By Andrew Mitchell & Steven Ng

Co-founders and Senior Portfolio Managers

In our October 2021 Letter to Investors we take a deep dive into the topic of “portfolio turnover” at Ophir. That is, the how, what, when and why of the changing, or turning over of, positions in our funds.

Dear Fellow Investors,

Welcome to the October Ophir Letter to Investors – thank you for investing alongside us for the long term.

Major equity markets turned the corner posting gains in October, following September’s sharp selloff, with most indices at or near all-time highs to end the month.

Short-term interest rates and longer-term bond yields have returned to the fore as key variables for share markets, as major central banks start thinking about winding back their ultra-accommodative programs they put in place during the COVID-19 crisis.

During the month, the ASX Small Ords (+0.9%), S&P 500 (+7.0%), Nasdaq (+7.3%), MSCI Europe (+4.7%) and Russell 2000 (+4.3%) generated positive returns while the ASX200 (-0.1%) detracted slightly from performance.

In the prior month in September, the U.S. stock market took a major hit with the S&P 500 (-4.7%), Nasdaq (-5.3%) and Russell 2000 (-3.0%) detracting significantly from performance. In October however, U.S. markets took a big leap forward and recovered all its losses from September.

October 2021 Ophir Fund Performance

Before we jump into the letter, we have included below a summary of the performance of the Ophir Funds during October. Please click on the factsheets if you would like a more detailed summary of the performance of the relevant fund.

The Ophir Opportunities Fund returned +1.7% net of fees in October outperforming its benchmark which returned +0.9% and has delivered investors +26.1% p.a. post fees since inception (August 2012).

Download Ophir Opportunities Fund Factsheet

The Ophir High Conviction Fund investment portfolio returned -0.1% net of fees in October, underperforming its benchmark which returned +0.6% and has delivered investors +20.4% p.a. post fees since inception (August 2015). ASX:OPH provided a total return of -2.0% for the month.

Download Ophir High Conviction Fund Factsheet

The Ophir Global Opportunities Fund returned -0.6% net of fees in October, underperforming its benchmark which returned +0.2% and has delivered investors +37.1% p.a. post fees since inception (October 2018).

Download Ophir Global Opportunities Fund Factsheet

Turning to the U.S. economy and developed markets more broadly, we are cognisant of inflation pressures driven by significant bottlenecks in the supply chain which is hampering the global recovery. These supply chain problems have been exacerbated by a surge in consumer spending through COVID-19 and now the ‘revenge spending’ phenomenon as people are freed from extended periods of lockdown. We are closely observing when these issues get resolved as this should alleviate a lot of the upwards pressure on inflation.

The macro remains as tough to pick as ever though and we are eternally grateful our long-term performance isn’t primarily determined by what’s happening to “big picture” factors like interest rates, monetary or fiscal policy, government edicts or commodity price swings. But rather we are reliant on being able to find the next up and coming businesses both here and offshore that can grow and take market share no matter the influence of these top-down impacts.

For those in the macro game though, showing how tough it can be, another big scalp was taken recently with London based macro hedge fund manager Russell Clark of RCIN shutting the doors after a series of bearish market bets over the years went against him as markets surged – forcing him to hand back the little remaining capital he had to investors.

This excerpt from his final recent letter to investors is instructive about the challenges macro investors face:

“This is why I am returning capital. Markets have now become a political choice. US markets are essentially a bet on the Fed unable to raise rates, and congress unable to regulate big tech or raise corporate tax rates. Commodity markets have now become a bet on Chinese policy objectives, and currencies have become a bet on what Chinese policy objectives are too.

Give me an economic problem, then I can properly gauge risk. Give me a Chinese political problem – I am taking a guess as much as the next person. Did I think Alibaba was going to fall 50% this year? No, not until the Chinese government told me to think that way. Is Alibaba a good short now? I have no idea, and like everyone else will have to wait to see what the Chinese government says.

So, I think it time to step back, have a think about where we are going, and then come back when I can see an opportunity for my skill set. Perhaps that’s never, but I doubt it. The only constant in life is change.”

Clark uses macro-economic analysis to bet on stocks. We appreciate his honesty, from the fundie who was born and raised locally in Canberra before making it big overseas.

