By Andrew Mitchell & Steven Ng

Co-founders and Senior Portfolio Managers

In our June Letter to Investors we explore some key issues — including the delta Covid-19 variant, the outlook for rate rises, and the commodities cycle — that will help determine if the new financial year will be just as strong for markets as FY21.

Dear Fellow Investors,

Welcome to the June Ophir Letter to Investors – thank you for investing alongside us for the long term.

When Doves Cry

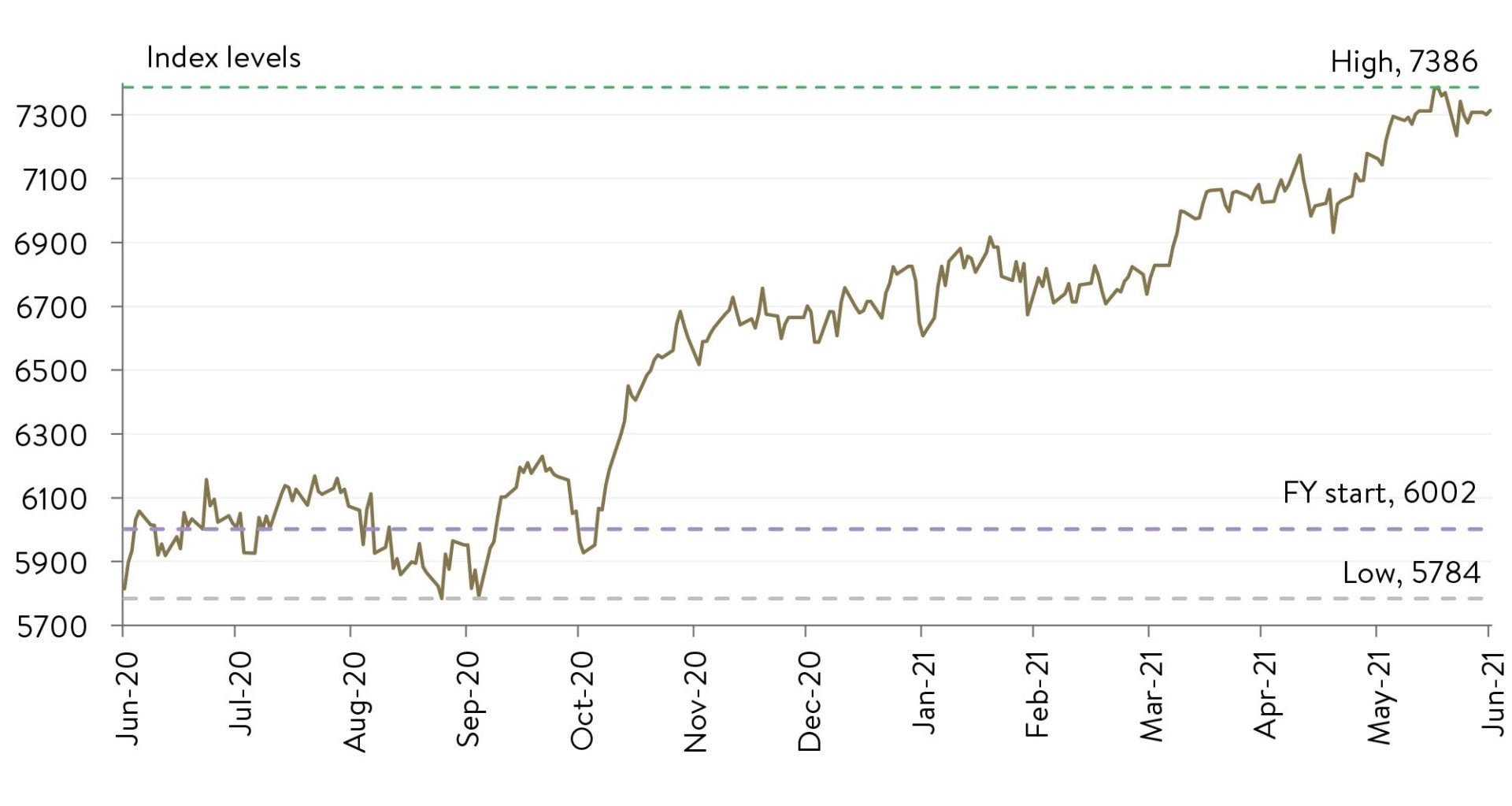

The 2021 financial year, which recently ended, was certainly one to remember with most major markets up an ultra-bullish 20%+ in the year to 30 June. That’s well above their long-term average of circa 10%.

US equities gained +42.5%, Europe +27.3%, and Japan +28.9%. The domestic market was a relative laggard in FY21, with the ASX200 rising +27.8%. But that was still its 11th highest financial year gain since 1903.

After a slow start to the FY, the ASX200 was stronger from November, finishing close to its all time high of 7386

Source: RIMES, Morgan Stanley Research

As you can see in the chart above, most of the gains came after November 2020 when positive vaccines news and a reflationary Biden government agenda in the US saw markets take off.

Income returns during last financial year, though, only made up a sliver of returns because dividends were cut due to COVID-19 induced uncertainty, providing the lowest level of income returns since 1987 for Australian shares.

So what will the new financial year hold for investors?

In this letter, we explore some key issues — including the delta Covid-19 variant, the outlook for rate rises, and the commodities cycle — that will help determine if the new financial year will be just as strong for markets. We also discuss that for investors seeking long-term wealth creation, equities will still be the place to invest, with small and mid-cap Australian and global equities markets providing a particularly sweet spot with an abundant supply of opportunities and ideas.

And, finally, we reveal an interesting lesson from soccer goalies that — as with investing — it is not always best to take action.

June 2021 Ophir Fund Performance

Before we jump into the letter, we have included below a summary of the performance of the Ophir Funds during June. Please click on the factsheets if you would like a more detailed summary of the performance of the relevant fund.

The Ophir Opportunities Fund returned +5.1% net of fees in June outperforming its benchmark which returned +3.1% and has delivered investors +25.6% p.a. post fees since inception (August 2012).

