By Andrew Mitchell & Steven Ng

Co-founders and Senior Portfolio Managers

In this month’s Letter to Investors we focus on the recent underperformance of the Ophir funds and look back to late 2016 and early 2017 when our funds experienced similar levels of underperformance. We also discuss the recent yield curve inversion in the US and what this could mean for the global economy and share market returns.

Dear Fellow Investors,

Welcome to the March Ophir Letter to Investors – thank you for investing alongside us for the long term.

Markets climb the wall of worry in March as recession risks increase

After a meaningful pullback in February after the outbreak of war in Eastern Europe, markets across the globe were much more sanguine in March.

Investors were left somewhat surprised that with a worry list that just keeps growing, the major indices logged such a positive month. The order list of the major markets during the month went something like this, with the Nikkei (+5.7%), S&P 500 (+3.7%), Nasdaq (+3.5%), Russell 2000 (+1.2%) and MSCI Europe Index (+1.0%) all finishing well in the green. Australia kept up its ‘lucky country’ moniker being in the right place at the right time for the second month in a row with the ASX 200 and ASX Small Ords returning +7.0% and +5.5% respectively – boosted by its exposure to buoyant commodity prices as a result of supply concerns stemming from the war.

During March, the Federal Reserve raised interest rates by 0.25%, signaling the start of an aggressive rate hiking cycle. More interest rate hikes are expected to occur throughout the rest of 2022 in the US and this continued to be a drag on performance for Growth stocks vs. Value stocks in the small cap part of the US market and for the Australian share market overall. The Russia/Ukraine conflict continued and with the endgame still unclear, share market participants are closely watching inflation numbers as supply chains continue to be disrupted and commodity prices move broadly higher. The Energy sector was the standout performer globally during the month as share prices rose alongside key energy prices such as oil and gas.

During the month we witnessed shorter term US government interest rates (2year bonds) move temporarily higher than longer term interest rates (10 year bonds) in the US. This phenomenon, known as an “inversion” of the yield curve, can be a very earlier predictor of an impending US recession. As the famous line from the movie Titanic goes, is an “iceberg – dead ahead”?.

March 2022 Ophir Fund Performance

Before we jump into the letter in more detail, we have included below a summary of the performance of the Ophir Funds during March. Please click on the factsheets if you would like a more detailed summary of the performance of the relevant fund.

The Ophir Opportunities Fund returned 5.6% net of fees in March, outperforming its benchmark which returned 5.3%, and has delivered investors +23.7% p.a. post fees since inception (August 2012).

Download Ophir Opportunities Fund Factsheet

The Ophir High Conviction Fund investment portfolio returned 6.5% net of fees in March, outperforming its benchmark which returned 6.2%, and has delivered investors +15.7% p.a. post fees since inception (August 2015). ASX:OPH provided a total return of 7.7% for the month.

Download Ophir High Conviction Fund Factsheet

The Ophir Global Opportunities returned -7.2% net of fees in March, underperforming its benchmark which returned -2.3%, and has delivered investors +21.5% p.a. post fees since inception. (October 2018).

Download Ophir Global Opportunities Fund Factsheet

Yield curve inverts – be alert but not alarmed

Why are investors so worried about this so-called yield curve inversion in the US?.

Historically is has been a good predictor of a recession following in 12-18 months’ time. The logic generally goes like this: yield curves invert with higher shorter term interest rates than longer term ones when central banks are rapidly increasing short term interest rates to cool an overheating economy. They often have to take short term rates so high to fight rising inflation that it throws the economy into recession.

Will it happen this time in the US? No one knows for sure. There are some reasons to believe this time might be different such as:

- The yield curve has since un-inverted very quickly.

- Many other parts of the yield curve (outside of the 2yr and 10yr portion) haven’t inverted.

- The after inflation ‘real’ yield curve has not inverted with short term real yields still very low providing stimulus to the economy.

- Other metrics on the health of the US economy still point to reasonably strong growth ahead.