We can’t help but have sympathy for the difficulty in trying to add value through this type of analysis given the hundreds of thousands of professional investing eyeballs parsing the macro-economic data each day.

We remain as content as ever, meeting with company management, customers, suppliers, competitors etc to get a better understanding of our prospective small cap portfolio companies. It’s an approach that for us seems a far easier and fun way to spend our time and put our, and our investors’, capital to work.

For the rest of this Letter to Investors, rather than diving deeper into the machinations of markets over the last month, we thought we’d take a step back. Instead, we’d like to provide you deeper insight into the topic of ‘portfolio turnover’ here at Ophir. That is, the how, what, when and why of the changing, or turning over of, positions in our funds.

We hope you enjoy, and it provides a little more insight into the day-to-day activities we undertake on your behalf with your investments.

You’ve got to know when to hold ‘em, Know when to fold ‘em

Insight into Ophir’s portfolio turnover

You’ve no doubt heard these classic lyrics from one of Kenny Rogers’ hit songs at some point in your life. For one of your writers, their first memory comes from hearing it repeatedly at a local Uni bar as one of the last songs of the night back in the 90s. This usually meant it was time to go home!

“You’ve got to know when to hold ’em

Know when to fold ’em

Know when to walk away

And know when to run”

The song was Rogers’ most famous hit and one of five consecutive no.1 Billboard country music chart-toppers for the Texan crooner.

Of course, Rogers was singing about a game of cards, but the words could equally apply to managing a share portfolio.

Imagine a share you own has just gone up 20% on the day of its latest earnings announcement because it ‘beat’ earnings expectations and it raised its profit outlook. Should you continue to ‘hold ‘em’?

Or what if one of your key portfolio positions has just tanked 30% after a poor earnings update at its latest AGM. Should you ‘fold ‘em’? Or perhaps should you even run?!

Many investors who put some of their life savings with a fund manager want to know what the manager’s ‘portfolio turnover’ might be. That is, does the manager hold positions in companies for a very long time, happy to look through any short-term bumps in the road, resulting in low turnover? Or are they more active, trying to make every post a winner, changing weights of stocks in the fund frequently, or perhaps selling out entirely and introducing new companies at a more rapid pace – racking up higher turnover?

Who cares about portfolio turnover?

Well, trading costs money. You don’t see it turn up in the management expense ratio, which is what the fund manager charges you. But it does come out of the investors’ assets – going to brokers for buying and selling companies. For professional investors, this can often cost anywhere from 0.1-0.3% of the value of the stock traded.

Source: New Yorker

There is a well-known and very funny book called ‘Where are the Customers’ Yachts?’ on this very topic. It’s about a visitor to New York who admired the boats of the wealthy stockbrokers, but couldn’t understand why their clients didn’t have their own luxurious boats.

Author, Fred Schwed Jr, starts the book with:

Once in the dear dead days beyond recall, an out-of-town visitor was being shown the wonders of the New York financial district. When the party arrived at the Battery, one of his guides indicated some handsome ships riding at anchor. He said,

“Look, those are the bankers’ and brokers’ yachts.”

“Where are the customers’ yachts?” asked the naive visitor.

It’s sometimes argued fund managers don’t have an incentive to keep transaction costs from portfolio turnover low as they are not the ones that directly bear the cost. This may be true to a degree, but not at Ophir.

Remember, we have all our investable wealth in the Ophir funds, so we care greatly about transaction costs from buying and selling and the resultant portfolio turnover. We’ll only trade if we have high conviction that it will add value, AFTER costs.

How you can have 100% turnover but still own the same stocks as a year ago

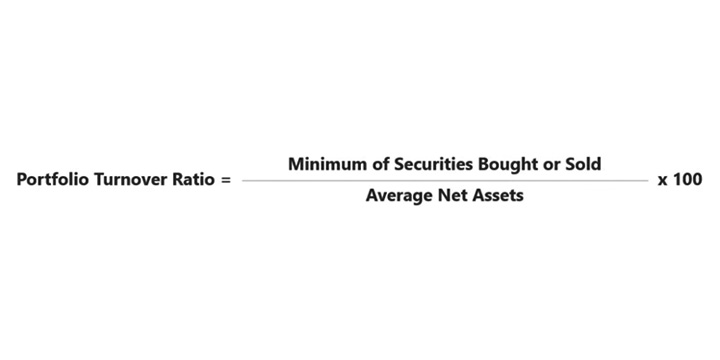

Portfolio turnover happens any time a stock is bought or sold, either partially or in full.

