Building with surgical precision

PDF

Have you ever had a family member rushed into emergency surgery for an aortic dissection? Then you’ll know it’s one of medicine’s most terrifying experiences.

The aorta – the body’s largest artery – carries blood from the heart to the rest of the body. When it tears, every minute counts.

Treating these conditions requires some of cardiac medicine’s most complex and high-value surgical procedures. And behind many of those procedures sits a company most investors have never heard of: Artivion.

Artivion (NYSE: AORT) is a ~US$1.8 billion medical device company headquartered near Atlanta, Georgia, focused exclusively on aortic disease.

Their product portfolio spans four key areas: aortic stent grafts, the On-X mechanical heart valve, surgical sealants (BioGlue), and implantable human tissues. They sell into more than 100 countries worldwide.

We’ve been deeply engaged in Artivion for several years and believe the company is in the middle of a multi-year, product-led growth phase that will extend to the end of the decade.

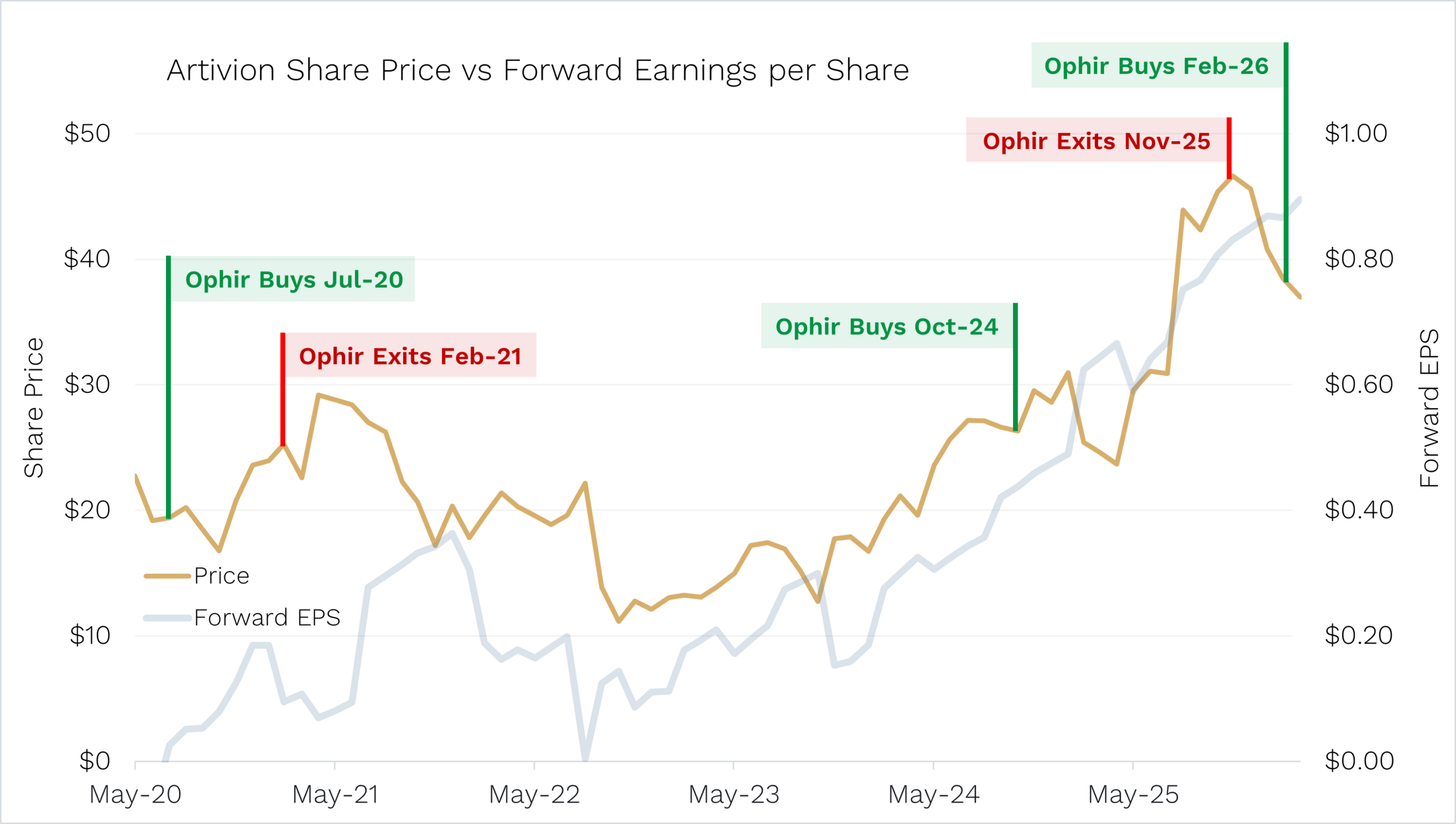

The recent pullback in the stock – down roughly 25% from its November 2025 highs – has allowed us to re-enter (we first bought pre-COVID then sold at the 2025 highs) at a valuation that is deeply mispriced.

Finding Artivion … and Pat

We first discovered Artivion on a trip to Atlanta in early 2019 when visiting several companies. During that visit, we met with Artivion’s CEO, Pat Mackin.

Pat explained how he had spent over a decade at Medtronic, one of the largest medical device companies in the world. His last role was Senior Vice President presiding over the Cardiac Rhythm division – at the time, Medtronic’s largest business unit.

Pat joined what was then CryoLife (the company rebranded to Artivion in 2022) because he saw a big opportunity: building a company focused solely on the aorta.

By concentrating on the cardiac surgeon customer base, and with a single, focused sales force selling several product families to a large total addressable market (TAM), Artivion could gain significant operating leverage.

What we saw was a company with a market cap of sub-US$1 billion and revenues of sub-$250 million, run by an extremely high-quality manager who had left a $5 billion business segment because he believed he could not only compete with it, but beat it and take meaningful share.

At the time, the company had just two analysts covering it.

It was one of the clearest value creation stories we had encountered.

A Decade Assembling a Comprehensive Aortic Portfolio

When we first met Pat in early 2019, he had been at the company a little over four years and had already begun materially reshaping its portfolio.

He sold several non-core products and, through a series of acquisitions and partnerships that now form the backbone of Artivion’s product roadmap, he’d started realigning the business exclusively toward the aorta.

Between 2016 and 2020, there were four key strategic moves:

- The first major move was the acquisition of On-X Life Technologies in January 2016 for ~$130 million. That brought the On-X mechanical heart valve into the portfolio and strengthened the company’s presence in aortic valve replacement.