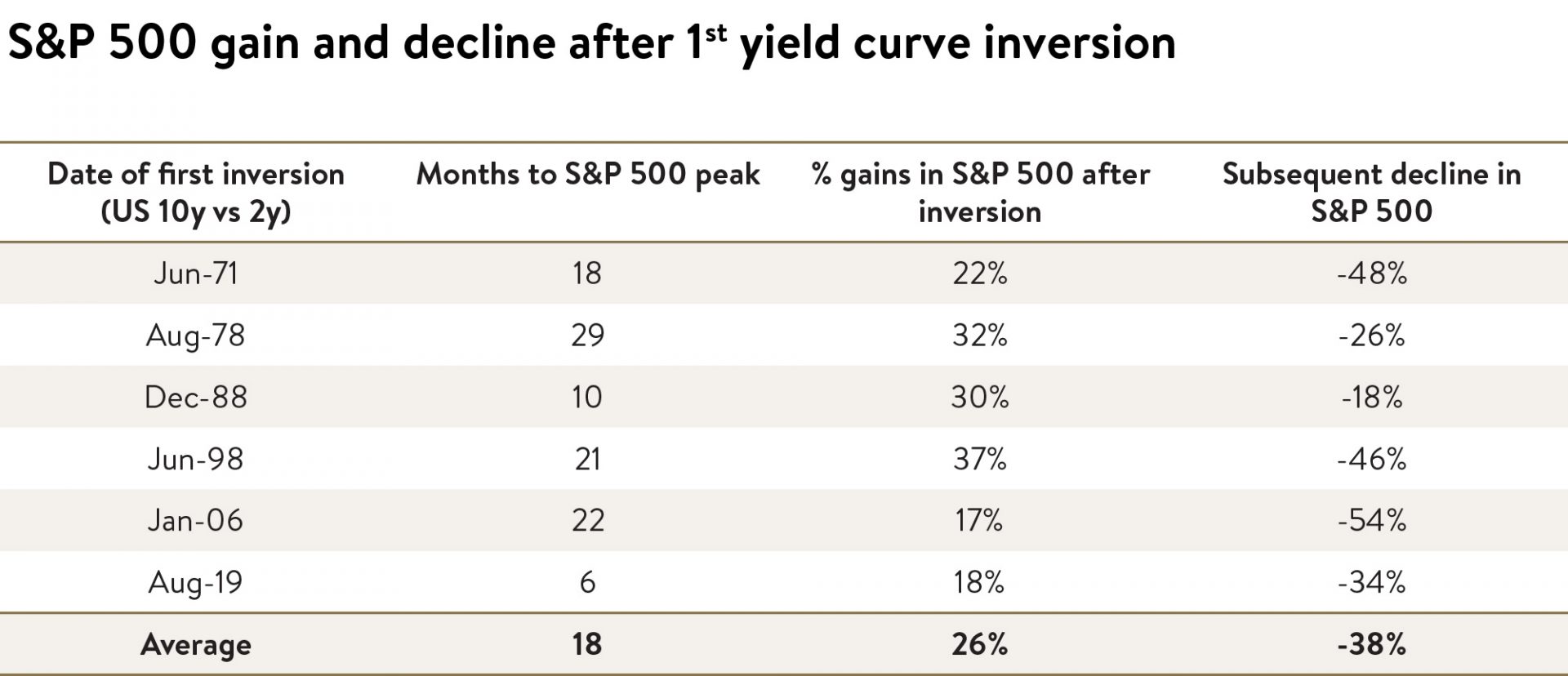

Ultimately time will tell but we think investors should be alerted (not alarmed) by this as share markets have typically continued to deliver good returns for 12-18 months after an inversion.

We show this in the table below where on average the S&P500 has gone on to make 26% gains over the next 18 months before hitting a peak after yield curve inversion.

Near term returns have often remained strong post an inverted yield curve

Source: Ophir. Data as of 31 March 2022. ^Net performance after fees and including reinvestment of distributions calculated using the net asset value of the Fund. Inception dates: Ophir Global Opportunities Fund – October 2018, Ophir

Source: MST Marquee

If you wanted further evidence that going to cash after yield curve inversion is a bad idea, then you only have to turn to those powerhouse finance academics who studied it – Fama and French. In their recent 2019 paper they found:

“We find no evidence that inverted yield curves predict stocks will underperform Treasury bills (cash) for forecast periods of one, two, three and five years”.

