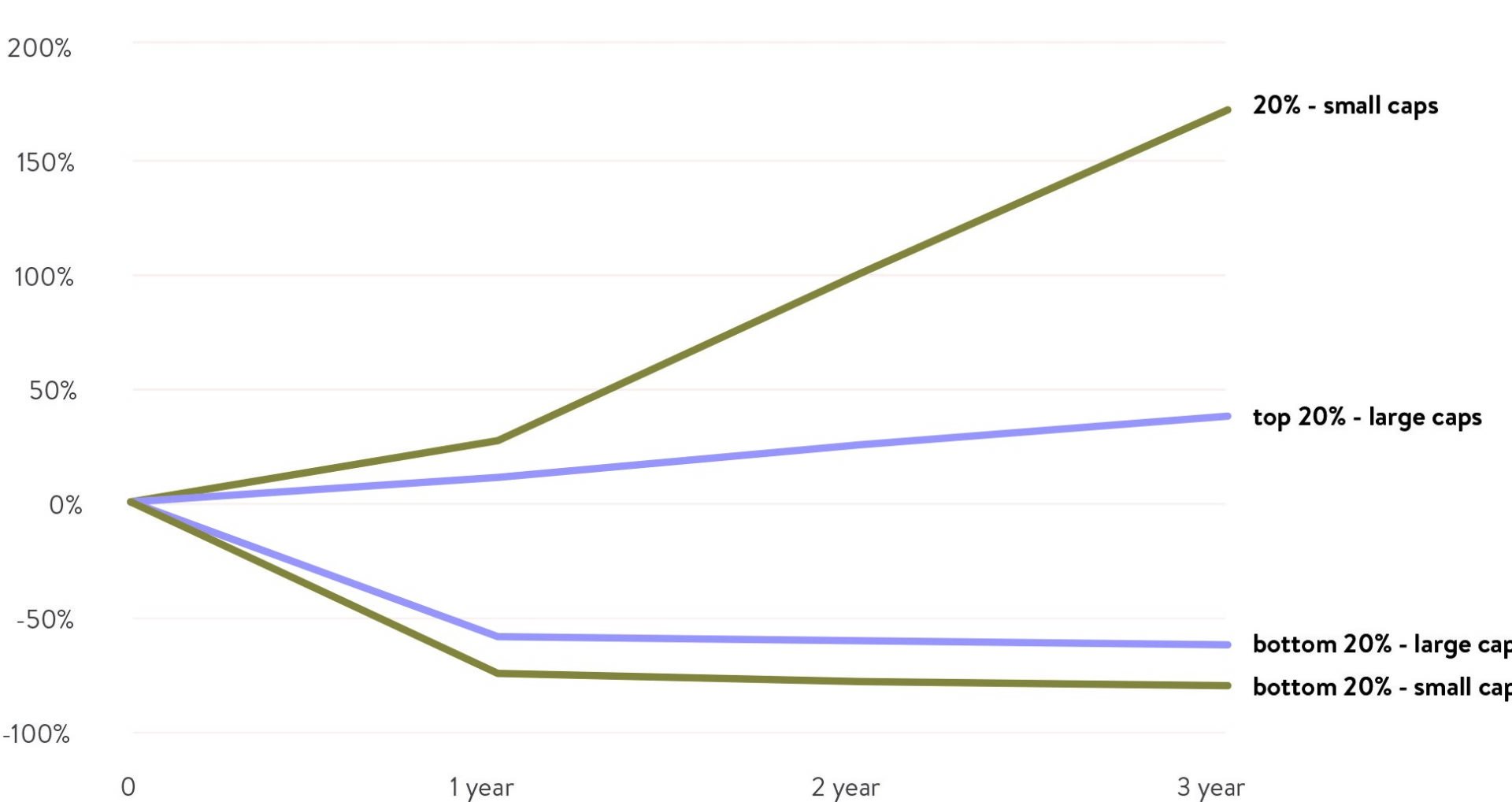

These inherent inefficiencies within the small cap universe create a greater opportunity for outsized investment returns. This can be illustrated best by simply comparing the dispersion of stock returns over any given 12 month period. To do this, below we have organized stocks into five buckets (quintiles) from best to worst performance. What jumps out immediately is that as you move down towards smaller stocks, returns are much more dispersed, on average. As shown in chart 2 below, the best quintile of stocks from the Australian small cap universe have returned +172 percent on average over the last three years. On the flip side of the equation, small caps stocks in the worst quintile fell by 80 percent on average during the same time period. Performing this same exercise across the large cap universe showed a less compelling spread, with the top quintile up by just 38 percent on average, and the bottom down by 62 percent on average. The wider dispersion of returns from small cap equities highlights just how critical it is to align one’s portfolio with the outperformers of this index, and to avoid the underperformers.