The generally accepted formula for how a fund manager’s portfolio turnover is calculated is below.

So, if you bought $12 million of stocks and sold $10 million during the year, whilst the average fund value was $10 million, then your turnover would be 100%.

Some say this is the same as having a whole new line-up of stocks in the portfolio on the 31st of December, compared to a year ago on the 1st of January. But this is not strictly true.

As well as FULL buy and sells (that introduce new and remove old stocks from the portfolio), the buys and sells include PARTIAL buy and sells (otherwise known as re-weighting of positions).

So technically it’s possible to still hold the exact same stocks at year-end as the beginning, and still have 100% portfolio turnover, from very active reweighting of positions (though this would be incredibly rare!).

For equity funds, low turnover is generally regarded as less than 20-30% p.a. Whereas high turnover is often thought of as above 80% p.a.

Is high turnover bad?

If you’re cost-conscious, you might immediately think that a high portfolio turnover is bad because more transaction costs are subtracted from your assets – only enriching the brokers and funding their next luxury yacht. But that is not the full story. If the transactions add more value than their cost, then they should be executed.

Academics haven’t helped us much. The evidence from their research is mixed as to whether high portfolio turnover adds or subtracts from net investment performance on average.

Digging a little deeper, though, and what you generally find is that the best performing high-turnover equity funds outperform the best-performing low turnover funds, but the worst also do worse. So, get it right and the potential gains may be higher, but get it wrong and the downside is also greater.

You also find that, on average, high turnover funds don’t last as long. But this is just the poor-performing high-turnover funds going out of business because they underperform the worst-performing low-turnover funds.

Would Kenny go disco? Your fund type and turnover

For investors, one way to check if a manager is behaving “true to label” is whether their portfolio turnover is in line with their investing style. Just as you expect Kenny Rogers to keep churning out country hits, you might get a little worried if he tried to reinvent himself with a new dance floor anthem!

On the low turnover end are passive index tracking funds. Here for example, Vanguard’s S&P500 tracking funds typically have turnover as low as 3-4% p.a. as they are basically just buying and holding the index constituents and only changing them when the index (infrequently) changes. If you find out your passive index tracking fund has turnover of greater than 30% p.a. – that’s a massive red flag!

Amongst active managers, next up is usually “Value” style managers with a long-term investment horizon that seek to buy more mature undervalued businesses and wait for the market to realise they were previously selling cheaper than they should have.

More “Growth” orientated managers usually have a higher turnover as they seek out more rapidly growing businesses that are more likely to be sold once growth slows or is replaced by the next high growth company.

Overall, active style equity funds on average typically have turnover around 60-100% p.a. but with a wide variety to be found outside these ranges. For example, for some hedge funds or highly active high octane quantitative style equity managers, turnover over 500% p.a. can often be found!

Revealing our hand. What’s our turnover at Ophir?

So that brings us to what you’re all here for. Where do Ophir’s funds sit on the turnover spectrum and what does it say about how we are managing your money?

The best gauge of the turnover at Ophir is our longest-running fund, the Ophir Opportunities Fund, which has been going for a little over nine years.

Its turnover is close to 100% p.a. on average, over the long term, which on face value is high compared to many other active equity managers. About 40% of this turnover though has been from FULL buys or sells – that is, new stocks entering the portfolio or old stocks being sold in full. The other 60% results from partial buys and sells, or in other words, reweight existing positions based on our analysis and changes in our conviction levels.

The 40% of turnover resulting from full buys or sells means that the average holding period of a stock in our original Ophir Opportunities Fund is about 2.5 years. Now that’s an average. Sometimes we hold positions in companies for as little as a few months, but sometimes for longer than 5+ years. It is not something that is predetermined. Ultimately, turnover is an output of our investment process and it depends on how long it takes, if at all, for the market to realise the value we see in the companies we hold.

