SaaS versus Semis

For this month’s Stock in Focus, we’re doing something a little different.

Rather than spotlighting a single company (though we will highlight one), we’re zooming out to explore a significant rotation: The growing dispersion between software and semiconductors, particularly within the broader AI thematic.

Both groups sit under the ‘tech’ umbrella, but their near-term investor narratives couldn’t be more different.

Put simply:

- The application layer (SaaS) is being severely punished for uncertainty around the durability of its business models in an AI world.

- The picks and shovels (semis, AI Infrastructure) are being rewarded for their growth potential and the earnings certainty that AI investment is creating for them.

This dispersion is throwing up big opportunities for Ophir in both application companies and semis, but we are mindful of managing downside risks as debates about the impact of AI continue to play out.

Source: Ophir. Bloomberg.

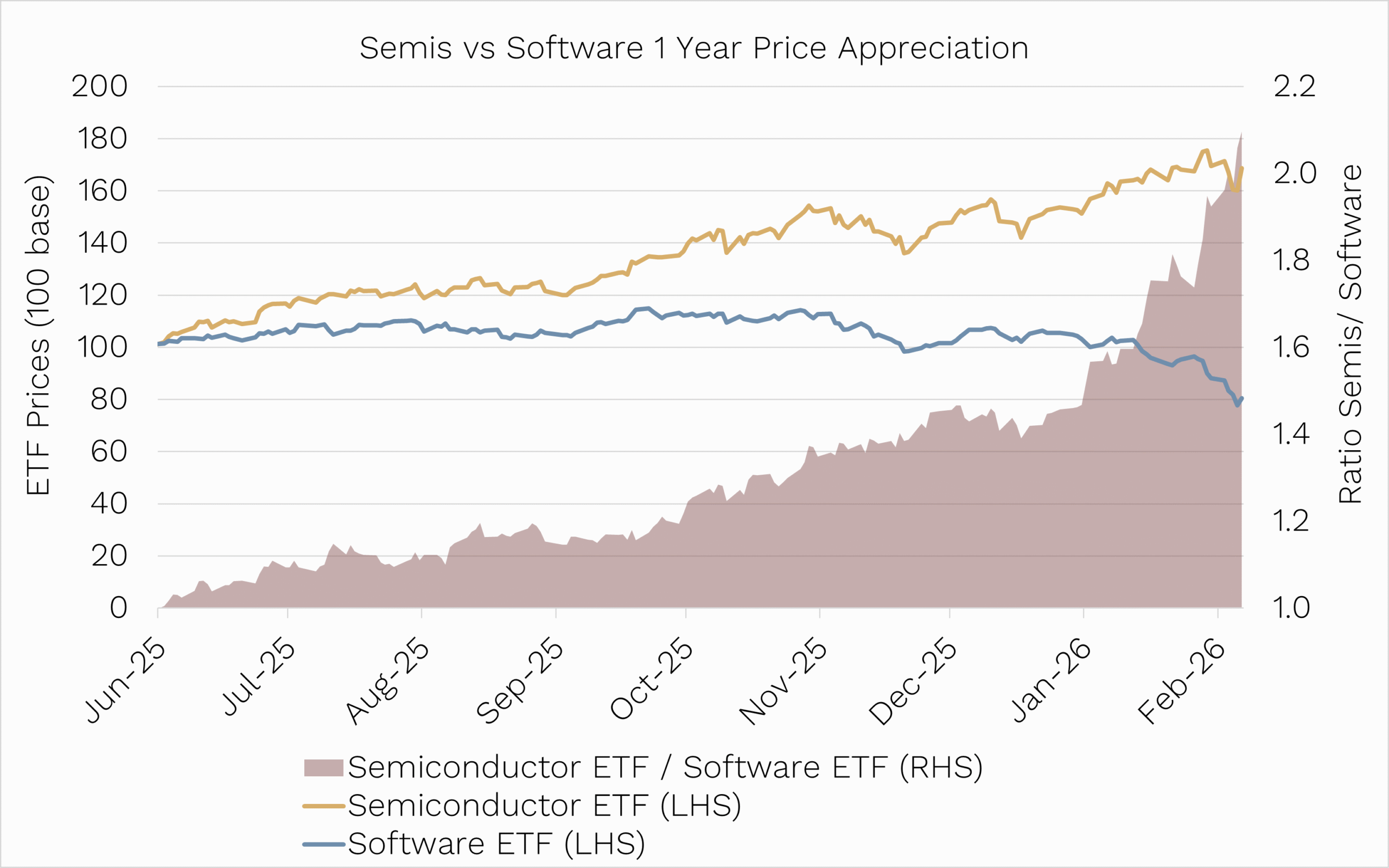

The Software Shakeout: Zero-Seat Threat

The woes of the software sector started as a slow bleed in the second half of 2025 when it became clear AI investment would skew heavily toward infrastructure, rather than application-layer enhancements. Investors began recalibrating growth expectations for software businesses.