Download Ophir Opportunities Fund Factsheet

The Ophir High Conviction Fund investment portfolio returned +6.3% net of fees in June, outperforming its benchmark which returned +3.4% and has delivered investors +20.2% p.a. post fees since inception (August 2015). ASX:OPH provided a total return of +5.0% for the month.

Download Ophir High Conviction Fund Factsheet

The Ophir Global Opportunities Fund returned +5.6% net of fees in June, outperforming its benchmark which returned +3.4% and has delivered investors +45.1% p.a. post fees since inception (October 2018).

Download Ophir Global Opportunities Fund Factsheet

Doves cry in June

We may never know the underlying meaning of what Prince’s 1984 smash hit ‘When Doves Cry’ meant. Some say it symbolised when two people disagree. (At the time many may have disagreed with it knocking Bruce Springsteen’s ‘Dancing in the Dark’ to no.2 in the charts – including one of your authors!)

In markets, June was all about a disagreement between hawks and doves.

The main news was the US Federal Reserve’s ‘hawkish’ stance in its interest rate outlook. This put the noses out of joint for monetary policy ‘doves’ – those crying out for lower-for-longer interest rates. The Fed brought forward their expected interest rate ‘lift-off’ from 2024 to 2023 because of better-than-expected growth and employment outcomes. In response, the US yield curve ‘flattened’, with 2-year interest rates rising and 10-year yields declining, which reflects investors now expecting lower long-term inflation.

Still, equity markets generally took this in their stride to help produce a strong finish to the year. The Nasdaq (+5.6%), ASX Small Ords (+3.1%), ASX200 (+2.3%), S&P 500 (+2.3%), Russell 2000 (+1.9%) and MSCI Europe (+1.7%) all generated above-average results for June.

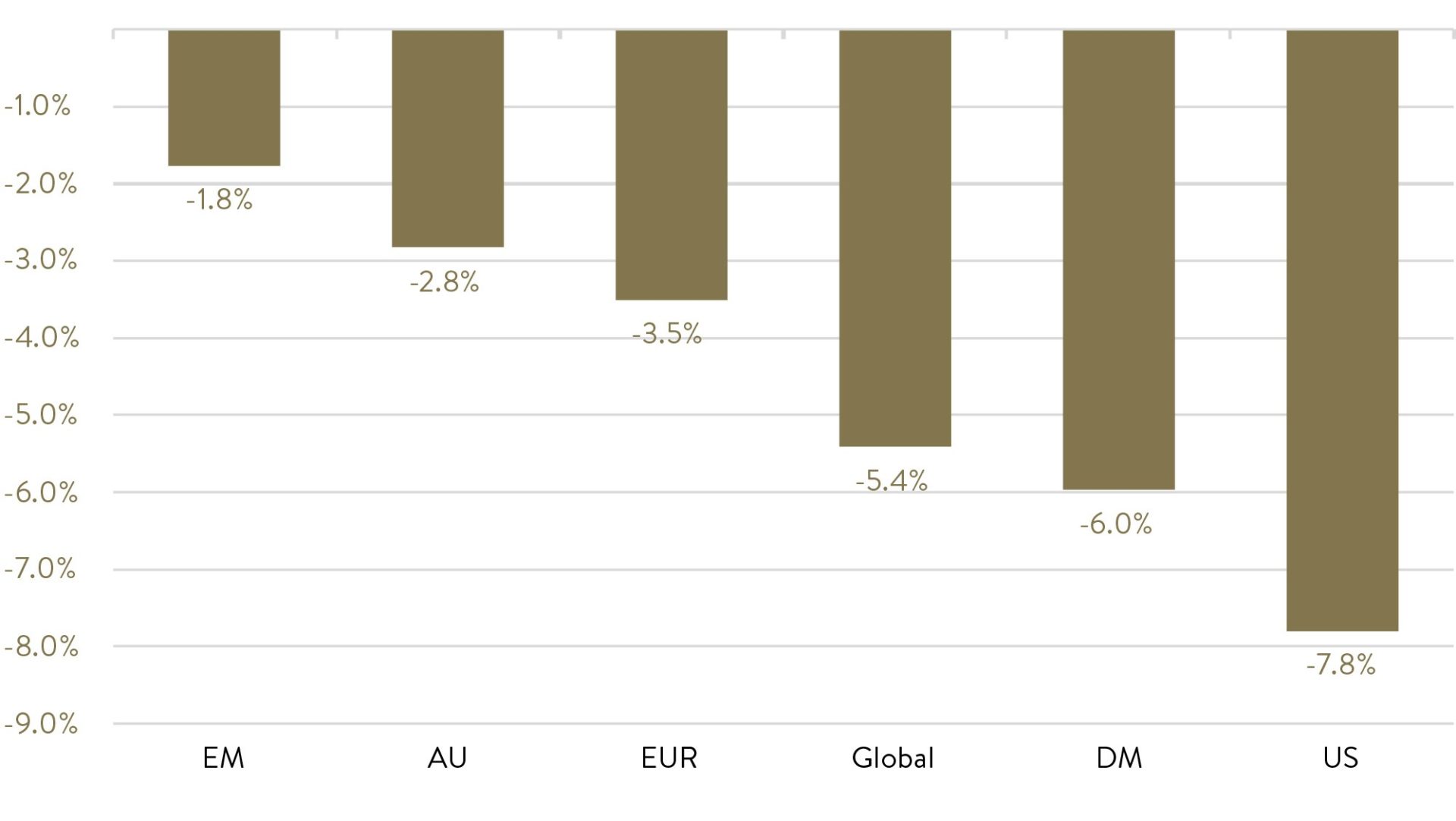

As expected, the US dollar rose because investors bought the currency to take advantage of the higher short-term interest rates on offer. The USD rose +3.0% against the Australian dollar and +2.9% (DXY) against a basket of major currencies. The commodity with the largest sensitivity to the USD – gold – was hit the hardest, falling -7.8% on the month.