If we discover an undervalued business that is growing quickly, and the market fully realises that value at its next earnings result in a few months’ time, then we may recycle that capital into the next idea that has bigger upside.

Alternatively, if the market only partially realises the value, then we may continue to hold if we see further big gains ahead. Again, turnover is an output, not something we target ahead of time.

So, in sum, we are quite active, and more active than most. We would be worried if turnover went down significantly because it would probably mean that we weren’t finding as many new ideas to keep the expected return of our funds high. But remember, much of our activity is also making sure we have the position sizing right for the conviction levels we have in our holdings. As George Soros once said:

“It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right, and how much you lose when you’re wrong”.

In funds management, position sizing is not everything, but it is almost.

Do our different Ophir funds have different turnover?

In short yes. Ranking our Ophir funds from highest turnover to lowest over time goes something like this:

Global Opportunities Fund > Ophir Opportunities Fund > Ophir High Conviction Fund.

- The Global Opportunities Fund tends to have higher turnover given the larger opportunity set (about a 20 times bigger investment universe than the Ophir Opportunities Fund), which means there are more ideas, as well as quarterly financial reporting in the US which provide more ‘scoreboards’ for the market to hopefully realise the value we have seen in our companies.

- Next up is the Ophir Opportunities Fund which has a higher turnover, on average, than the Ophir High Conviction Fund because of its smaller-cap, higher-growth bias and higher stock count which means that positions tend to be changed more frequently.

- The lowest turnover of the Ophir funds is the High Conviction Fund, which, with its more concentrated nature and more limited investment universe, tends to have slightly lower turnover compared to the Ophir Opportunities Fund.

What causes our turnover to change

Whilst 100% p.a., on average, is a good yardstick to keep in mind for turnover of the Ophir funds over the long term, it can and does change significantly from year to year.

What causes it to change? Many things, but mostly the number of new ideas we have for the funds at any one point in time and the performance of existing positions.

Turnover highly correlates with performance. When performance is high, turnover tends to be high. And causation runs both ways here. That is, if we have a high number of new ideas, then we are frequently selling existing positions to fund those ideas with higher expected returns. At the same time, if those higher returns bear out, then we are more likely to either sell some of them for risk management purposes, so they don’t represent too much of the portfolio, or they have met their price target and we are recycling the capital into new ideas to keep the expected return of the fund high.

Turnover also tends to increase during significant market events. A classic recent example is March last year when COVID-19 first hit. We reshaped our portfolios to take account of the new reality that faced economies, companies and markets, using the price volatility in shares to buy those that were oversold as fear gripped markets. Likewise, when effective vaccines news hit the airwaves in November last year, it required meaningful portfolio readjustments as the starter’s gun was fired on an eventual return to some form of normality.

An example of higher turnover has been the Global Opportunities Fund in recent years, where its very high performance and COVID-19 related re-shuffling saw turnover significantly higher than 100% pa at different times. We think its turnover is likely to trend down as hopefully no more COVID-like events are around the corner anytime soon (!) and abnormally high performance moderates somewhat (though we’d be quite ok if it doesn’t!).

When we fold. The four factors that trigger us to sell a stock

When talking about portfolio turnover we must also mention the four main triggers that cause us to sell a stock.

1. Earnings snag

The first, and certainly the most worrying trigger, is when the earnings trajectory of the company seems to have hit a snag and no longer has us as excited. It’s worrying because this is what we hang our hat on when doing our due diligence on businesses, i.e., we are highly confident they are growing faster than the market thinks. We are going to get some companies wrong though, that is life, business is risky. Things come out of the blue and even smack the (hopefully) most informed person on the business, the CEO, in the face. But we need to make sure that when these shocks happen that they are infrequent, small and we limit their impact by having a lower portfolio weight.

2. Overvalued

The second reason we sell is when a stock just becomes too expensive. Not every company, no matter how wonderful or how quickly it is growing, makes a great investment. It can be too expensive. Or in other words, it can be factoring in too rosy a future. Plus, if you are wrong on the earnings trajectory, as above, at least you won’t be compounding it too much if you are continually trimming the expensive flowers.