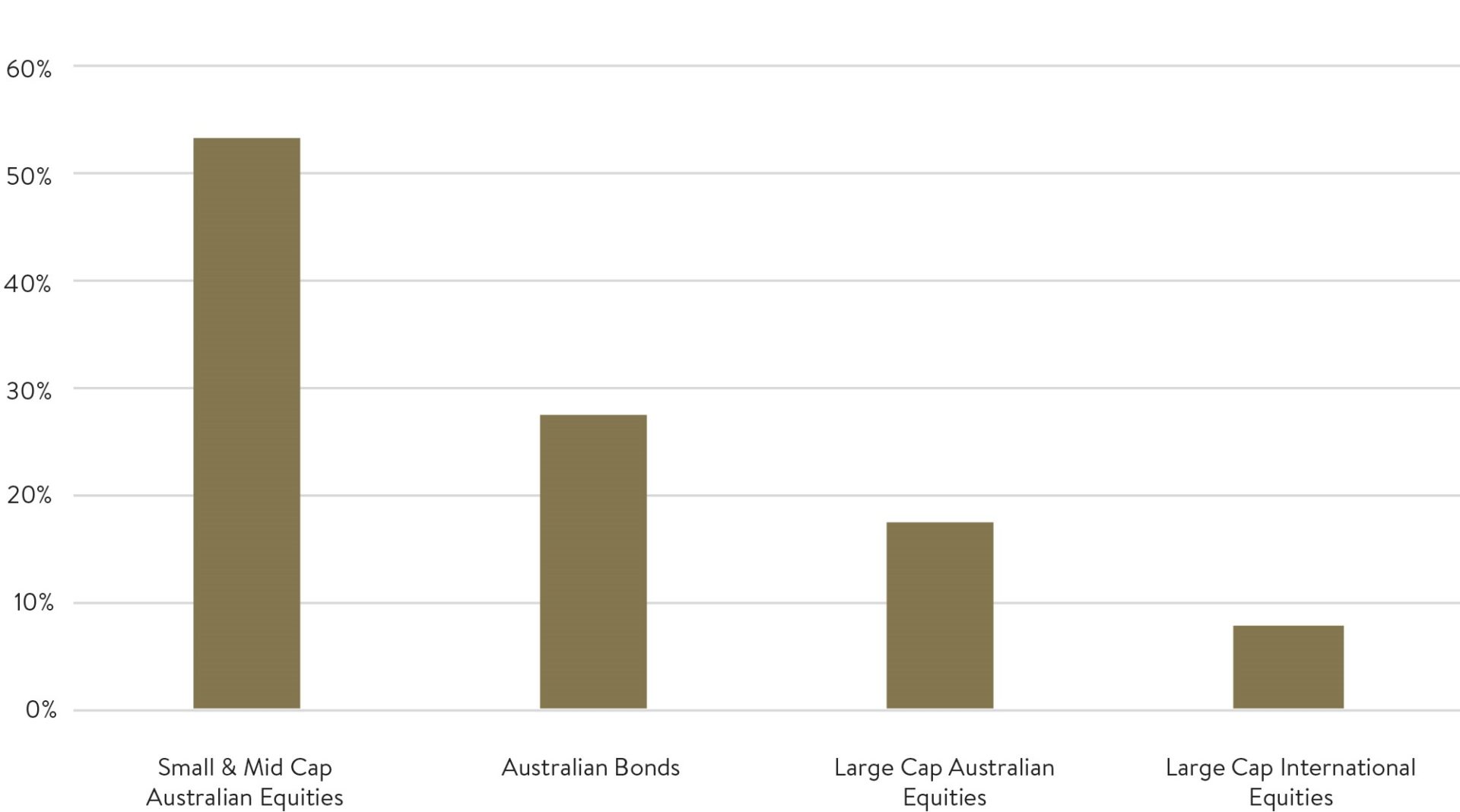

Percentage of Funds Which Outperformed their Benchmark – Last 10 years

Source: MSCI SPIVA, Data to 30 June 2019

Dispersion of Returns – Australia Small caps vs Large Caps

Source: S&P, Refinitiv, Data to 30 June 2019

In summary

Since our goal is to earn the highest returns possible above the market without taking undue risk, it stands to reason that we prefer parts of the market which offer the greatest chance of such large returns. And with most of the traditional investment funds simply being unable to run meaningful small-cap portfolios, many of these stocks go unnoticed. At Ophir we believe that these inefficiencies within the small-cap universe allow for outstanding opportunities for disciplined investors and why small cap investing provides an ideal space to generate the strongest gains to your portfolio.