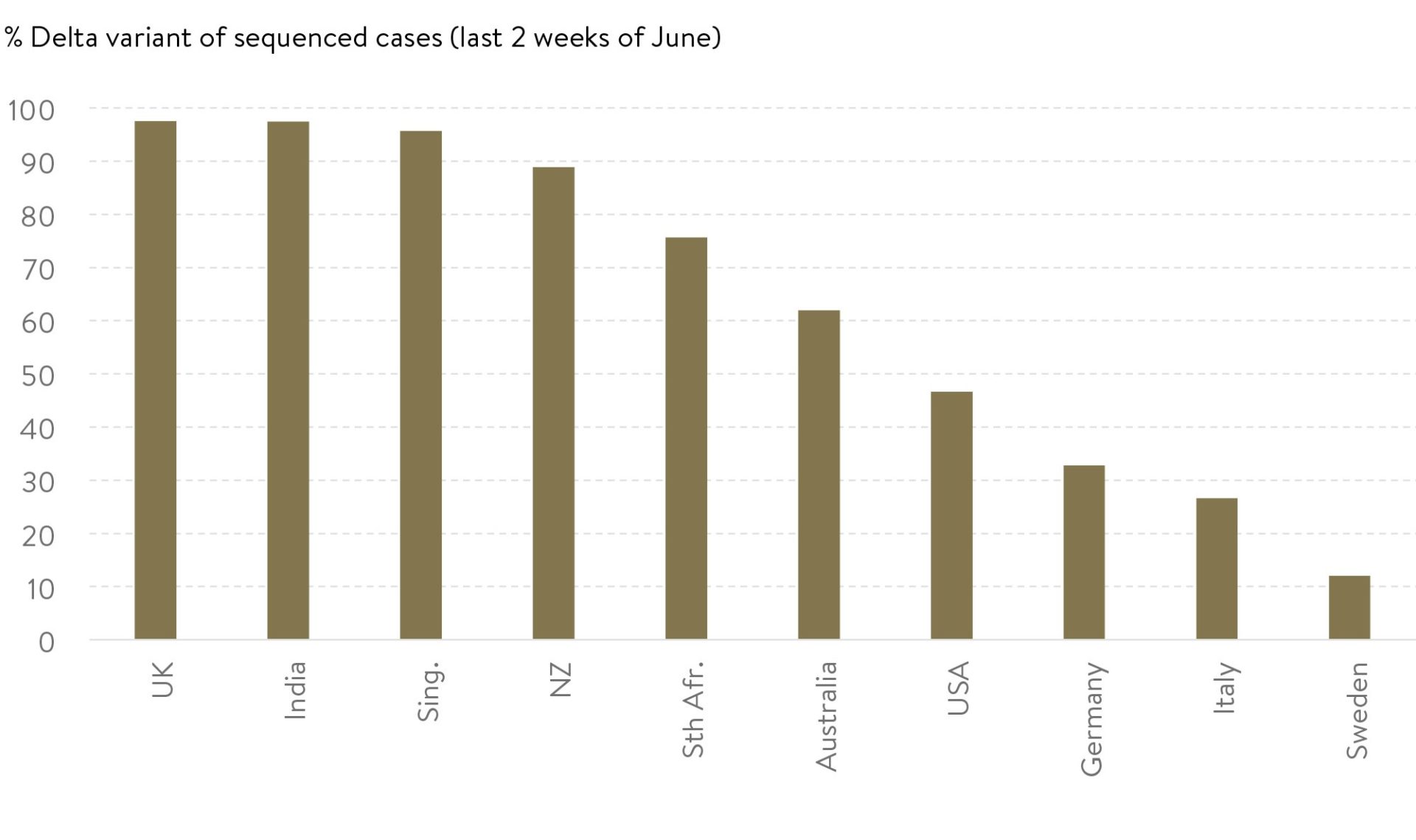

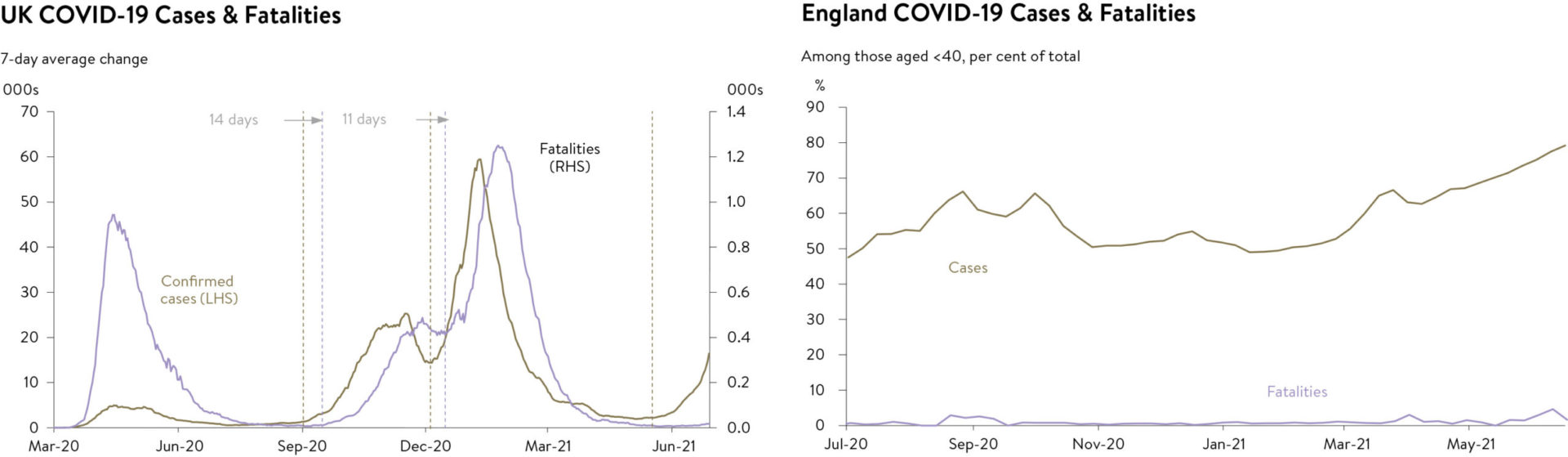

The delta strain races vaccines

If you didn’t know what the ‘delta’ strain of the new coronavirus was before June, you almost certainly do now. The more transmissible variant has quickly become, or will likely soon become, the dominant strain of the virus in many parts of the world (see chart).

