By Andrew Mitchell & Steven Ng

Co-founders and Senior Portfolio Managers

In our May 2020 Letter to Investors we discuss whether the remarkable rise in global share markets can continue and why as investors now is the time to be very selective.

Dear Fellow Investors,

Welcome to the May 2020 Ophir Letter to Investors – thank you for investing alongside us for the long term.

The remarkable market rebound has thrown up opportunities, but it’s not time to be making big bets.

A remarkable rise continues

May will go down in history as the month much of the world started re-opening from the COVID-19 shut down. Along with some improving leading economic data, the reopening saw global sharemarkets follow up April’s very strong gains with further, albeit smaller, rises in May.

The benchmark global share index (MSCI ACWI USD) rose 4.4%, following April’s 10.8% gain. The local Australian sharemarket (ASX200 Index) also rose 4.4% after gaining 8.8% the month before.

Global Shares (MSCI ACWI) continue their march higher

Source: JP Morgan

Whilst the local Australian bourse, is still a relative laggard compared to most other markets in this recovery, having recouped just under 50% of its losses, the speed of the rise has been extraordinary.

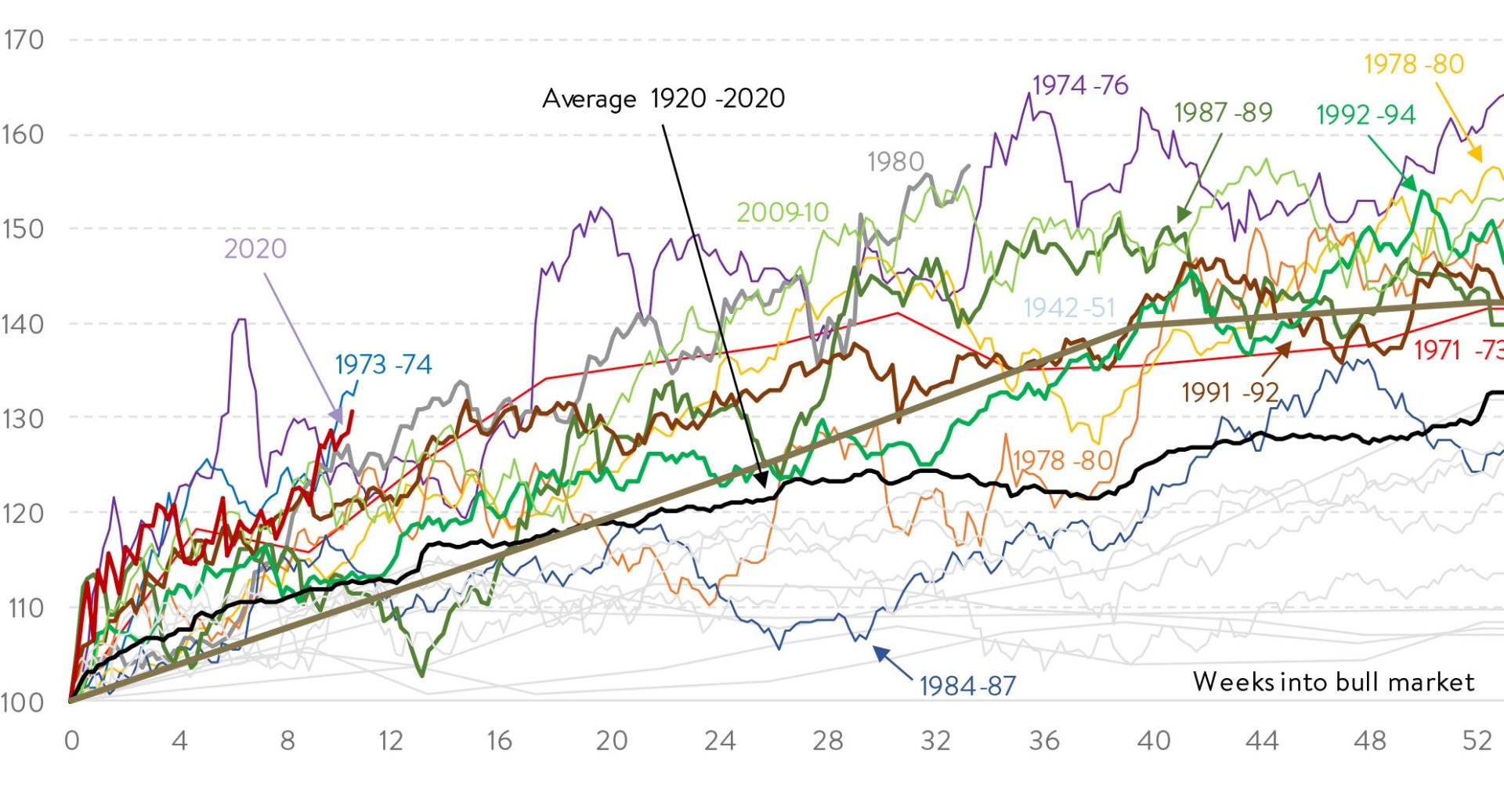

COVID-19 has now seen the fastest bear market (>20% falls) in history followed up by the second fastest bull market (>20% gains). The average bull has put on 30% over a year, whilst the market’s current rise has done this in just 10 weeks. A similar story has been seen in most of the other major sharemarkets.