But then the software sector was rocked on January 12 when Anthropic released its Claude Cowork preview. It showcased autonomous agents that could perform complex workflows with minimal human input.

This wasn’t just another chatbot. It highlighted that entire seat-based workflows (licensing models based on the number of users) could be replaced.

For the past decade, enterprise SaaS companies have grown alongside corporate headcount. Products were priced ‘per seat’, and forward multiples assumed that more humans meant more licences.

But if AI agents can perform a week’s worth of work in a day, the unit of value in software – the human seat – comes under serious structural pressure.

This is the Zero-Seat Threat.

While big-cap incumbents like Salesforce (CRM) and Adobe (ADBE) have launched AI initiatives (Agentforce, Firefly) to defend their moats, these have yet to translate into a tangible revenue uplift, and investors fear that incumbents are simply running to stand still.

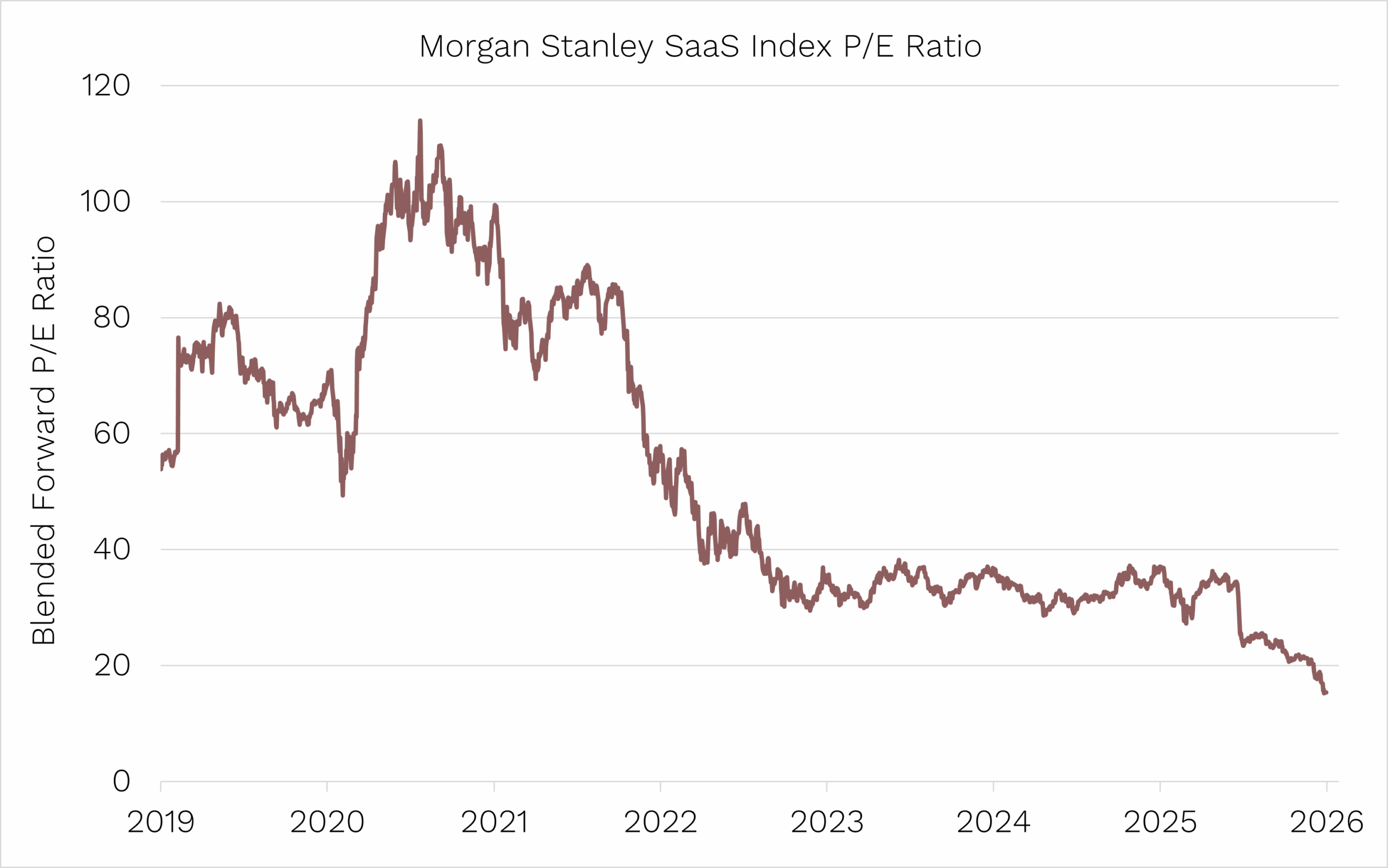

When long-duration stocks lose revenue predictability, multiples compress quickly. Morgan Stanley’s SaaS index forward earnings expectations are now trading on ~15x, compared to a 30-40x range since mid-2022.

Source: Ophir. Bloomberg.