So, in the near term, we probably, at least in so far as history suggests, can expect reasonable returns ahead. And one of the reasons is typically yield curve inversion happens because shorter term interest rates are moving higher due to the economy performing better than average. And that is certainly part of the reason why the Federal Reserve in the US is starting to normalise interest rates now.

Ophir fund performance – reverting to the long term trend

Our fellow investors will know that returns of the Ophir funds of late have underperformed their benchmarks. Whilst never pleasant to experience, particularly when that underperformance is combined with negative absolute returns, it can be expected from time to time as part of the long term investing journey.

You may have heard us say that our internal investment return target is 15% per annum (after fees) over the long term which is over rolling 5 year periods.

Why?

Well over the long term almost all that matters is earnings growth and that’s what we focus on day to day at Ophir and what we believe we have an edge in analysing compared to the market. But over shorter periods of time, and like right now, what’s happening in the macro environment can drive markets.

As seen below, long term performance of the Ophir funds has been around or above that 15% pa target net of fees (since inception figures are listed to the right of the lines).

Ophir Funds – Long Term Performance

Date as at 31 March 2022. Ophir performance figures are net of fees. Chart above represents the net return on $100,000 invested in the Ophir Opportunities Fund when it was established in August 2012. For illustrative purposes, the Ophir High Conviction Fund has been added to illustrate the net performance of the High Conviction Fund assuming an investment of equal size as the Opportunities Fund investment at the Fund’s inception date (August 2015). For illustrative purposes, the Ophir Global Opportunities Fund has been added to illustrate the net performance of the Global Opportunities Fund assuming an investment of equal size as the High Conviction Fund investment at the Fund’s inception date (October 2018). It is noted that past performance is not a reliable indicator of future performance.

Back in June last year our Global Opportunities Fund had generated a 79.1% (net) return over the previous year and 45.1% pa (net) since inception. Those were numbers we were never going to keep up indefinitely. Remember Buffett has done 20.1% pa since 1965 and we’d be happy to approach anywhere near that longer term!

Pull backs in equity fund performance are painful but normal and are a necessary part of the journey. We cover this topic in detail in this month’s latest Investment Strategy Note. Eventually the macro winds won’t blow so forcefully, and we will return to a stock picker’s market.

Interestingly, despite the outsized underperformance of late of the Global Opportunities Fund, it is still outperforming both Ophir Australian funds since its inception.

Global and Aussie fund performance diverges in March

Normally, from month to month, given the same investment team and process sits behind each of the Ophir funds, performance tends to be somewhat similar or at least move in the same direction.