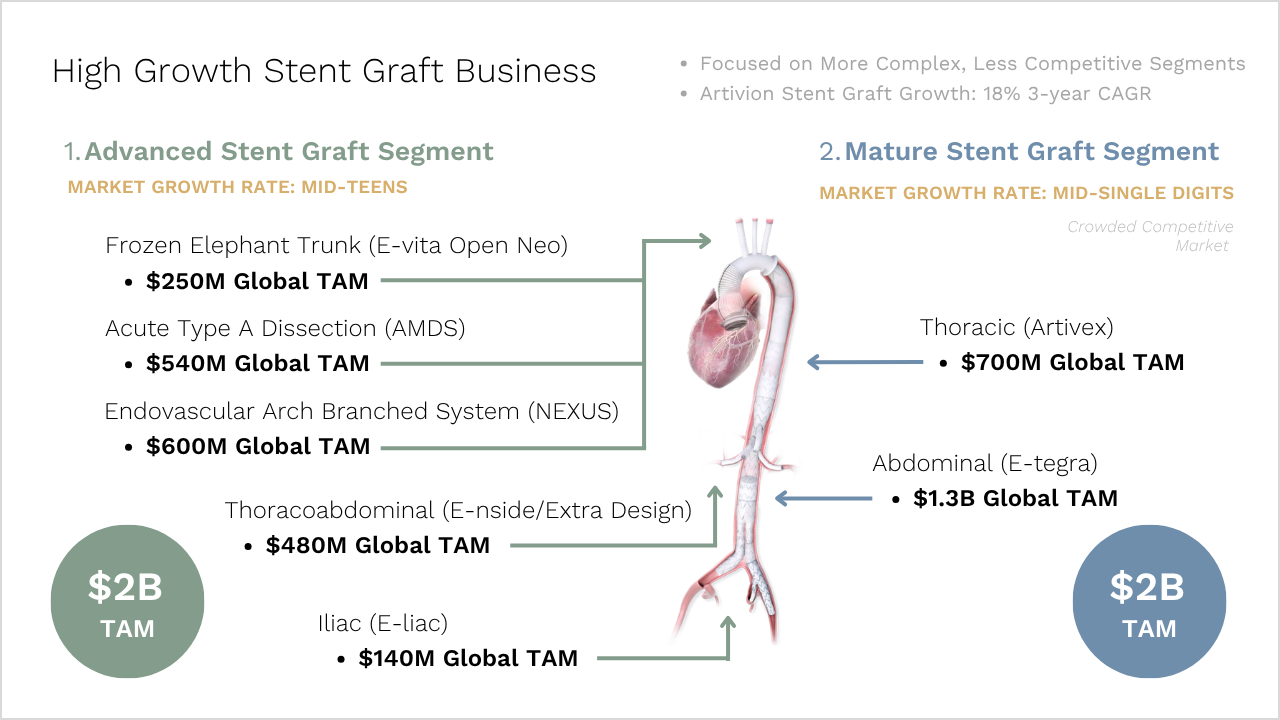

- The following year, in December 2017, came the pivotal deal. In a ~$250 million transaction, Artivion bought JOTEC, a German developer of advanced endovascular stent grafts (minimally invasive surgery to repair an aneurysm). This gave Artivion immediate access to the ~$2 billion global stent graft market and significantly expanded its minimally invasive aortic capabilities.

- Then in 2019, Artivion entered a strategic partnership with Endospan for the NEXUS aortic arch stent graft system – a catheter-based solution for total endovascular repair of the aortic arch (which supplies blood to the brain, head and arms).

- And in 2020, the company acquired Ascyrus Medical for up to $200 million, bringing into the portfolio the AMDS (Ascyrus Medical Dissection Stent) – a hybrid prosthesis designed to remodel the aortic arch in acute Type A aortic dissections.

Pat played a huge role in creating this value. These were competitive processes where he would personally fly out to close deals – including on public holidays and family vacations – to make sure Artivion was the successful bidder against larger, better-capitalised peers.

The result is a comprehensive aortic portfolio – spanning open surgical, endovascular, hybrid, and valve solutions – that now tracks from the heart down to the bottom of the aorta in the most complex, high-value areas of aortic surgery.

Source: Artivion Corporate Overview February 2026.

