The plumbing of global markets

Some of the best businesses in the world are the ones nobody talks about at dinner parties. Toll roads. Pipelines. Stock exchanges. Payment networks.

The common thread is that they sit in the middle of something essential, charge a small fee for every transaction that flows through, and are extremely difficult to dislodge.

They tend to be regulated. They tend to compound quietly. And they tend to be valued accordingly – on premium multiples that reflect the durability of the cash flows.

But every now and then, the market hands you one of these businesses at a fraction of the multiple it deserves.

One is clearing broker Marex (NASDAQ: MRX).

Its shares are trading at a discount to its closest peers simply because the market is failing to appreciate that it is, in essence, a structurally protected, infrastructure-style compounder.

A great business

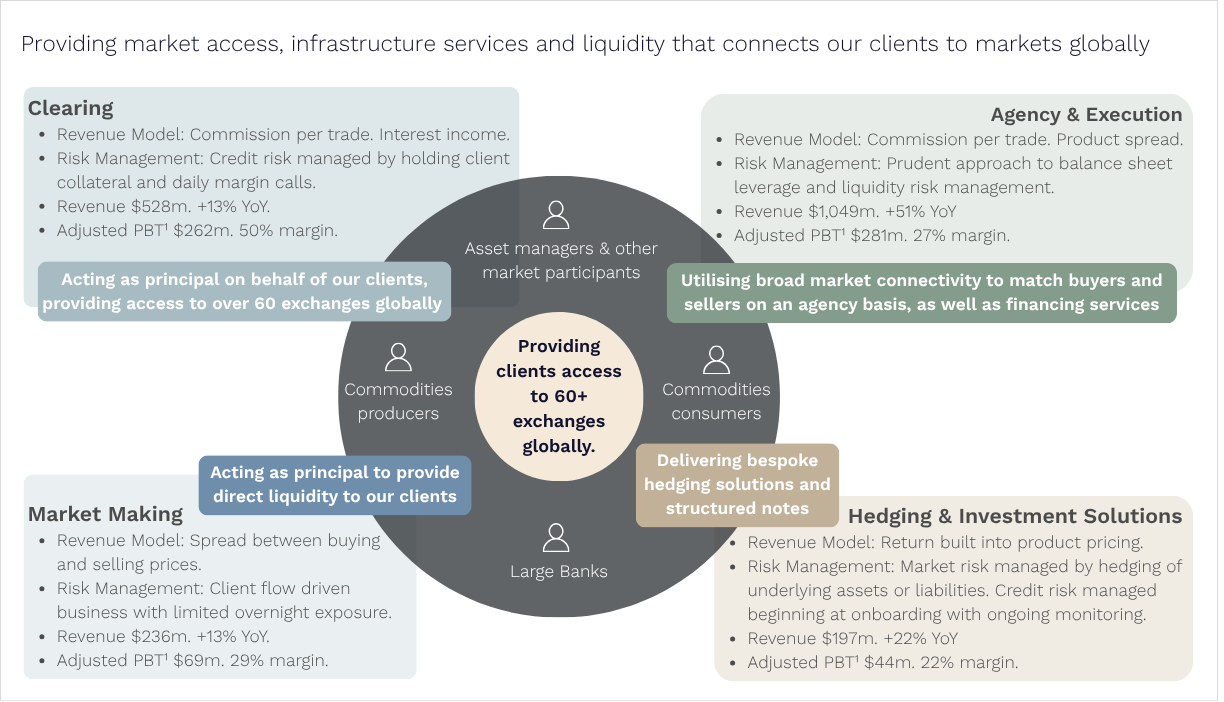

Marex is one of the largest clearing brokers in the world. One of only ~60 Futures Commission Merchants (FCM) globally, it sits in the middle of one of the most essential pieces of financial infrastructure in modern markets.

To understand why Marex is a great business, you need to understand what clearing actually is.

When a hedge fund or an airline trades a futures contract, they don’t trade directly with the exchange. The exchange uses a central counterparty clearing house (CCP) – a regulated utility that becomes the buyer to every seller and the seller to every buyer, mutualising risk across the system. CCPs like Chicago Mercantile Exchange (CME) and Intercontinental Exchange (ICE) charge a fee for this service and trade on premium multiples (around 20x earnings) as they are some of the most prized financial infrastructure in the world.