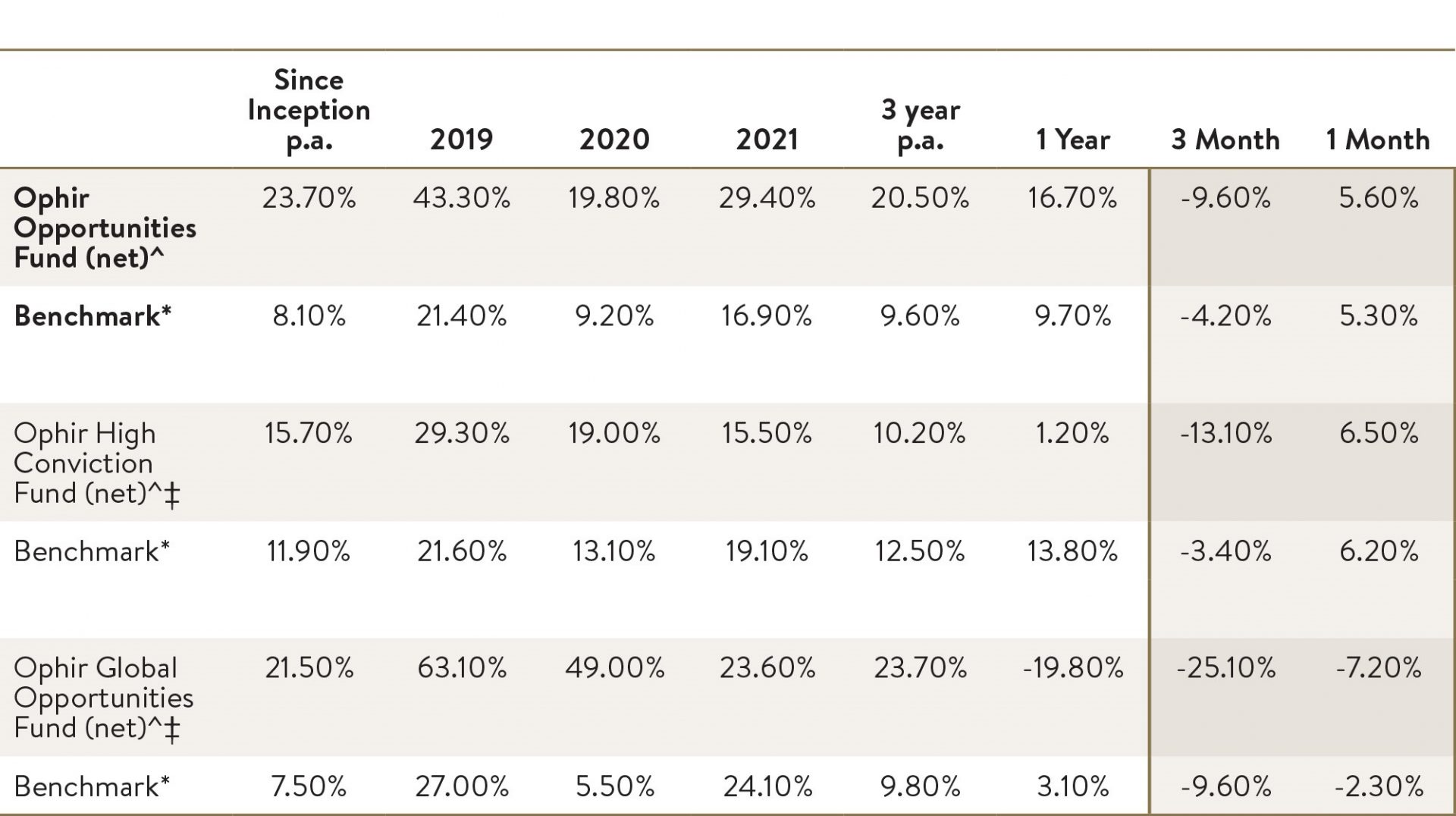

March was different. The Global Opportunities Fund materially underperformed both Ophir Australian equity funds (see table below).

Ophir Strategies – Performance to 31 March 2022

Source: Ophir. Data as of 31 March 2022. ^Net performance after fees and including reinvestment of distributions calculated using the net asset value of the Fund.

There are three key reasons for this:

- Currency -the Global Opportunities Fund reports its performance in Australian dollars but holds investments in foreign currencies – primarily the US dollar and the Euro. The AUD appreciated 3% and 4.5% respectively against the USD and EUR during March which reduced performance by circa 3.5% to 4%.

- The global small caps market in general materially underperformed Australian small caps by about 4% to 5% in local currency terms.

- The portfolio companies in our Australian funds held up better during the month despite the underperformance of ‘growth’ style businesses again in small caps. This was assisted by the takeover offer for Uniti Group (ASX:UWL).

On the first point, currency will sometime be a tailwind and sometimes a headwind to performance of the Global Opportunities Fund. There are no reliable forecasts of currency movements in the short term however over the long term we like the unhedged foreign currency exposure in the Fund. This is because during ‘risk off’ environments the Australian dollar tends to fall (as commodity prices fall), providing a buffer or hedge to the AUD returns of the Global Opportunities Fund. This was evident during March 2020 quarter when markets fell as COVID first spread, seeing the AUD fall -13% versus the USD.

We’ve been here before, in 2016/2017

If you were to just look at our long-term performance numbers for each of the Ophir funds you may think we have never had material pullbacks in performance or benchmark underperformance before. That is simply not true!