New Products Set to Accelerate Growth

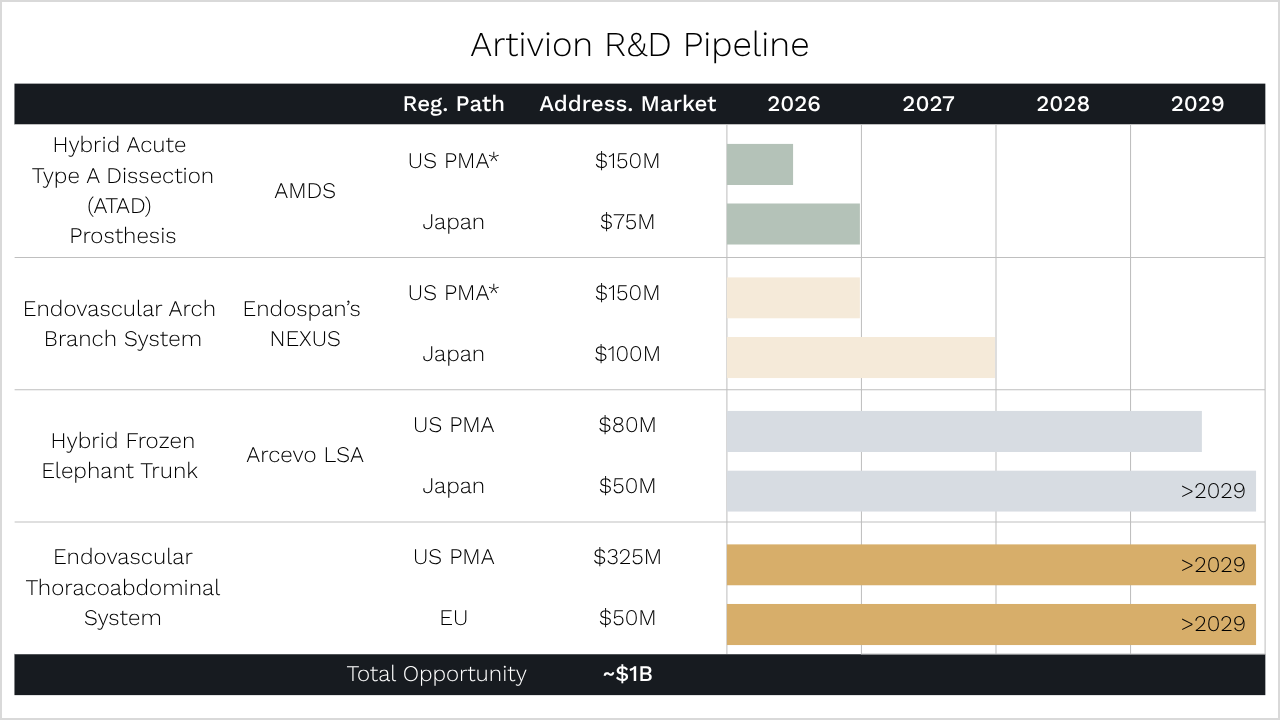

Artivion is particularly compelling now because its new products are set to accelerate growth.

Nearly $500 million of new TAM is opening up in the next 12–18 months through key products, AMDS and NEXUS.

Source: Artivion Corporate Overview February 2026.

These are not speculative launches. Both products have already been used in Europe with CE Marking approval (which allows products to be sold in the European Economic Area). That gives us a high degree of confidence in their clinical profile. The risk here is regulatory timing, not clinical efficacy.

Meanwhile, On-X continues to compound. It has grown at double digits for over a decade and now represents almost 20% of the business. New clinical data has demonstrated a mortality and reoperation benefit in patients aged 65 and over compared to bioprosthetic valve (made from animal tissue) alternatives. That effectively opens a new $100 million annual US market that Artivion can pursue.