But CCPs are not allowed to deal with end clients directly. Regulation requires them to be neutral risk utilities, insulated from credit risk. So between the client and the CCP sits a clearing broker – the FCM – that takes on the operational burden, fronts the margin, manages credit, and handles defaults when they occur.

This is what Marex does. They are the firm that absorbs everything the CCP cannot touch.

Source: Marex Investor Presentation, May 2026.

Marex went public in April 2024 when it was the fastest-growing FCM by client assets in the US, and we estimate the company now has more than 10% market share in clearing, up from around 3% in 2022.

Three Structural Tailwinds

But our path into Marex started with a peer and the incredibly strong tailwinds we found for clearing and execution businesses.

We had been doing initial work on StoneX (NASDAQ: SNEX), Marex’s closest listed peer in the US, after StoneX made a transformative acquisition.

We flew to New York to meet with the StoneX team in person and caught up with their management again when they passed through Denver.

Those conversations crystallised something for us: clearing and execution sit in a rare position in financial markets because of three structural tailwinds compounding on top of one another:

- Growth in the underlying market.

Total exchange-traded contract volumes have been growing at a high-single-digit pace for years. That’s happening as more activity migrates from over-the-counter markets into centrally cleared venues, more asset classes get listed, and global hedging needs continue to expand.

- Share gains from the banks.

International banking regulations, Basel III and Basel IV, have made clearing structurally uneconomic for large bank incumbents, compressing their returns and forcing them to retreat or exit entirely. But the clients haven’t gone anywhere. The activity hasn’t disappeared. It is simply migrating from the banks to a small group of specialist non-bank platforms – of which Marex and StoneX are the two largest listed examples. The result has been a long, slow exit by the banks. The number of FCMs globally has fallen from over 300 in the 1990s to around 60 today.

- Consolidation of the fragmented non-bank tail.

The smaller end of the FCM market lacks the technology, capital, and regulatory expertise to compete at scale. The larger specialists – Marex chief among them – are consolidating these books inorganically, improving share, pricing power, and overall market quality in the process.

We usually work hard to find one structural tailwind in most investments. Finding three in the same business is rare.

Building conviction and dispelling doubts

But the more we worked on the sector, the more obvious it became that Marex was the best-positioned name in the space. For a start, it had the highest-quality earnings mix. In a normal quarter, around 80% of group profit comes from the most defensible parts of the value chain: clearing and execution. StoneX had a much smaller weighting to clearing and execution.

Marex also had the best technology platform and the most disciplined M&A track record. Ian Lowitt, the CEO, has built Marex over more than a decade through a combination of disciplined organic growth and a series of well-executed acquisitions. Each acquisition was made at attractive an valuation (often at or below tangible book value) and integrated onto the group’s single global technology platform.

Yet trading on less than 10x forward earnings, Marex had the lowest multiple of its peer group.

Why was Marex’s multiple so low?

One reason was a short-selling report published in August 2025 by short-selling research firm, NINGI Research. Titled ‘A Financial House of Cards’, the report alleged accounting irregularities, off-balance-sheet entities, and conflicts tied to the CEO’s prior career. Marex fell sharply when it was published.

If anything, however, the report helped us. It gave us a discounted entry point and a clear set of bear points to stress-test.

We concluded the short thesis lacked substance and started buying Marex in October 2025.

We went through every claim in the short report ourselves, then with sell-side analysts, then with the company directly. Marex publicly rebutted the report twice. S&P Global Ratings reviewed the allegations and affirmed Marex’s BBB- rating with a stable outlook.

Fantastic financial results

On the morning of their investor day in late March, we caught the red-eye from Denver to New York. Arriving early, we were the first non-Marex person in the conference room and were able to spend time one-on-one with the entire senior management team before the other investors and brokers arrived.