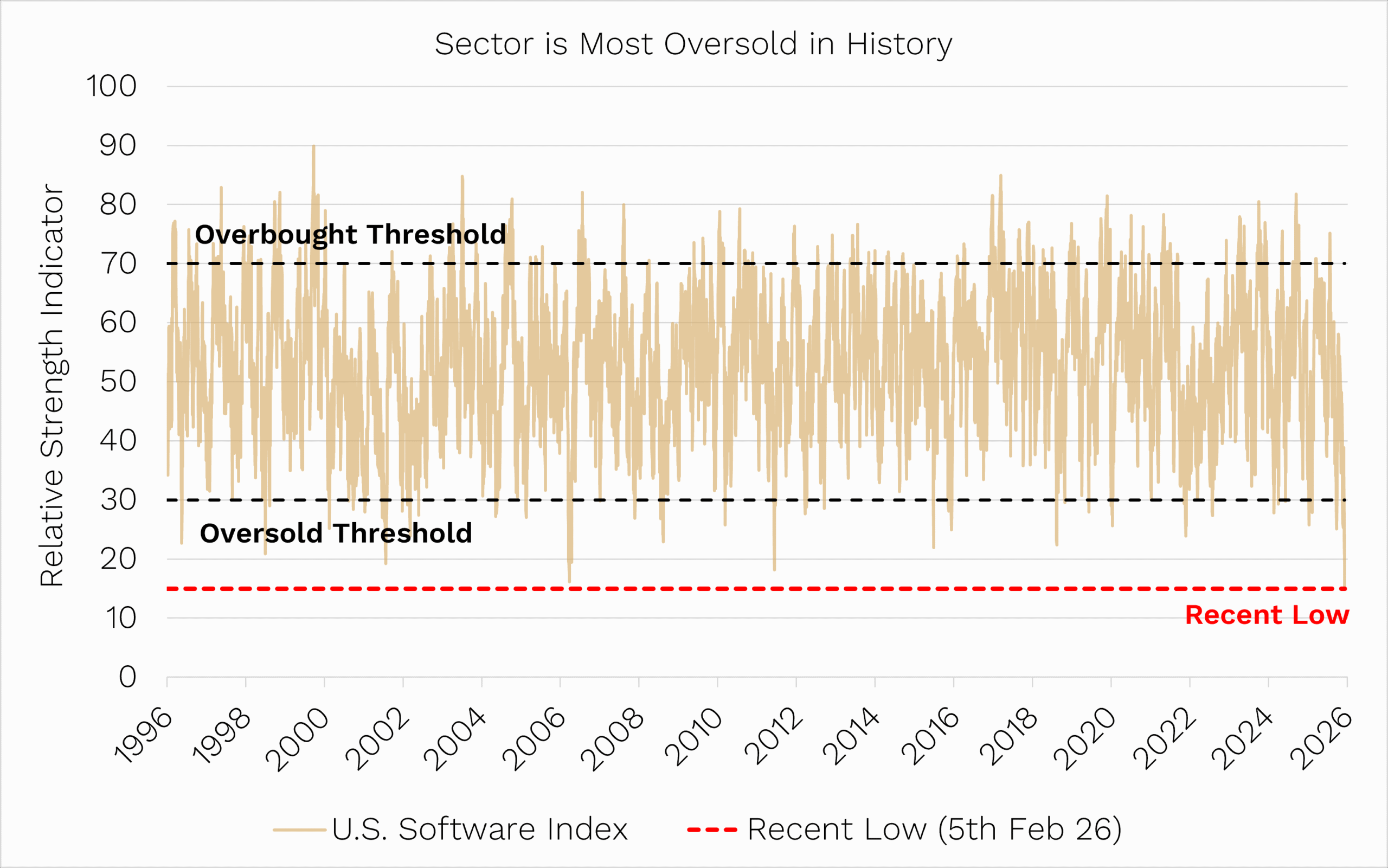

The software sector is now showing its weakest technical breadth since 2018. The S&P North American Software Index recently hit it’s most oversold level ever based on its 14-day RSI (relative strength index) – even more than in the tech wreck of 2001!

Source: Ophir. Bloomberg. U.S. Software Index refers to S&P North American Technology Software Index (SPGSTISO).

Given the quantum and indiscriminate nature of the price moves in the sector, we expect there to be opportunities to invest in companies that have been oversold.

However, we are mindful that as uncertainty persists and the debate around future earnings continues, it will be difficult for many software names to see their multiples re-rate.