3. Thesis change

The third, and probably our biggest pet peeve of the bunch, is when the investment thesis changes for a stock. That is, we were holding it for one reason, but that reason no longer exists and we, or another analyst in the team, have found another reason to keep holding the position. This is an automatic sell for us. If we’ve lost our edge on the original reason the company was a ‘buy’ for us, then we shouldn’t be hanging around for another reason just to justify inaction.

4. Something better

And lastly, but probably the most frequent reason for selling, is simply we have found something better. If a new company is growing more quickly, trading at a cheaper valuation than one of the lowest conviction positions in the fund, then there is a good chance it will be out with the old and in with the new. Fresh ideas are the lifeblood of funds management and help ensure that new investors to the Ophir funds stand a chance of receiving returns as good if not better than those who have been with us for years.

Why we won’t cut turnover to minimise tax

One of the side effects of portfolio turnover is its impact on distributions from managed funds, including our own. The higher your turnover, the more likely you are to generate realised gains or losses. And if you are getting it right, your gains will handsomely outstrip your losses over time.

Typically, equity managed funds must distribute realised capital gains every year to investors for tax purposes. All else equal then, a higher turnover fund will have to distribute more of its return to investors.

We sometimes have investors who are disappointed to receive a significant annual distribution from our funds comprised of realised gains – given many must pay tax on those gains, depending on their investment entity. Whilst we very much understand where these investors are coming from (no one likes to pay more tax than they need to, including ourselves) we are reminded that a wise man once said:

“No one went broke paying taxes!”

If we didn’t sell when we thought it appropriate, just to avoid generating these realised gains, we’d ultimately provide lower total returns in our funds and incur more risk. Or in other words, we’d be cutting off our nose to spite our face. We never want to have the ‘tax tail’ wag the ‘investment dog’.

We can assure you both of us face a stiff marginal tax rate on our holdings in the Ophir funds. We also naturally have many investors in our funds with all manner of different marginal tax rates they face depending on which vehicle they invest through, from 0%, all the way up to the top marginal tax rate.

The one thing we can assure you is that we and the team are working our hardest every day to ensure we are providing the best investment return to you without taking undue risk.

We will remain quite active in our approach, as it has served us well in the past, and strongly believe it will continue to in the future.

As always, thank you for entrusting your capital with us.

Kindest regards,

Andrew Mitchell & Steven Ng

Co-Founders & Senior Portfolio Managers

Ophir Asset Management

This document is issued by Ophir Asset Management Pty Ltd (ABN 88 156 146 717, AFSL 420 082) (Ophir) in relation to the Ophir Opportunities Fund, the Ophir High Conviction Fund and the Ophir Global Opportunities Fund (the Funds). Ophir is the trustee and investment manager for the Ophir Opportunities Fund. The Trust Company (RE Services) Limited ABN 45 003 278 831 AFSL 235150 (Perpetual) is the responsible entity of, and Ophir is the investment manager for, the Ophir Global Opportunities Fund and the Ophir High Conviction Fund. Ophir is authorised to provide financial services to wholesale clients only (as defined under s761G or s761GA of the Corporations Act 2001 (Cth)). This information is intended only for wholesale clients and must not be forwarded or otherwise made available to anyone who is not a wholesale client. Only investors who are wholesale clients may invest in the Ophir Opportunities Fund. The information provided in this document is general information only and does not constitute investment or other advice. The information is not intended to provide financial product advice to any person. No aspect of this information takes into account the objectives, financial situation or needs of any person. Before making an investment decision, you should read the offer document and (if appropriate) seek professional advice to determine whether the investment is suitable for you. The content of this document does not constitute an offer or solicitation to subscribe for units in the Funds. Ophir makes no representations or warranties, express or implied, as to the accuracy or completeness of the information it provides, or that it should be relied upon and to the maximum extent permitted by law, neither Ophir nor its directors, employees or agents accept any liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. This information is current as at the date specified and is subject to change. An investment may achieve a lower than expected return and investors risk losing some or all of their principal investment. Ophir does not guarantee repayment of capital or any particular rate of return from the Funds. Past performance is no indication of future performance. Any investment decision in connection with the Funds should only be made based on the information contained in the relevant Information Memorandum or Product Disclosure Statement.