Delta variant taking over

Source: MST Marquee

The delta variant creates two risks for share markets. The first is whether it would spread before countries could inoculate their populations, forcing Governments to extend or plunge their nations back into mobility restrictions and once again cripple economic activity. The second risk is whether the current vaccines are effective against this new variant.

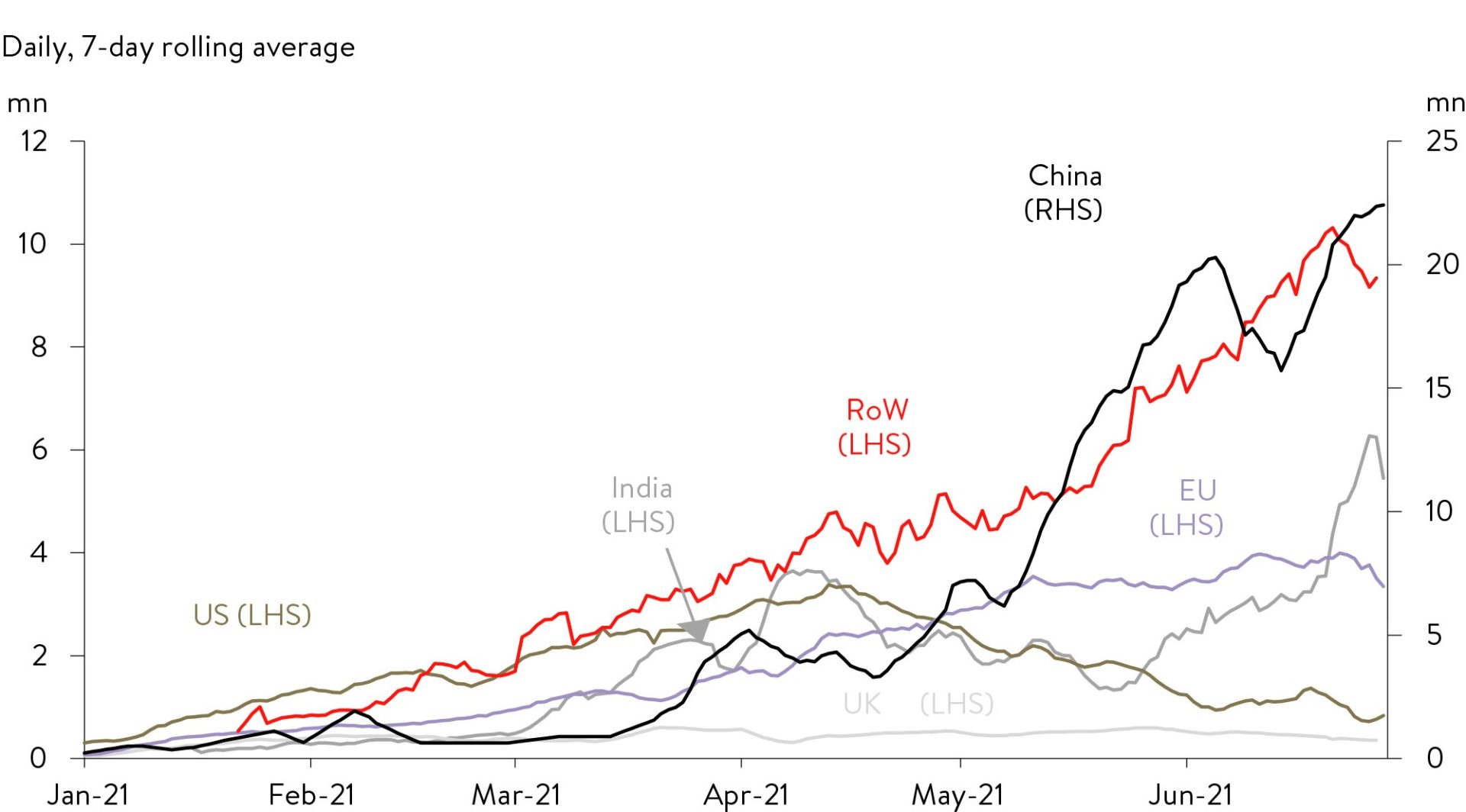

COVID-19 Vaccination Doses Administered

Source: Macquarie

On the first risk, the rollout continues to ramp up with around 40 million doses per day being dolled out at present. Incredibly, at around 23 million a day, China is doling out more than half of these doses. That’s almost the equivalent of Australia’s population in a 24-hour period! (chart above).

