As investors, we view bear markets as a natural part of the investment cycle. However we understand that losing capital is never an enjoyable experience and in this article we share our thoughts on how investors can identify the warning signs of an approaching bear market.

As investors, we view bear markets as a natural part of the investment cycle. And while losing capital is never an enjoyable experience, bear markets should not be feared as they tend to present fantastic opportunities to purchase high quality businesses at depressed prices. It is these high quality businesses with strong balance sheets and good management teams that can consolidate their competitive position during these periods and emerge even stronger.

However, during the initial stages of a bear market high quality stocks are likely to see their price fall along with lower quality stocks. It is therefore important for investors to know how to identify the warning signs of an approaching bear market.

Creating a bear market map

Creating a bear market map

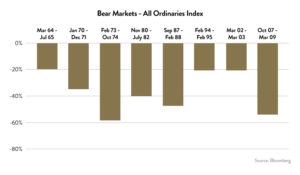

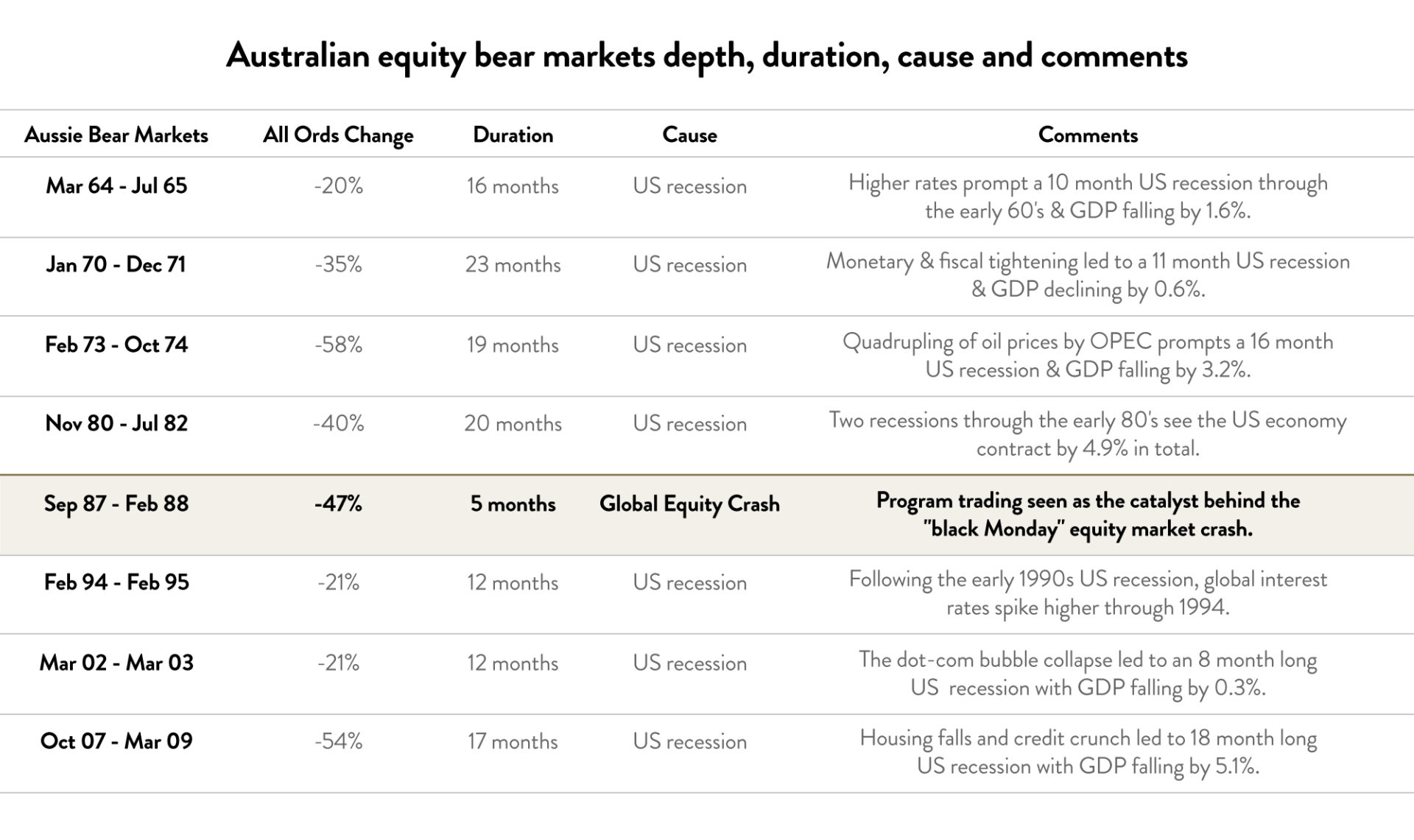

If we define a “bear market” as a peak to trough fall of 20% or greater, we find the Australian share market has experienced eight such periods since 1960. Over this 58-year span, these eight bear markets saw the All Ordinaries index fall on average by 37%, and last for 16 months.

One of the most common and misleading views held on the cause of bear markets is they are a natural product of the preceding bull markets age. This narrative will often be delivered via references to how long the previous or average bull run lasted before ending. Unfortunately for investors, such simple rules of thumb hold little truth. Instead each market cycle is unique, and even though it may already be eight or ten years long, this does not necessarily mean it can not continue for longer!

Unfortunately for investors, such simple rules of thumb hold little truth.

Another widely held misperception is that bear markets are an inevitable outcome from when equity markets just get too expensive. Under this scenario it is thought that as equity valuations get stretched to certain levels the natural forces of the markets will bring about a sharp correction in prices, so these valuations can be brought back to what are considered more “normal” levels. In reality, equity markets can remain expensive for extended periods of time, in the same way that at other points in the market cycle we see stocks remain stuck at low valuations for years on end.

So if neither the length of the preceding bull market, nor high valuations can by themselves be considered drivers of bear markets, what can we use as a guide?