Meanwhile in Semis: Earnings Visibility is the New Growth

While software stumbles, semiconductors are going from strength to strength.

Semis are benefiting from both a cyclical rebound and structural AI demand.

It began, of course, with Nvidia, the poster child of the AI build-out, but it’s now expanded into the broader infrastructure stack.

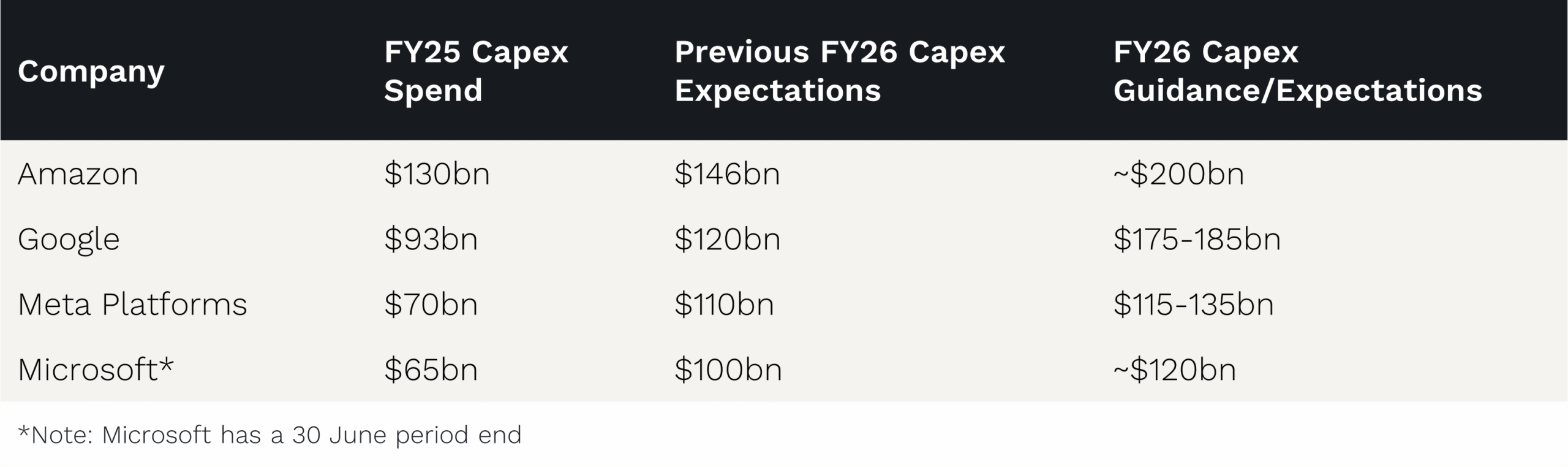

The major driver is huge AI capex.

Microsoft, Amazon, Alphabet, and Meta have all locked into multi-year AI capex plans, committing hundreds of billions each toward training clusters (specialised supercomputers to build large language models) and inference capacity (infrastructure to run AI for users).