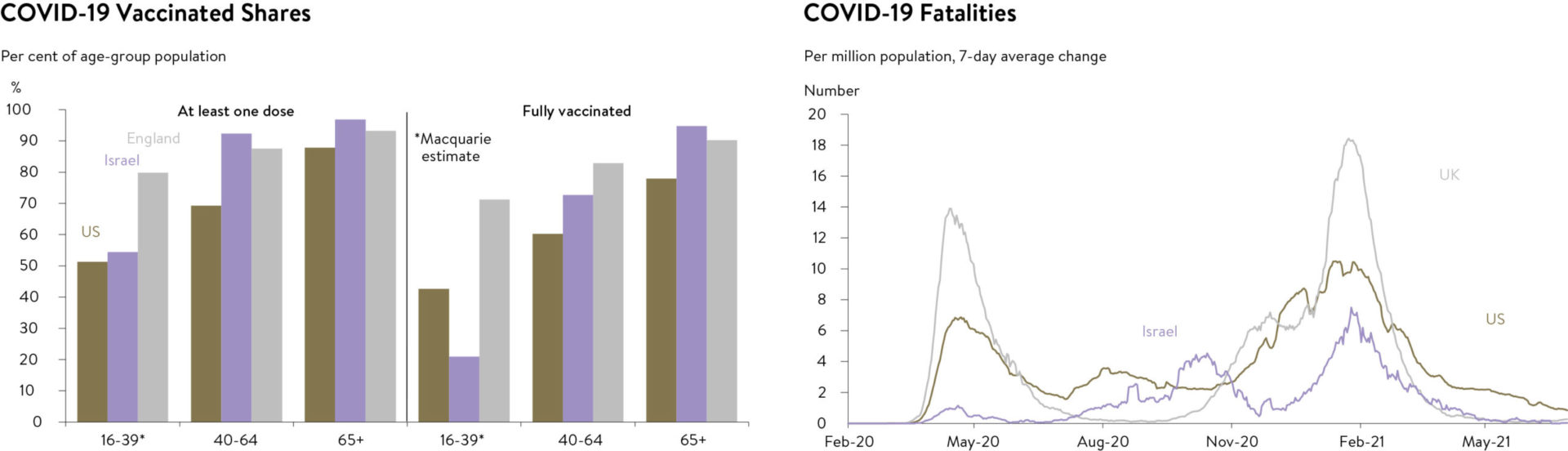

A few countries are also winning the race with a high percentage (50%+) of their adult population vaccinated (such as Canada, Israel, UK, US, Italy and Germany). Many, though, are languishing, including most emerging economies (e.g. India and Brazil), but also South Africa, New Zealand and Australia.

Source: Macquarie

Very encouragingly, as you can see in the chart above, countries that are nearing maturity of vaccine rollouts, such as the US, UK and Israel, have blunted fatalities at a stunning rate.

On the second risk, pleasingly, the main vaccines (including Pfizer, Moderna, J&J and Astrazeneca) appear quite effective against the delta strain based on early data. In highly vaccinated countries like the UK, where cases have started to spike again recently due to the delta strain, hospitalisations and fatalities haven’t surged because the cases have been concentrated in unvaccinated young people who are less likely to suffer serious illness (see chart below).

Source: Macquarie

This all bodes well for the continued re-opening of economies as vaccine rollout continues throughout this year.

Hawkish Fed sees rotation rotate

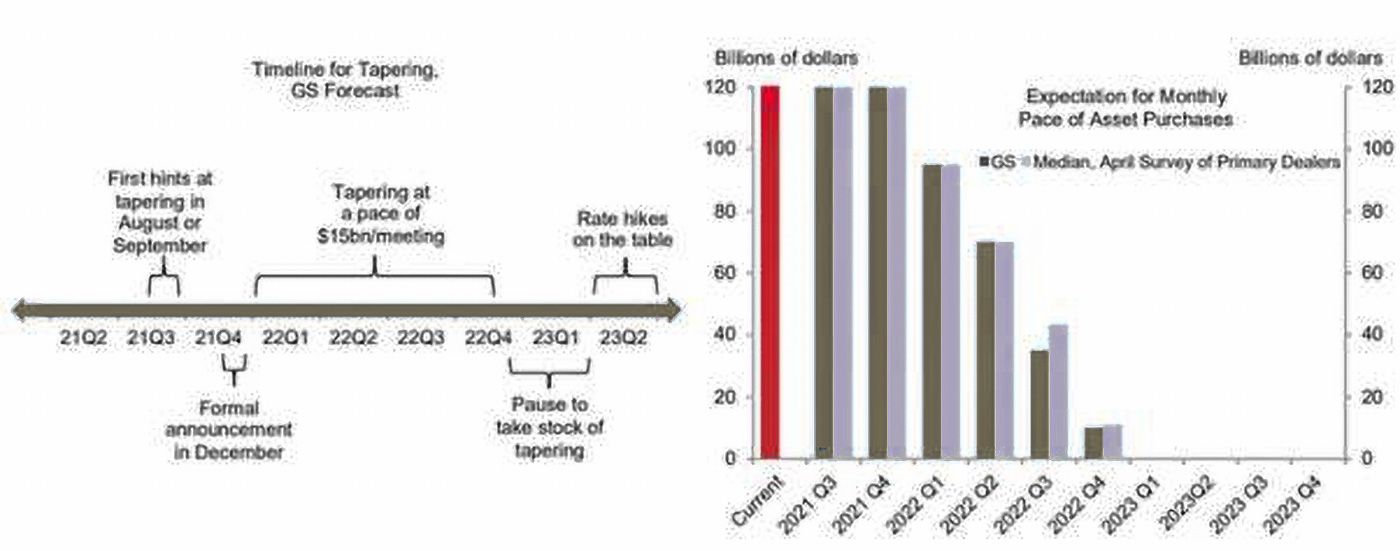

As noted above, if markets weren’t talking about the delta strain in June, they were talking about the more hawkish stance the Fed took post their June meeting. The Fed expects to raise rates sooner than it expected because the economic recovery is beating expectations. But before that occurs, they must begin reducing (or tapering in ‘Fed speak’) their bond buying/quantitative easing (QE) program.

Source: Goldman Sachs

As you can see in the chart above, Goldman Sachs and market surveys see 2022 as being ‘The Year of QE Tapering’ with rate hikes beginning in mid-2023.

The Fed will have not forgotten the so-called ‘taper tantrum’ of markets in 2013 when the central banks wound down their GFC bond-buying program. So investors can expect the Fed to provide clear guidance this year on how they taper QE. If the past is a prologue, any share market weakness around the signalling of tapering may be a buying opportunity for investors.

As we’ve discussed in previous letters improving economic growth and higher expected inflation have generally seen ‘value’ styles of investing outperform ‘growth’ over the last 6-9 months.

In June, however, that rotation to value stopped. As inflation expectations eased, and long-term interest rates fell in the US (and Australia), markets rotated back to growth.

The US had the most pronounced underperformance of value during the month, but it was across the board, including domestically where recent value outperformance has been greater relative to other markets because of Australia’s large weighting to the value-centric financials/banks sectors.

Value vs. Growth (Jun-21)

Source: JP Morgan, Bloomberg Finance L.P.

Still, we still think this is likely just a pitstop, with high interest rates from the Fed likely to drive real interest rates higher and continue further outperformance of Value orientated sectors and companies.