The best signal of a potential bear market for Australian stocks is the health of the US equity market. The clear link here is that bear markets in Aussie equities have always shown themselves to be a by-product of a US equity bear market. In fact, of the eight bear markets we identified in Australia since 1960, US equities fell by an average of 20% through these same periods. What this clearly demonstrates, is that a relationship exists between equity markets such that when the US sneezes, Australia catches a cold.

Given that bear markets in Australian shares are driven by US equity bear markets, the obvious question that follows is, what causes US equity bear markets?

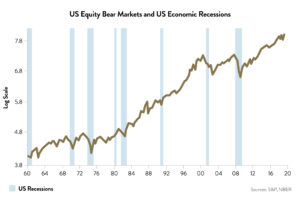

The answer to this is a US economic recession. As shown in the chart below, we can see significant corrections in US equities almost always coincide with a US recession.

The only reason we mention “almost”, is there was one instance when US shares did crash outside of a recession period, with that being the short sharp crash seen in October 1987, commonly referred to as “Black Monday”.

So where are we now?

So we believe that identifying the likelihood of a US economic recession is key in preparing for a bear market in Aussie equities. It follows that we then need to ascertain how close the US economy is to a potential recession.

Currently, we would assign a relatively low probability to the US slipping into recession over the next twelve months. Recessions are almost always a product of monetary policy being tightened too much, in efforts to reign in a credit or capex boom. And although interest rates have been tightened by the US central bank over the last three years, they are still very low by historic standards. The absence of any obvious bubble, combined with very low and stable inflation rates and the recent slowing in the labour market has meant that US authorities are now in a position where they are more likely to cut rates than increase them. In fact, markets are predicting that the Federal Reserve will cut rates two times by the end of the year.

Finally, we would point out that although these traditional bear market flags may not be present now, this doesn’t necessarily mean a bear market is an impossibility. Every market cycle throws surprises which have no precedent, as we are now seeing in the ongoing trade tensions between the US and China.

For us at Ophir this means continually focussing on investing in high quality businesses and waiting for the attractive buying opportunities that will inevitably emerge when the next bear market comes.