ASX 200, or equivalent, capital return during the fist 52 weeks of a bull market

Source: RBA, Refinitiv, MST Marquee

Ophir May Fund Performance

We have been very pleased with how the Ophir Funds have performed in recent months in what has been an extremely challenging market environment.

The Ophir Opportunities Fund returned +13.2% for the month after fees, outperforming its benchmark by +2.6%. Since inception, the Fund has returned +24.6% per annum after fees, outperforming its benchmark by +18.3% per annum.

Download Ophir Opportunities Fund Factsheet

The Ophir High Conviction Fund investment portfolio returned +9.0% for the month after fees, underperforming its benchmark by -0.2%. Since inception, the Fund’s investment portfolio has returned +18.4% per annum after fees, outperforming its benchmark by +9.7% per annum. The Ophir High Conviction Fund’s ASX listing provided a total return of +5.1% for the month.

Download Ophir High Conviction Fund Factsheet

The Ophir Global Opportunities Fund investment portfolio returned +9.6% for the month after fees, outperforming its benchmark by +4.2%. Since inception, the Fund’s investment portfolio has returned +28.8% per annum after fees, outperforming its benchmark by +30.4% per annum.

Download Ophir Global Opportunities Fund Factsheet

But can this remarkable rise continue?

Investors are rightly asking whether this rise can continue when Australia is about to enter its first recession in 29 years and the world enters its deepest recession since World War Two.

All this is happening as record numbers of companies have withdrawn formal guidance given the uncertain months ahead, though in Australia Treasurer Josh Frydenberg has given listed companies cover for this after he announced the suspension of continuous disclosure rules for six months.

Despite this lack of clarity from companies, stock indices have decoupled globally from earnings on the back of supportive valuations, momentous fiscal and monetary support, and as investors eye an end to the profits recession as the global economy starts to reopen.

Not everyone agrees that this rise is justified.

Investors can generally be split into two camps: those focussing on economic and profits data right here, right now – and the story is very bad; or those looking at valuations compared to bonds, the stop gap measures by authorities and the recovery in profits ahead.

At the moment the latter is winning the battle.

The market seems to be pricing a V-shaped recovery in profits globally. While this is an average, clearly not all companies will be this lucky. A V-shaped profits recovery does, however, have quite a reasonable chance of occurring and is probably still the base case.

But there a lot of unknowns, such as how much reopening can be done without a second wave of infections or when and how effective will a vaccine or therapeutics be. The market doesn’t appear to be pricing a second virus wave, delayed vaccine/therapeutics, slow labour rehiring or escalating US-China tensions.

We’re seeing typical bear market recovery rotations

If we drill down into the market action in May we can see it continued a similar path to April with the market moving higher but masking high daily and intraday volatility and meaningful divergence of returns from particular sectors and investing styles. As we discussed last month this kind of volatility is not uncommon as economies enter recessionary environments and simply reflect a market trying to actively price in a wide range of future outcomes. This volatility is elevated because of the limited history or reference points to price in forced economic shutdowns and subsequent reopening.

Initially defensive and growth orientated sectors of the market led the rally in sharemarkets from the March bottom as investors added risk in safer areas. Through the second half of May, though, there was evidence that investors had become bolder as cyclical and value sectors such as Industrials, Materials and Financials started leading the way, along with lower quality companies with higher debts levels. In Australia, the Big Four banks have led. In the last week of May we saw Westpac outperforming Resmed and ANZ outperforming CSL by around 25% each. This general sector rotation saw our investment strategies pair back some of their relative performance that they had put on earlier in May.

These rotations are typical coming out of bear markets though, ultimately, we think will be constrained by the low/no growth and low inflation world we are in and constraints on spending as some forms of social distancing stay with us for some time yet.

What does this indicate for the sustainability of the market recovery?

Whilst we haven’t been trying to time these rotations, we have become slightly more aggressive in our portfolio positioning as it’s become clearer that spending is starting to improve in some parts of the world.