We won’t time the commodities cycle

One headwind that our Australian equity strategies have faced into over the last year is the outperformance of the Materials sector – a sector that we typically don’t have an overweight position in because they have highly cyclical earnings which fluctuates with commodity prices, they have virtually no pricing power and are generally very capital intensive businesses. Materials have outperformed in Australia over the last financial year as commodity prices, like iron ore, coal, oil and lithium rose on the back of a recovering global economy and supply issues.

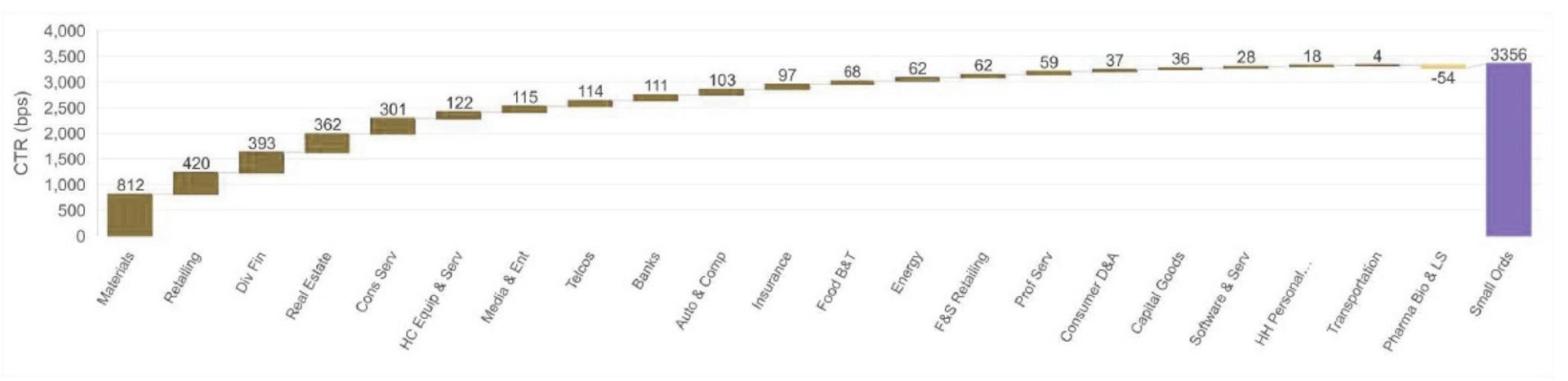

Industry Group Contribution to Performance (TR) – FYTD

Source: Bloomberg, Morgan Stanley Research. Performance as at 30 June 2021.

As seen above, the Materials group contributed twice as much to the Small Ords index return in Australia over the last year than any other industry group. This was driven by a large sector weighting and standouts such as Pilbara Minerals (+523%), Galaxy Resources (+378%) & Lynas Rare Earth (+190%).

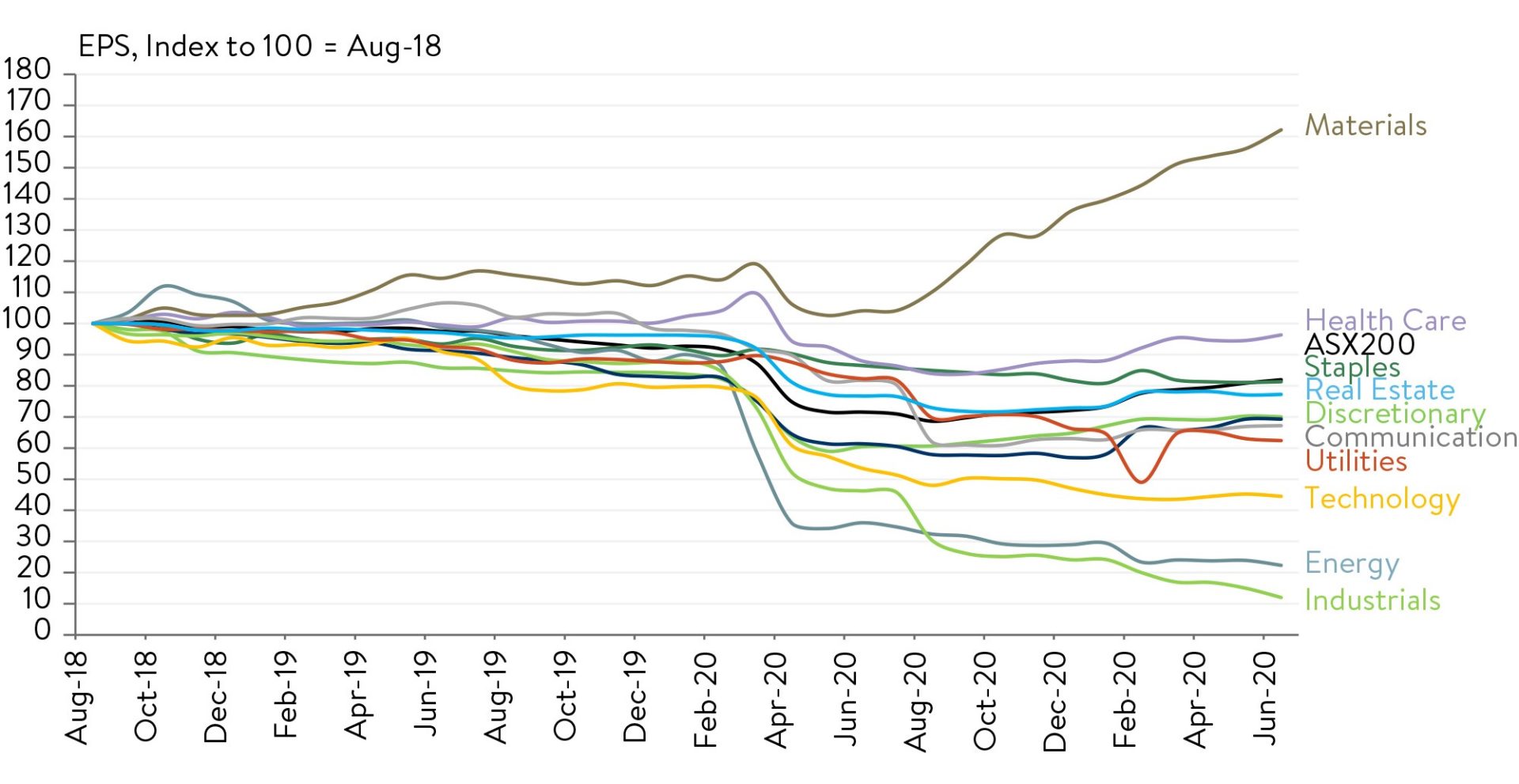

Price rises in the sector has been driven off a fundamental base, with earnings estimates rising on the back of the commodity price windfall (see chart below).