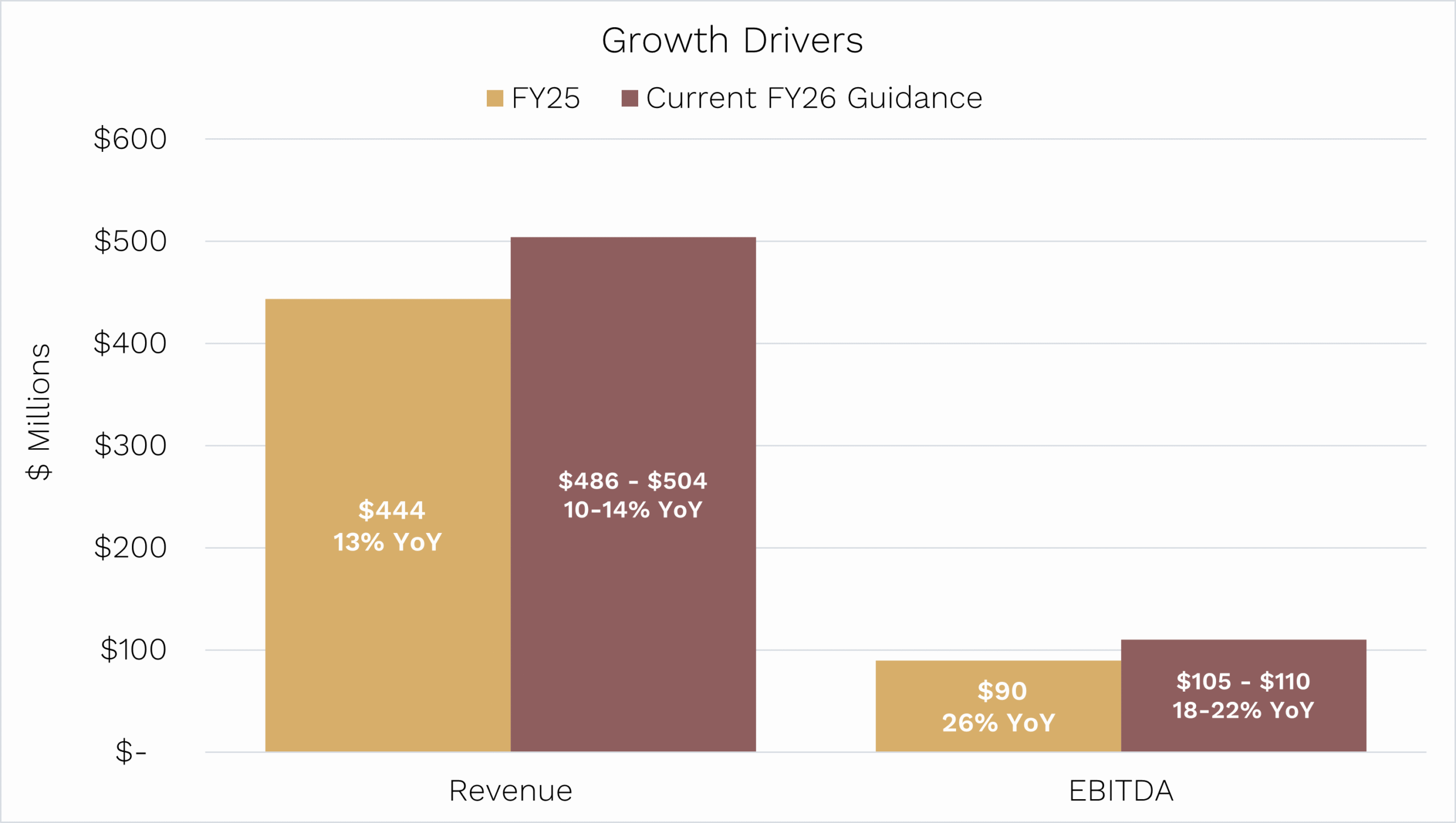

For the full-year 2025, Artivion delivered $444 million of revenue (13% adjusted constant currency growth), $90 million of adjusted EBITDA (26% growth). For 2026, the company has provided guidance of revenue of $486–504 million and adjusted EBITDA of $105–110 million.

Source: Artivion Corporate Overview February 2026.

Stent grafts represent approximately $200 million, or 40% of Artivion’s revenue today. This segment grew 44% year-on-year in Q4 2025 (36% on a constant currency basis).

We believe the upcoming product launches can facilitate a ~25% compound annual growth rate (CAGR) in revenue for stent grafts over the next three years, which in turn means the company can deliver double-digit growth at the group level through the end of the decade.

The Edge: Dozens of Conversations with Cardiologists

What has given us added confidence in Artivion is that we have spoken to dozens of cardiologists based in the US and Europe regularly over the past two years, as well as pre-COVID when we first invested.

This gave us a strong sense of new product adoption, competitive positioning against larger peers, and emerging technologies.

We’ve also spoken directly with ex-sales reps and competitors over the years.

The cardiologists are key.

Their sentiment toward Artivion continues to be very positive, and awareness is growing, which will facilitate higher product cross-selling in the future.

The concentrated nature of the cardiac surgeon customer base means that word-of-mouth and clinical evidence travel fast. That dynamic favours a company with differentiated products and a dedicated sales force.

Materially Mispriced