The reality of re-opening is actually a mixed picture

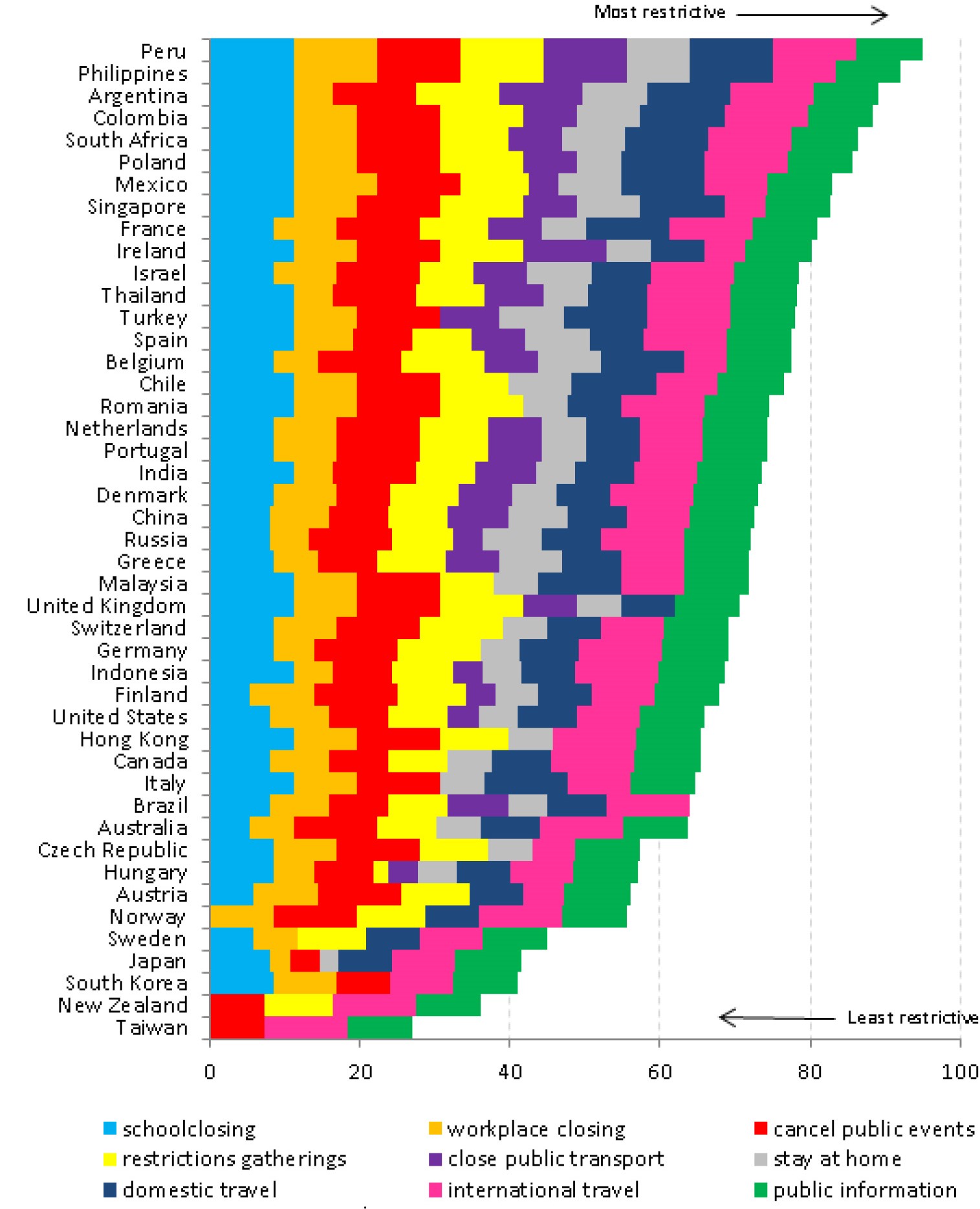

Whilst the re-opening theme took hold in earnest in many parts of the world in May, it’s actually a mixed picture. Below we show the Oxford University’s Stringency Index which attempts to measure where individual countries are currently at in their various forms of lockdown.