What might this mean?

FY21 Annual consensus EPS revision trends by sector

Source: RIMES, IBES, Morgan Stanley Research

Through harsh experience we have learned not to try and time the commodity price cycle – it is not our forte – but we are not sure it is many other investors’ either! When we do invest in the sector we would prefer to partner, by buying into their stocks, with the best operators in the sector who can manage these risks better than we can and have a track record of superior operational management to extract value through the cycle.

The high price of action

Like many things in investing, just because you CAN attempt to time the commodity cycle, or market tops and bottoms for that matter, doesn’t mean you SHOULD.

That reminds us of a study of professional soccer goalies conducted a few years ago. When facing penalty kicks, the goalie jumped left or right about 94% of the time and stayed in the middle only 6%. The penalty taker, however, went down the middle about 30% of the time.

Source: Ben Carlson, “Action bias among elite soccer goalkeepers” (Bar-Eli et al).

The researchers found the ‘save percentage’ would double if they just stayed in the middle a third of the time. The problem is you look silly as a goalie if you just stand in the middle and an opponent slots it past you to the left or right. The lesson is that humans prefer action because it makes us feel more in control. But many times, we are not!

Action has many costs in investing such as timing risks, brokerage and market movement costs. Sometimes the hardest thing is to just stay put, stick to your process, and only invest in areas where you believe you have an edge over competitors and the market. We continue to focus on conducting our very detailed bottom-up due diligence on companies.

At the present, at the margin, we prefer companies exposed to reopening economies where the company has a structural-growth tailwind, that can sustain them as growth normalises.

We have also continued to be even more mindful of not overpaying for growth because we believe long-term interest rates are more likely to head higher than lower over the next year or two in the major economies, creating headwinds for returns from sky-high ‘revenue multiple’ businesses. Our hurdle remains elevated for including high growth/high valuation businesses and we must be highly confident of material earnings ‘beats’.

An exciting surfeit of new ideas

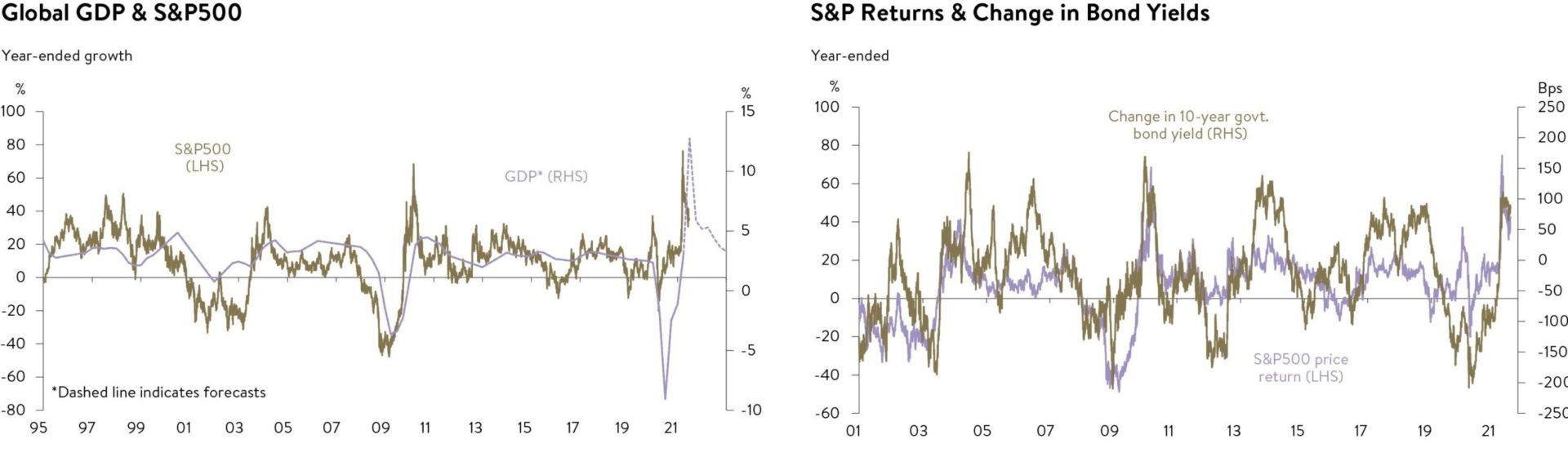

Overall, we remain somewhat sanguine about the outlook for markets. While peak growth may have just passed in the U.S. recently, solid economic growth and higher long-term bond yields (particularly in the normalisation stage) suggest reasonable equity returns are still ahead (see chart below).