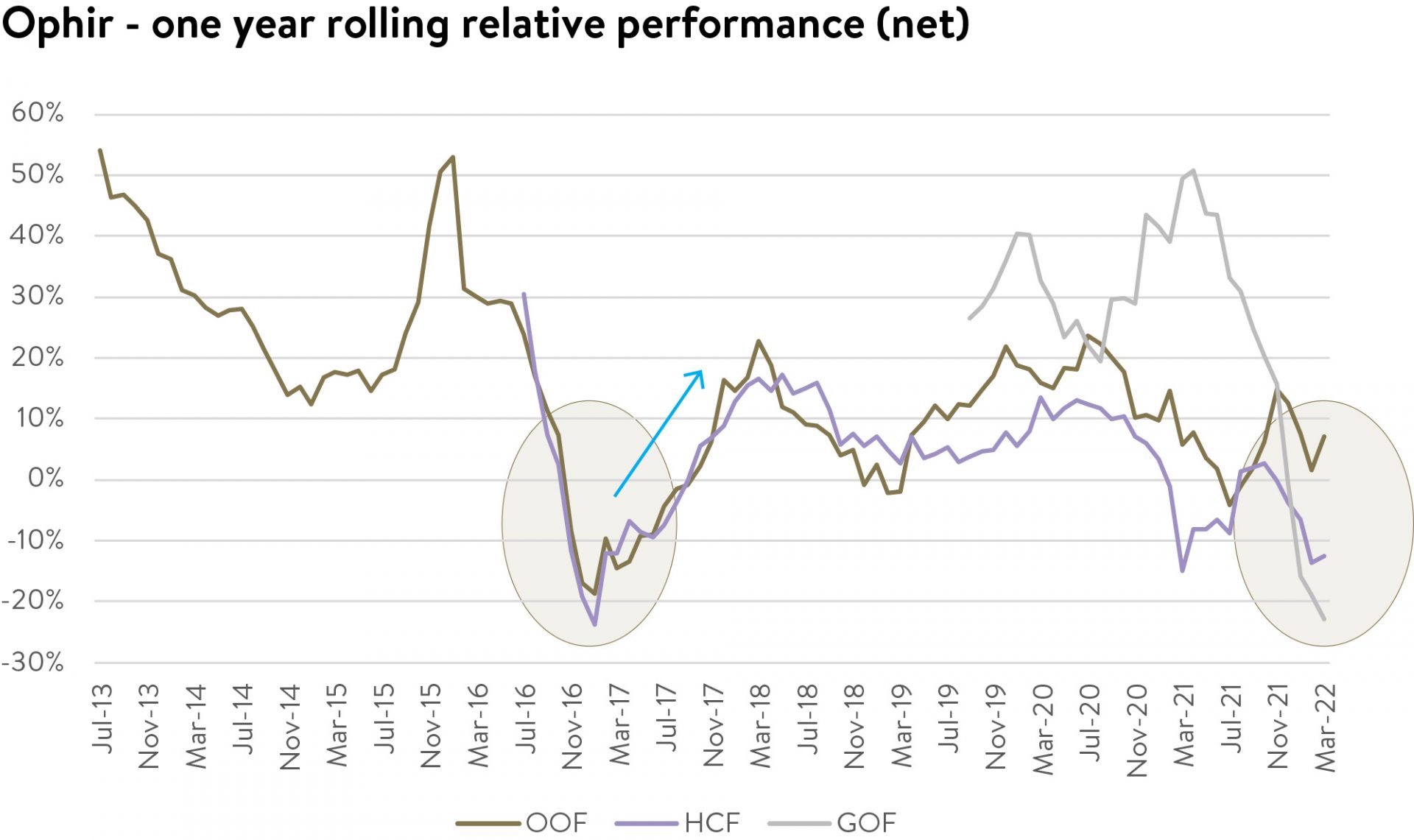

In the below chart we show the 1 year out or under performance of each Ophir fund, compared to its relevant market benchmark, since its inception date.

You can see that 1 year outperformance has generally been positive but not always. Back in late 2016 and early 2017 we had similar levels of underperformance in our Australian funds to what we are experiencing currently in our Ophir High Conviction Fund and Ophir Global Opportunities Fund. This previous period had some similar characteristics as the current period. That is, above trend global growth and rising inflation with the US central bank starting to engage in a more serious rate hiking cycle. This saw sharp outperformance of more ‘value’ and cyclical orientated businesses that we tend to invest less in. A similar cause for our current underperformance. This historic period was followed by a return to significant outperformance later in 2017 and 2018.