Decomposition Oxford Stringency Index

Source: UBS, Oxford University,

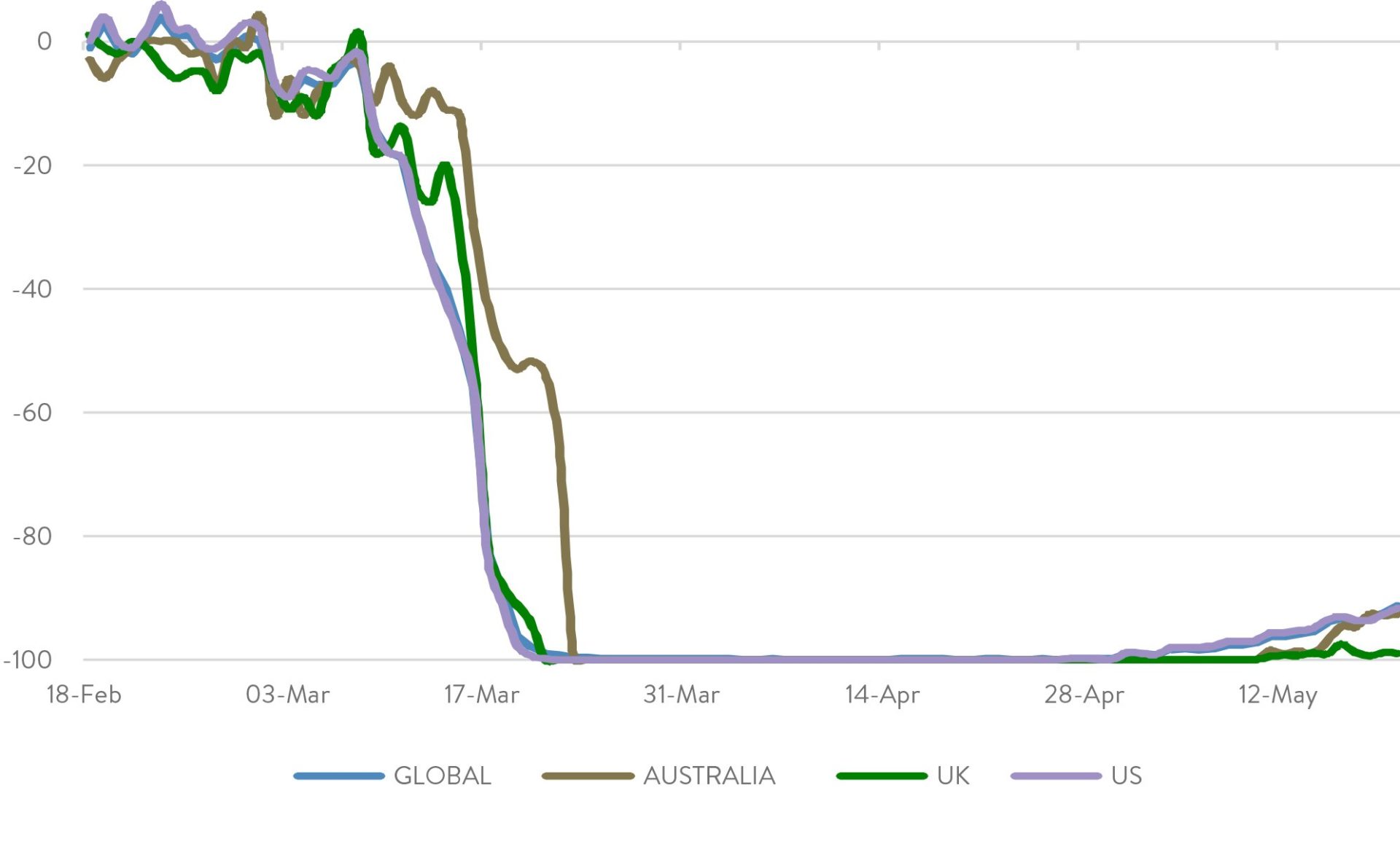

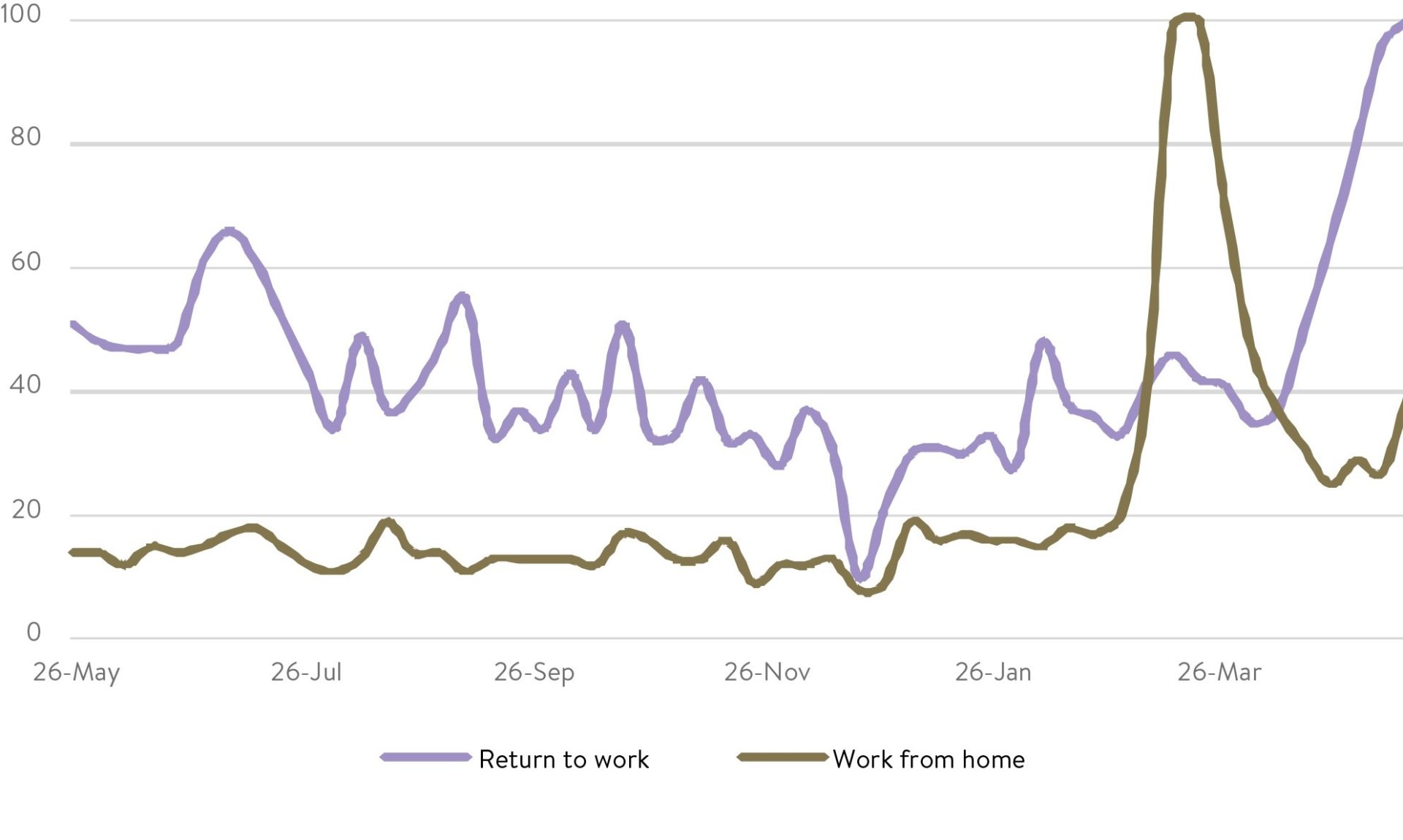

What you can see is that there is no “one size fits all” approach and that some of the measures that tend to be eased first are “stay at home” and “close public transport”. The finance industry has become very adept now at putting together various forms of “alternative” data that give a more real time view of how economies are reopening and the story here has generally been encouraging. We give you an idea of this in the panel of charts below with restaurant bookings starting to increase, google searches for “return to the office” now outstripping “work from home”, some debit and credit card spending rebounding in the US, and foot traffic and sales improving at shopping centres in Australia.