Source: Macquarie

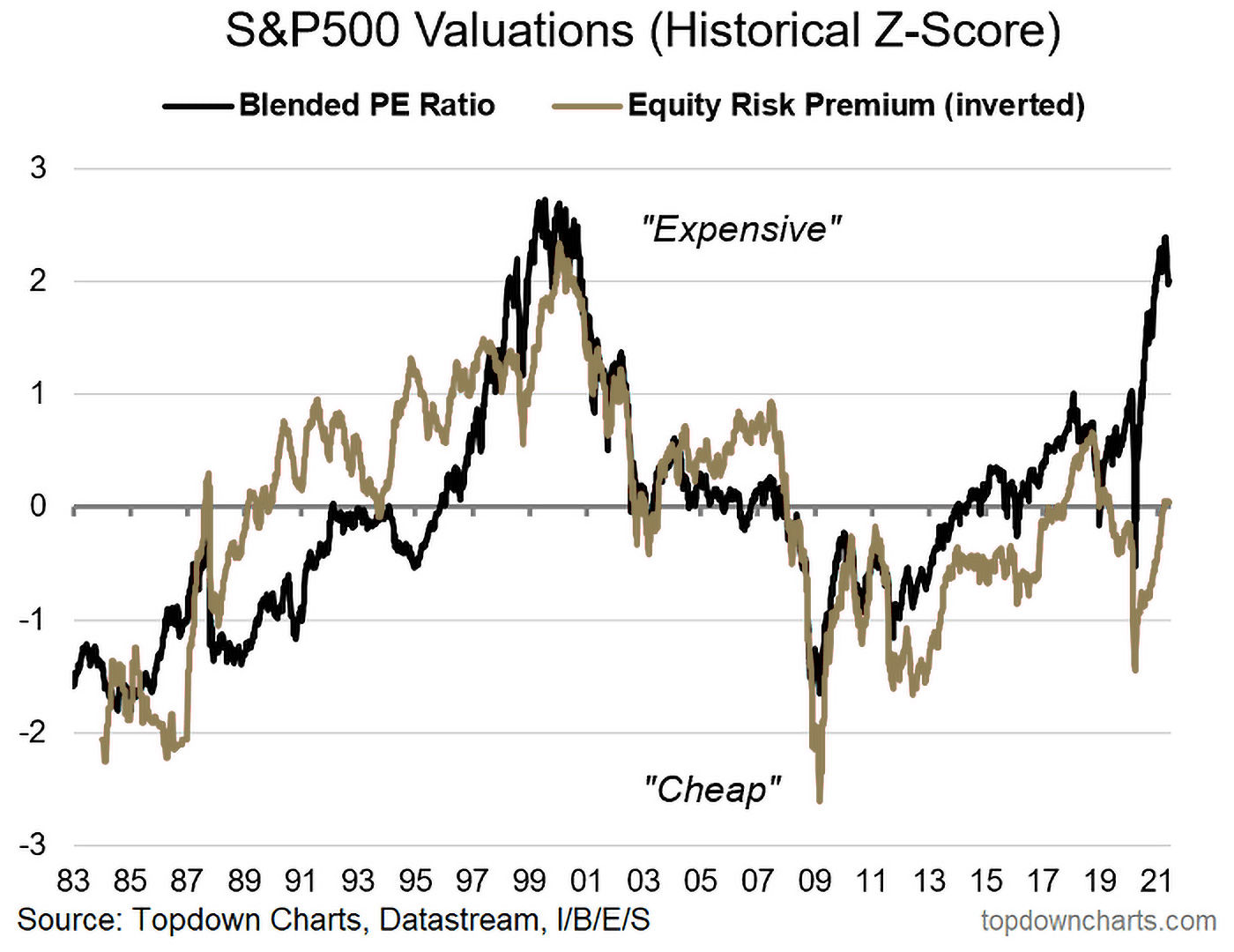

S&P500 Valuations (Historical Z-Score)

Many investors continue to complain about high valuations for share markets and in many cases that remains true in an absolute sense, particularly for US large caps (S&P 500 – black line below).

Source: Topdown Charts, Datastream, I/B/E/S

But bonds have been even more expensive. So, when we look at the ‘equity risk premium’ – a fancy term for how cheap or expensive shares are compared to bonds – the story is much less worrying (see gold line). In fact, it is downright boring. US large caps, the most expensive ‘big’ share market in the world, look about fair value versus bonds.

This is different to past episodes when absolute valuations (black line) used to send the same signal as relative valuations versus bonds (gold line) – but not so the last few years. So yes, expected returns might be lower due to the higher starting valuations for US large caps and bonds, but do you go to cash to avoid a bubble in share market valuations? We are not so sure.

Fortunately, the small and mid-cap Australian and global markets we invest in are currently more attractively valued relative to US large caps based on the key measures we follow.

The biggest test for us, though, comes from gauging the level of competition for new ideas to make it into our portfolios. Pleasingly, we have no shortage of ideas right now. Indeed, there are so many ideas our investment team is struggling to keep the position numbers in our funds low so they remain high conviction. That’s a good problem to have as we head into a new financial year.

As always, thank you for entrusting your capital with us.

Kindest regards,

Andrew Mitchell & Steven Ng

Co-Founders & Senior Portfolio Managers

Ophir Asset Management

This document is issued by Ophir Asset Management Pty Ltd (ABN 88 156 146 717, AFSL 420 082) (Ophir) in relation to the Ophir Opportunities Fund, the Ophir High Conviction Fund and the Ophir Global Opportunities Fund (the Funds). Ophir is the trustee and investment manager for the Ophir Opportunities Fund. The Trust Company (RE Services) Limited ABN 45 003 278 831 AFSL 235150 (Perpetual) is the responsible entity of, and Ophir is the investment manager for, the Ophir Global Opportunities Fund and the Ophir High Conviction Fund. Ophir is authorised to provide financial services to wholesale clients only (as defined under s761G or s761GA of the Corporations Act 2001 (Cth)). This information is intended only for wholesale clients and must not be forwarded or otherwise made available to anyone who is not a wholesale client. Only investors who are wholesale clients may invest in the Ophir Opportunities Fund. The information provided in this document is general information only and does not constitute investment or other advice. The information is not intended to provide financial product advice to any person. No aspect of this information takes into account the objectives, financial situation or needs of any person. Before making an investment decision, you should read the offer document and (if appropriate) seek professional advice to determine whether the investment is suitable for you. The content of this document does not constitute an offer or solicitation to subscribe for units in the Funds. Ophir makes no representations or warranties, express or implied, as to the accuracy or completeness of the information it provides, or that it should be relied upon and to the maximum extent permitted by law, neither Ophir nor its directors, employees or agents accept any liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. This information is current as at the date specified and is subject to change. An investment may achieve a lower than expected return and investors risk losing some or all of their principal investment. Ophir does not guarantee repayment of capital or any particular rate of return from the Funds. Past performance is no indication of future performance. Any investment decision in connection with the Funds should only be made based on the information contained in the relevant Information Memorandum or Product Disclosure Statement.