We’ve been here before

Source: Data as of 31 March 2022.

We fully expect to have shorter term periods of underperformance on the journey to achieving our 15% per annum (after fees) return target over the long term. As we have stated before, this is not a bug, but a feature of the path to achieving higher long-term returns (please click HERE for link to our Investment Strategy note on the percentage of top performing managers that have short term periods of underperformance).

Valuations supportive for small cap companies as we focus on not overpaying

One of the reasons why we are so bullish on the outlook for returns over the next 5 year period is the starting point now for valuations in global and Australian small caps. Lower starting valuations create a more fertile hunting ground for finding bargains.

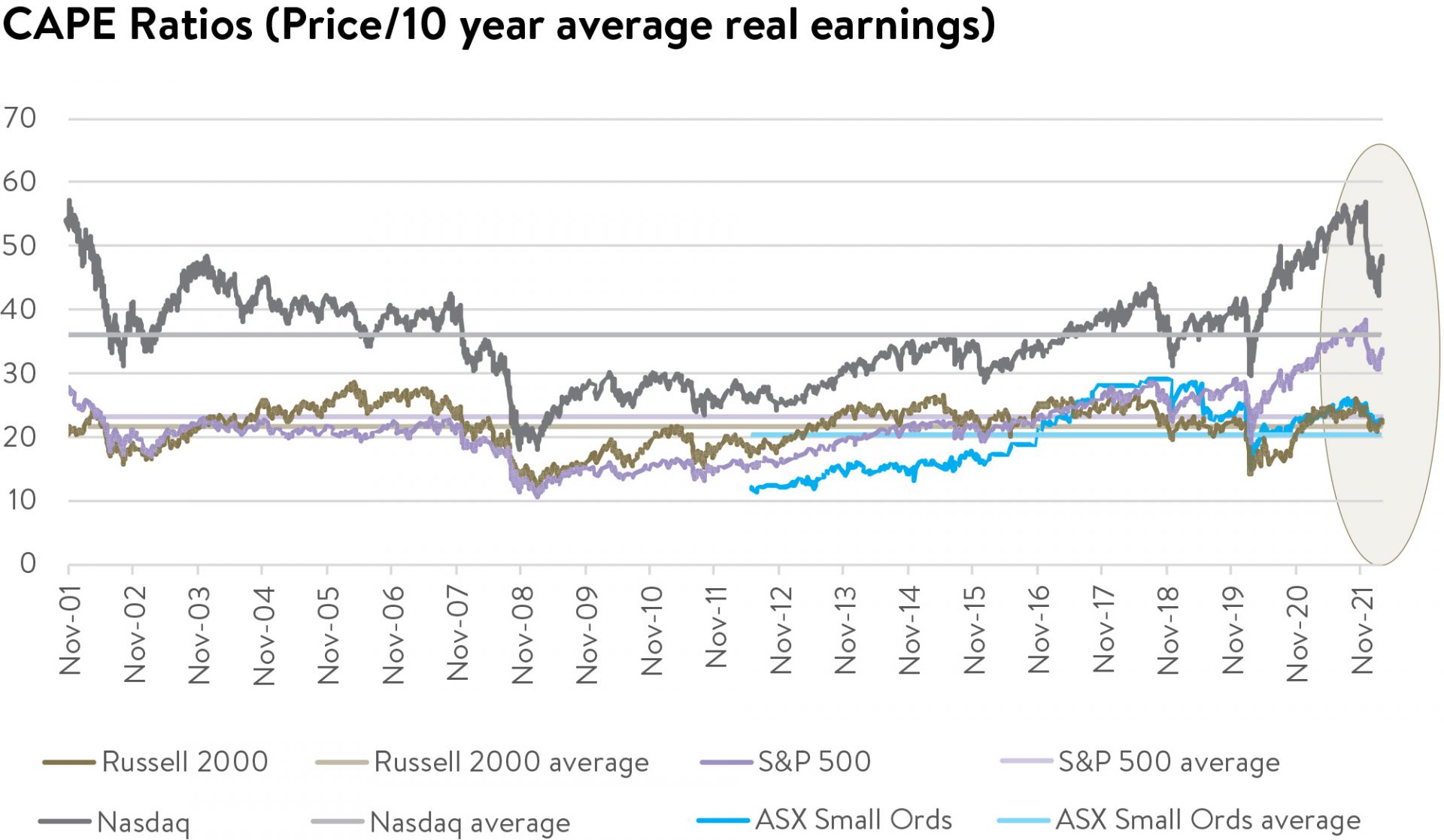

Below we show the valuations for US large caps (S&P500), US tech (Nasdaq), US small caps (Russell 2000) and Australian small caps (ASX Small Ords) using a cyclically-adjusted price-to-earnings ratio (also called the CAPE ratio). This metric has a very good relationship with subsequent returns over the medium to long term (next 5+ years).

What we can see is that US and Australian small cap valuations are now back to around their long term average levels after recent falls, suggesting 8-10%+ longer term market returns in these segments have a high probability. We of course hope to do considerably better than this through stock picking.

What is also clear from this chart is that small cap valuations are currently very attractive compared to US large caps and large cap tech companies. These parts of the market have much higher CAPE ratios.

Cheaper valuations in the small cap part of the market we fish in don’t guarantee better returns ahead, but they certainly give you a big head start.

Small cap valuations are currently attractive versus large cap

Source: FactSet to 5 April 2022. CAPE ratio in the cyclically-adjusted price-to-earnings ratio.

Earnings will win the day

The stock pickers have had to sit to one side of late as macro events are determining whether share prices go up or down. We are stock pickers at the end of the day and that is where our edge is.

We have been telling our investment team that we need to be travelling more than we ever have before. There are going to be stocks out there that have been sold off substantially more than the companies in our portfolios. We’ve got a huge universe of companies to analyse, and we need to sift through them because if we can find those that have been really harshly and unfairly dealt with, they will set us up for the next leg of growth in the Ophir funds.