Open Table Bookings

Source: JP Morgan, Open Table.com

Return to the Office (RTTO) overtakes Work from Home (WFH) in Australia

Source: JP Morgan, Google Trends

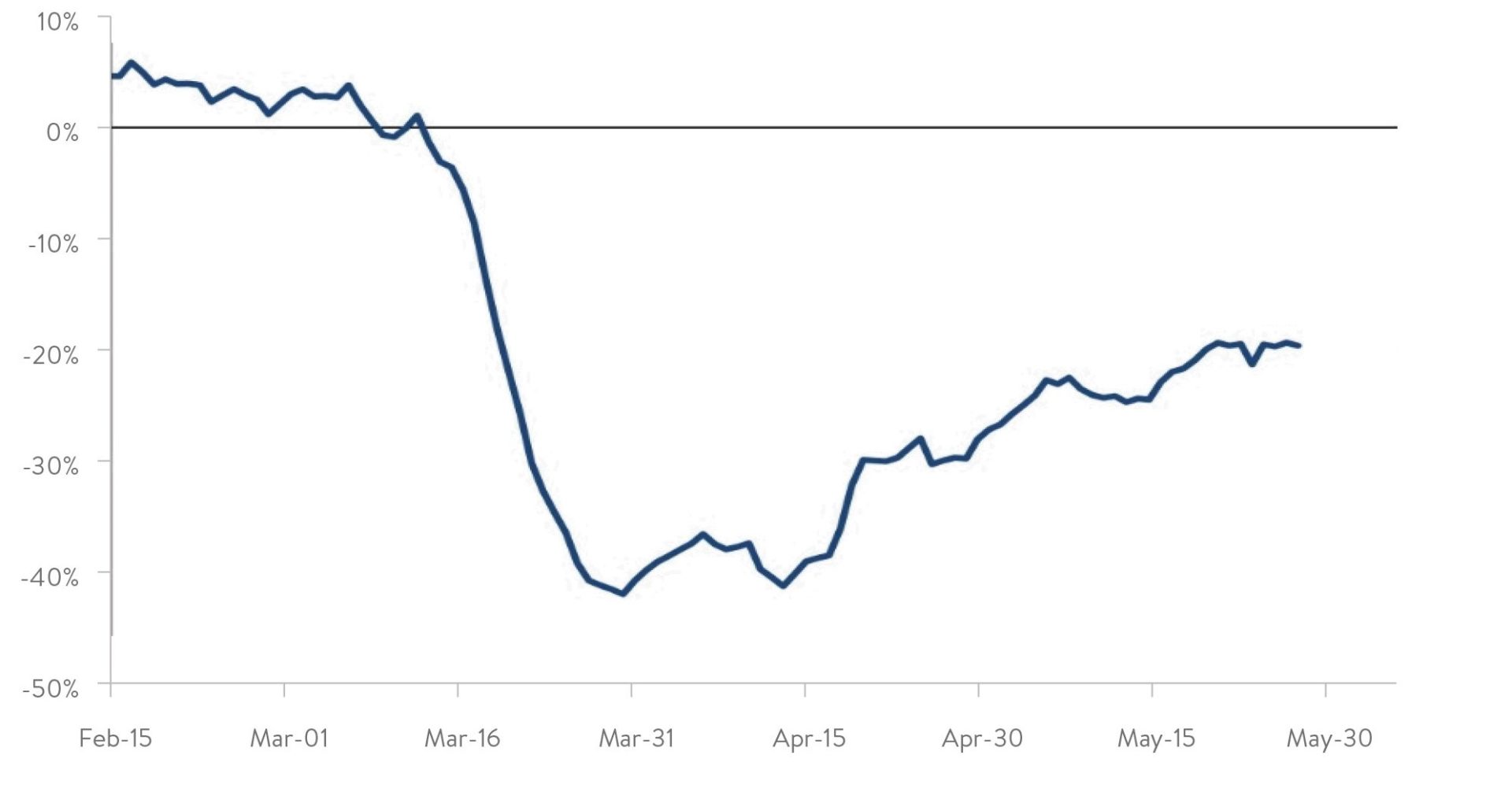

United states, credit and debit card spending

Source: JP Morgan. % change over year-ago in 7-day average of total in nonrecurring catergories