Despite this strong market position and mid-20% EBITDA CAGR outlook, Artivion currently trades on mid-teens EBITDA.

We think that is materially mispriced.

Additionally, trading at ~3.5x sales, the company will likely attract acquisition interest from a larger peer at 5–7x sales given the attractive and relatively low-risk growth rates, large TAMs, and high potential synergies from duplicative sales forces. That implies significant upside from current levels.

The stock has pulled back from its November 2025 highs on a combination of conservative management guidance into a year of elevated capex (~$50 million, up from $39 million) and outsized funding requirements for earn-outs.

Last year, the market did get ahead of itself and priced in an acceleration of product-led growth into 2026. But when the timeline reverted to the original 2027 trajectory, the share price gave back those gains.

Still, for us, this was the opportunity because the fundamental thesis hasn’t changed, and we have been able to buy a high-quality, accelerating growth story with over 20% three-year EBITDA CAGR at a ~50% discount to standard sector takeout multiples.

Source: Ophir. Bloomberg.

Exactly what we are looking for in this environment

Artivion is exactly the kind of name we’re drawn to right now: a medtech compounder with product-cycle driven growth, limited GDP sensitivity, and a valuation that reflects neither the clinical pipeline nor the margin expansion runway.

It doesn’t need a resolution to the AI debate to work. It doesn’t need rate cuts. It doesn’t need a benign tariff outcome.

It just needs its products to keep performing – and so far, they are.