Importantly, we’re picking the earnings upgrades of companies, as well as we ever have before. At the end of the day, our stock picking abilities have not changed at all. So, when this market turns to a stock picker’s market again, we will be rewarded. Now, we don’t know if it’s this month, next month or in three, four, five, six months’ time, but it will turn to being all about earnings again as it always has. We will be rewarded as long as we are patient.

As Buffett puts it “the stock market is a device from transferring money from the impatient to the patient”.

As always, thank you for entrusting your capital with us.

Kindest regards,

Andrew Mitchell & Steven Ng

Co-Founders & Senior Portfolio Managers

Ophir Asset Management

This document is issued by Ophir Asset Management Pty Ltd (ABN 88 156 146 717, AFSL 420 082) (Ophir) in relation to the Ophir Opportunities Fund, the Ophir High Conviction Fund and the Ophir Global Opportunities Fund (the Funds). Ophir is the trustee and investment manager for the Ophir Opportunities Fund. The Trust Company (RE Services) Limited ABN 45 003 278 831 AFSL 235150 (Perpetual) is the responsible entity of, and Ophir is the investment manager for, the Ophir Global Opportunities Fund and the Ophir High Conviction Fund. Ophir is authorised to provide financial services to wholesale clients only (as defined under s761G or s761GA of the Corporations Act 2001 (Cth)). This information is intended only for wholesale clients and must not be forwarded or otherwise made available to anyone who is not a wholesale client. Only investors who are wholesale clients may invest in the Ophir Opportunities Fund. The information provided in this document is general information only and does not constitute investment or other advice. The information is not intended to provide financial product advice to any person. No aspect of this information takes into account the objectives, financial situation or needs of any person. Before making an investment decision, you should read the offer document and (if appropriate) seek professional advice to determine whether the investment is suitable for you. The content of this document does not constitute an offer or solicitation to subscribe for units in the Funds. Ophir makes no representations or warranties, express or implied, as to the accuracy or completeness of the information it provides, or that it should be relied upon and to the maximum extent permitted by law, neither Ophir nor its directors, employees or agents accept any liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. This information is current as at the date specified and is subject to change. An investment may achieve a lower than expected return and investors risk losing some or all of their principal investment. Ophir does not guarantee repayment of capital or any particular rate of return from the Funds. Past performance is no indication of future performance. Any investment decision in connection with the Funds should only be made based on the information contained in the relevant Information Memorandum or Product Disclosure Statement.