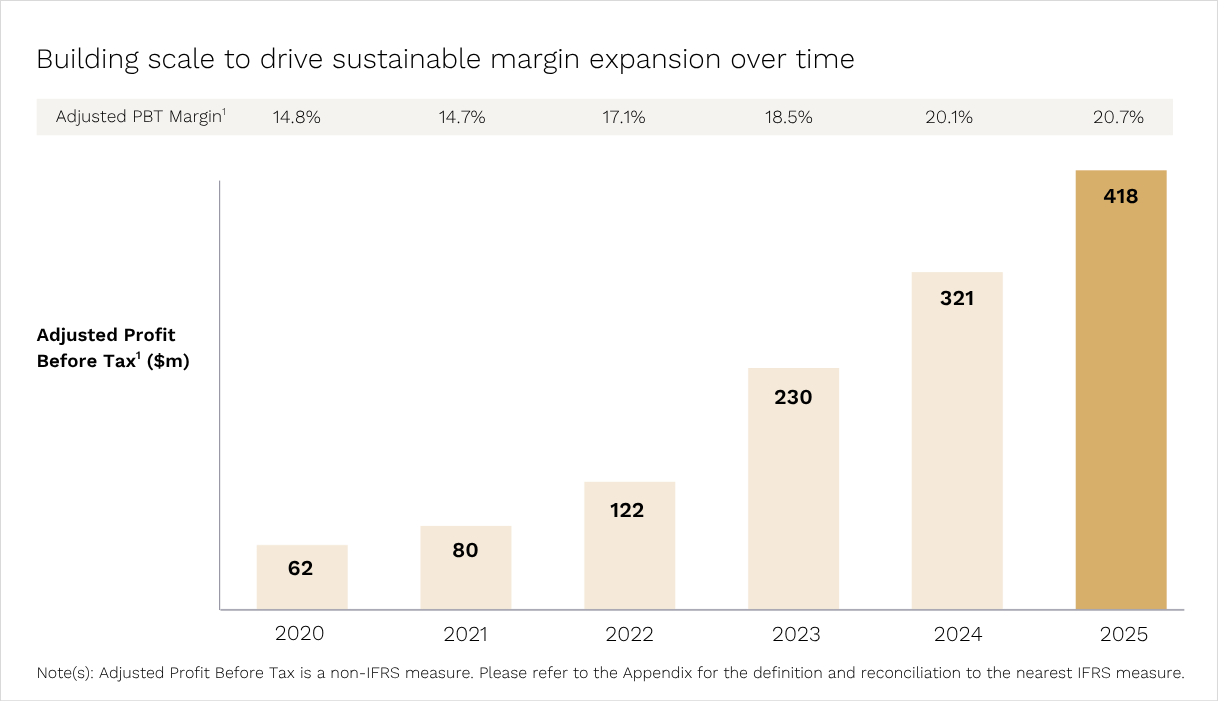

And, importantly, Marex continues to report record financial results.

Adjusted profit before tax has compounded from US$62 million in 2020 to US$418 million in 2025 – a compound annual growth rate of 47%. (Growth was 30% in 2025 alone.) Adjusted EPS came in at $3.99 for 2025, beating consensus by 4.4%.

Source: Marex Investor Presentation, May 2026.

Marex’s recent Q1 2026 result was another record:

- Revenue was $692 million, up 48% year-on-year.

- Adjusted profit before tax of $153 million, rose 59% year-on-year.

- The result was comfortably above the top end of the guidance the company had provided just six weeks earlier at its investor day.

This was achieved despite absorbing a $34 million loss from a single client default in natural gas trading in January – a useful, real-world demonstration that the business is built to take occasional shocks without breaking.