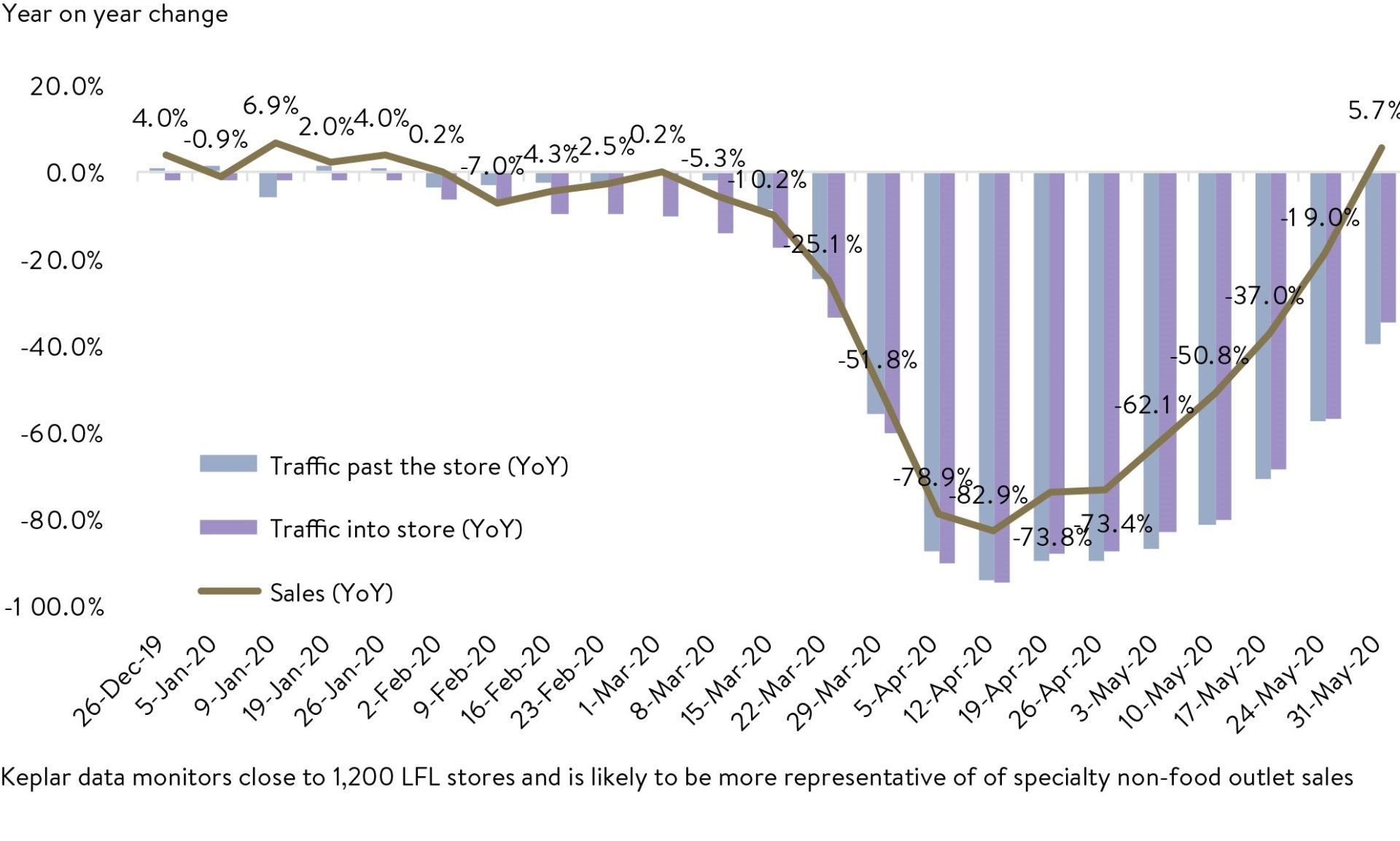

Retail foot traffic into Shopping Centres in Australia

Source: Citi Research, Kepler

We’re finding opportunities in a brave new world

It’s also become clear though that the world we are returning to might look a little different to the one pre-COVID-19. In perhaps a harbinger of things to come, during May Twitter CEO Jack Dorsey announced that all employees that can work from home can do so indefinitely. This was followed by Mark Zuckerberg saying he expected 50% of Facebook employees could be working remotely in the next 5-10 years. Whilst this is no doubt easier for these large tech companies to implement, greater work from home will be one of the enduring trends to result from COVID-19 which will have massive ramifications for many business models.