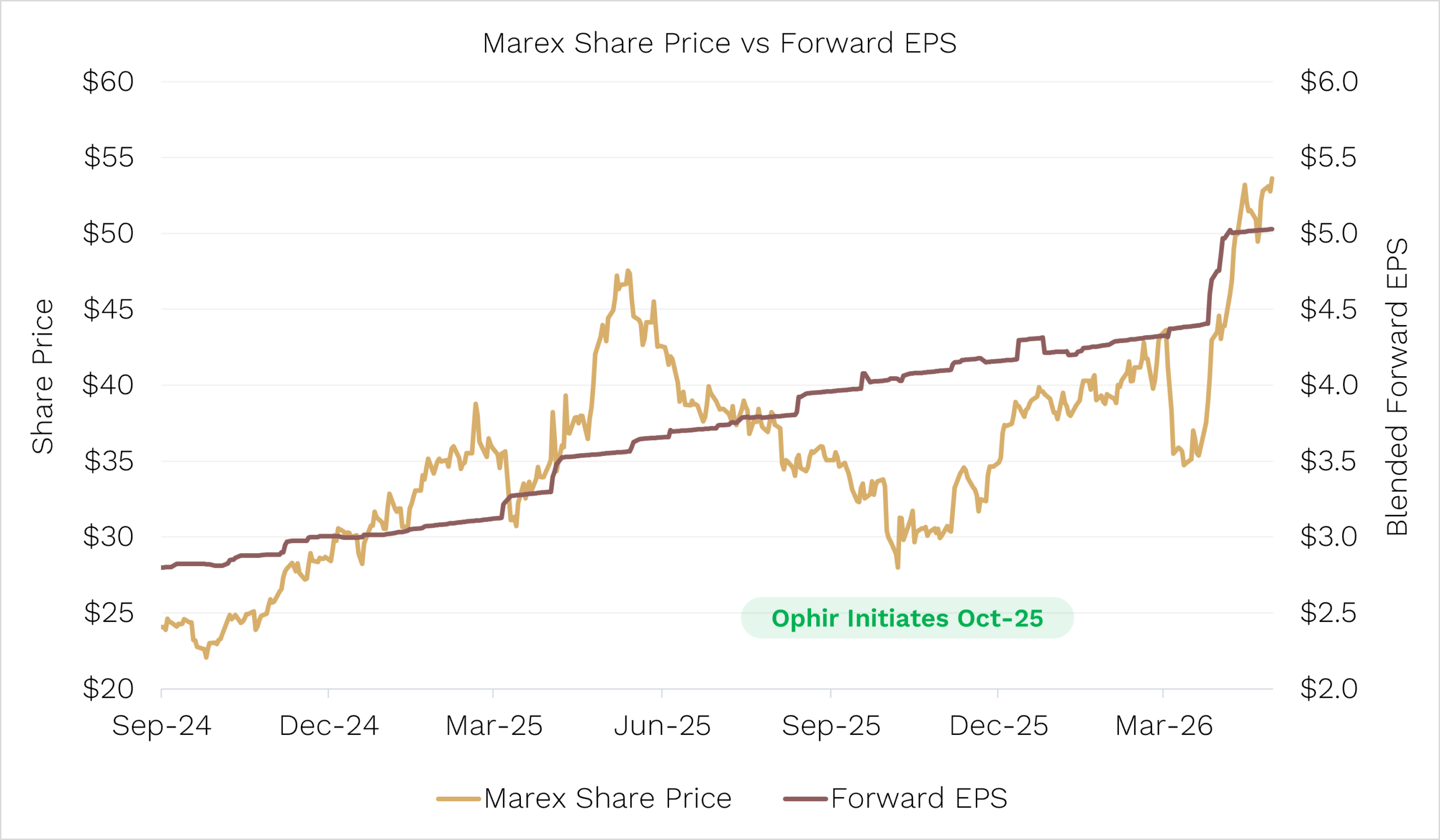

Source: Ophir. Bloomberg data as at 30 April 2026.

The big misunderstanding

Yet despite this strong financial performance and the debunking of the short report, Marex still trades on 10x earnings.

At the heart of this mispricing is an ongoing misunderstanding of what Marex does.

The market is treating Marex as a cyclical commodities broker – grouping it with low-multiple names like Virtu, TP ICAP and BGC.

But, as we saw above, a meaningful portion of Marex’s earnings behaves like infrastructure.

Those earnings are underpinned by sustained sequential growth in its clients’ clearing balances, as well as growth in the market volumes in total contracts cleared. What’s more, its Prime Services business continues to deliver outsized market growth.

CCPs, such as CME and ICE, trade on around 20x forward earnings. Interactive Brokers (which partly overlaps Marex) trades on 32x.

Given Marex sits between a clearing utility and a prime broker, we don’t think it deserves the premium multiples of the likes of CCPs and Interactive Brokers. But we don’t think it deserves to trade like a low-quality commission broker either. (Even StoneX, the closest direct comparison, trades on ~19x.)

Why Marex Fits This Environment

In a market consumed by the AI debate – where every software business is being asked whether its cash flows are durable at all – Marex is the opposite kind of investment.

It is a regulated, mission-critical piece of financial infrastructure. Its moat is created by Basel rules, CCP access caps, and post-2008 clearing mandates – not by software, brand, or distribution.

It benefits from volatility rather than being threatened by it. And the structural shift driving its growth (banks exiting clearing, activity migrating to non-banks) has years left to run.

It is, in short, the kind of compounder that doesn’t need a benign macro to work. It just needs the plumbing of global markets to keep flowing – and that, increasingly, runs through Marex.