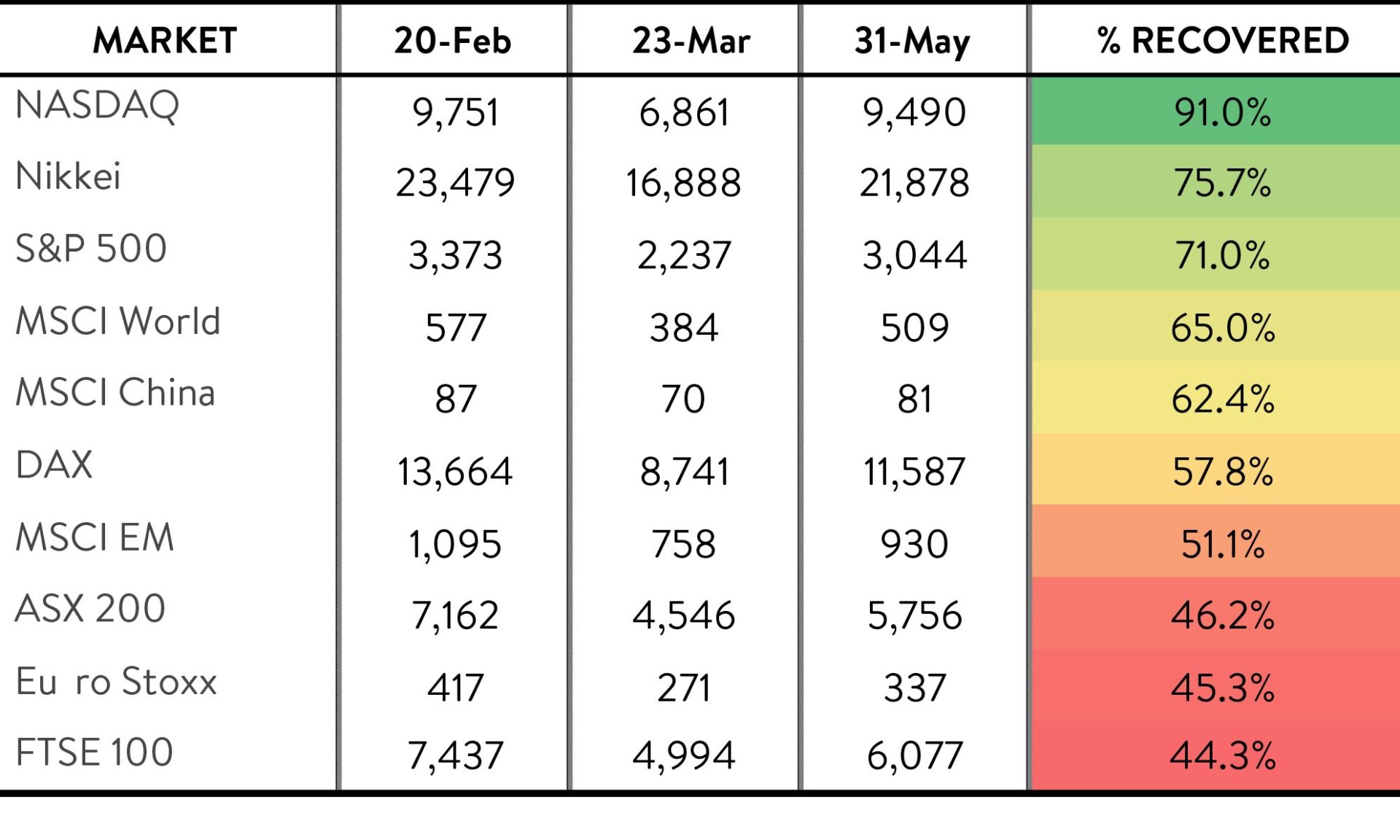

Speaking of tech companies, whilst many aren’t participating in the “return to the office” theme, they are benefiting from what some are calling the “Great Acceleration”, where many things online and e-commerce related are essentially seeing years’ worth of transformation being compressed into months. This tailwind has seen the tech heavy NASDAQ recoup almost all its COVID-19 losses by the end of May (chart below), and in fact in early June reach new all-time highs.

We have been able to benefit from this transformation, particularly in our global equity strategy where opportunities are more plentiful, through exposure to small cap names where we can get an edge and not have to pay the eye watering multiples some large household tech names in the US trade on.

Source JP Morgan. Data to 28th May 2020

Now is a time to be selective

You don’t have to buy the uncertainty that’s inherent in “the market”. We remain happy that we don’t have to play the market timing game and make big bets guessing, and that’s what they ultimately are, whether this rebound has overshot or not.

We are currently being very selective, looking for companies with greater earnings certainty that are less or even positively impacted by COVID-19, have high confidence that they will be able to grow those earnings on a 3-5 year basis, and that are trading at reasonable valuations. Now is not the time to be making bold calls on exactly what the new normal is going to look like for those companies most negatively impacted by COVID-19 now and into the future.

As always, thank you for entrusting your capital with us.

Kindest regards,

Andrew Mitchell & Steven Ng

Co-Founders & Senior Portfolio Managers

Ophir Asset Management

This document is issued by Ophir Asset Management Pty Ltd (ABN 88 156 146 717, AFSL 420 082) (Ophir) in relation to the Ophir Opportunities Fund, the Ophir High Conviction Fund and the Ophir Global Opportunities Fund (the Funds). Ophir is the trustee and investment manager for the Ophir Opportunities Fund. The Trust Company (RE Services) Limited ABN 45 003 278 831 AFSL 235150 (Perpetual) is the responsible entity of, and Ophir is the investment manager for, the Ophir Global Opportunities Fund and the Ophir High Conviction Fund. Ophir is authorised to provide financial services to wholesale clients only (as defined under s761G or s761GA of the Corporations Act 2001 (Cth)). This information is intended only for wholesale clients and must not be forwarded or otherwise made available to anyone who is not a wholesale client. Only investors who are wholesale clients may invest in the Ophir Opportunities Fund. The information provided in this document is general information only and does not constitute investment or other advice. The information is not intended to provide financial product advice to any person. No aspect of this information takes into account the objectives, financial situation or needs of any person. Before making an investment decision, you should read the offer document and (if appropriate) seek professional advice to determine whether the investment is suitable for you. The content of this document does not constitute an offer or solicitation to subscribe for units in the Funds. Ophir makes no representations or warranties, express or implied, as to the accuracy or completeness of the information it provides, or that it should be relied upon and to the maximum extent permitted by law, neither Ophir nor its directors, employees or agents accept any liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. This information is current as at the date specified and is subject to change. An investment may achieve a lower than expected return and investors risk losing some or all of their principal investment. Ophir does not guarantee repayment of capital or any particular rate of return from the Funds. Past performance is no indication of future performance. Any investment decision in connection with the Funds should only be made based on the information contained in the relevant Information Memorandum or Product Disclosure Statement.