In their recent results, all of these companies provided capex guidance for 2026 that was well above market expectations.

This obviously creates surging demand for chips and chip-making infrastructure.

Source: Ophir & Company Reports. Figures in $USD.

Semis have typically been more cyclical, but massive AI capex has given them what investors love – earnings visibility.

With AI being funded in real time, order books are now full, supply is constrained, and lead times are stretched.

This has shifted the entire sector’s narrative from ‘cyclical’ to ‘critical infrastructure’.

At the same time, semis are benefiting from a broader macro recovery in PCs and smartphones.

And in January there were several key events that added more fuel to the fire:

- At CES (Consumer Electronics Show), Nvidia CEO Jensen Huang called out memory and storage as the next AI frontier.

- Samsung and Micron said the price of memory was increasing 40-50%.

- TSMC came out with really strong capex guidance of ~US$52-56 billion, which was well above market expectations.

As a result, memory and storage names have continued to surge, including (approximate 1-year returns) SanDisk (+1,520%), Seagate (+335%) and Western Digital (+450%).

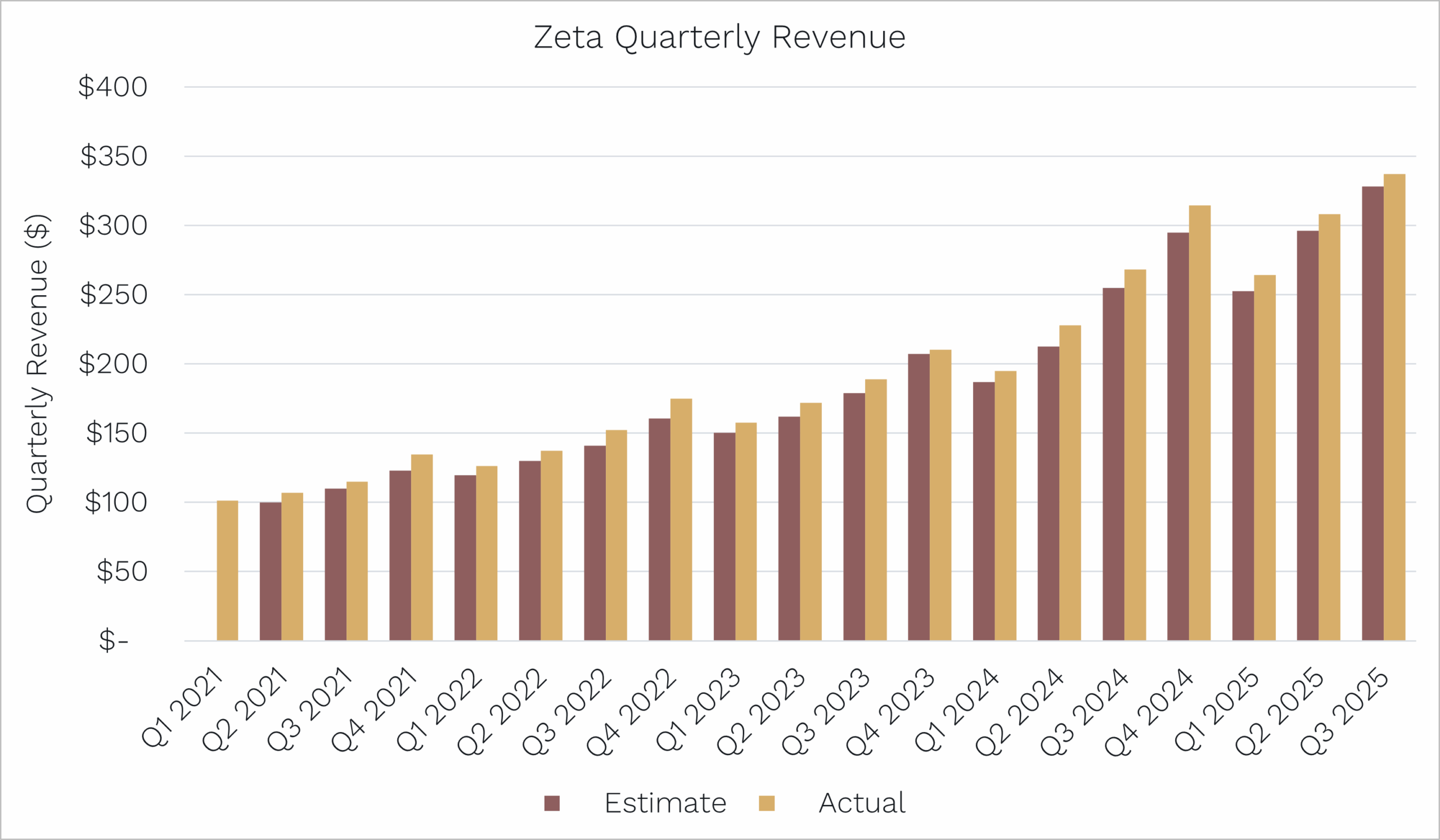

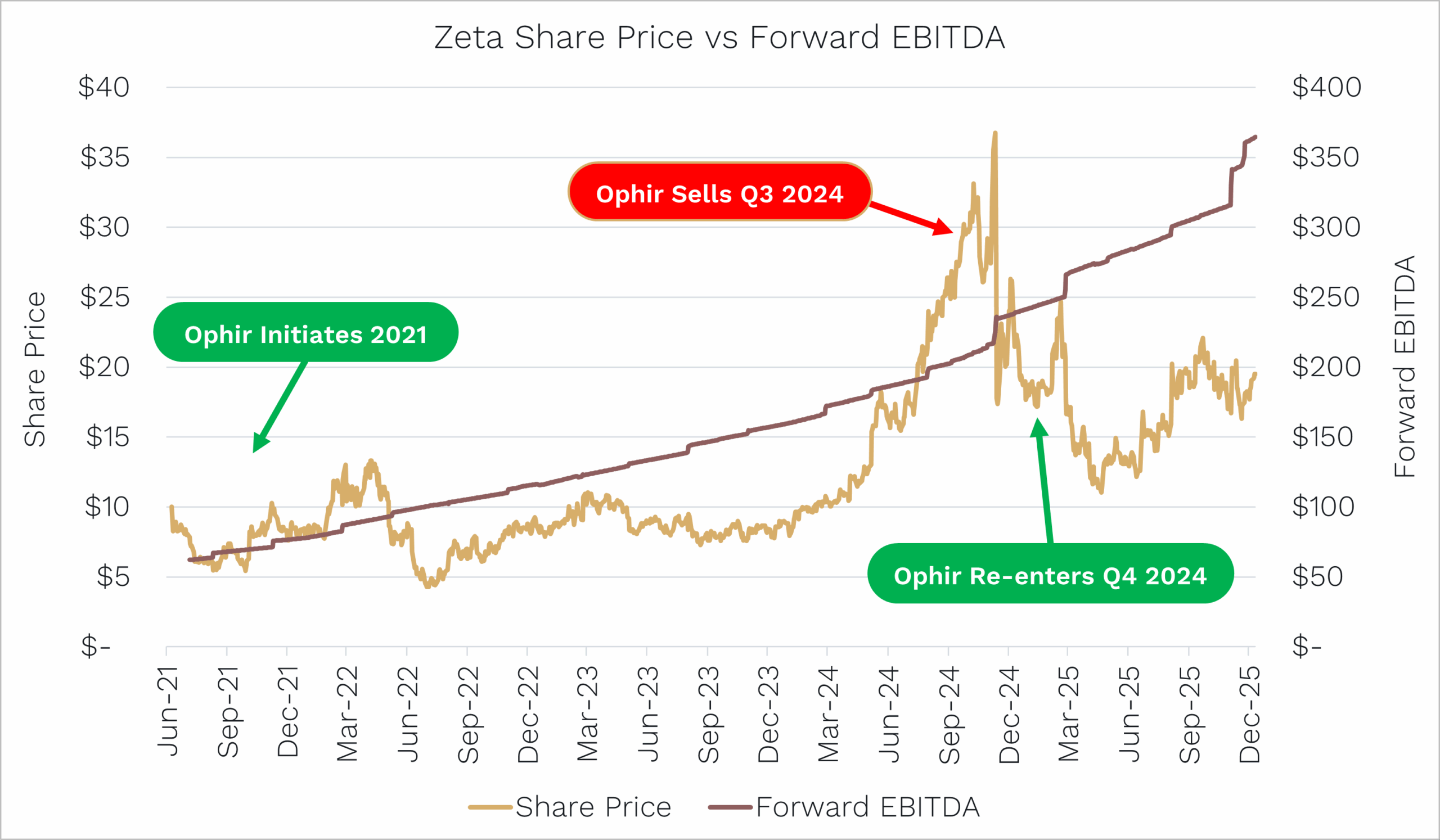

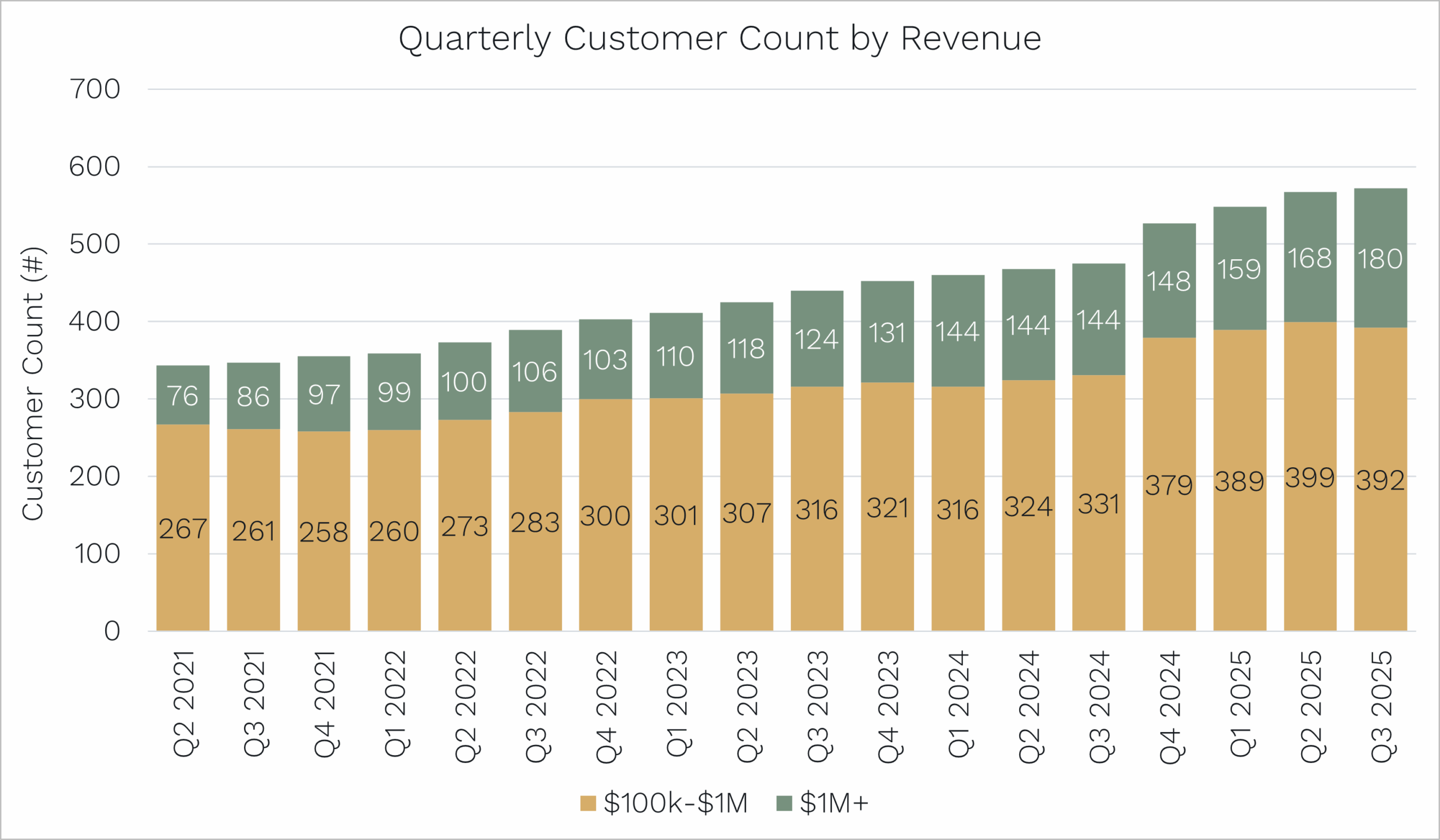

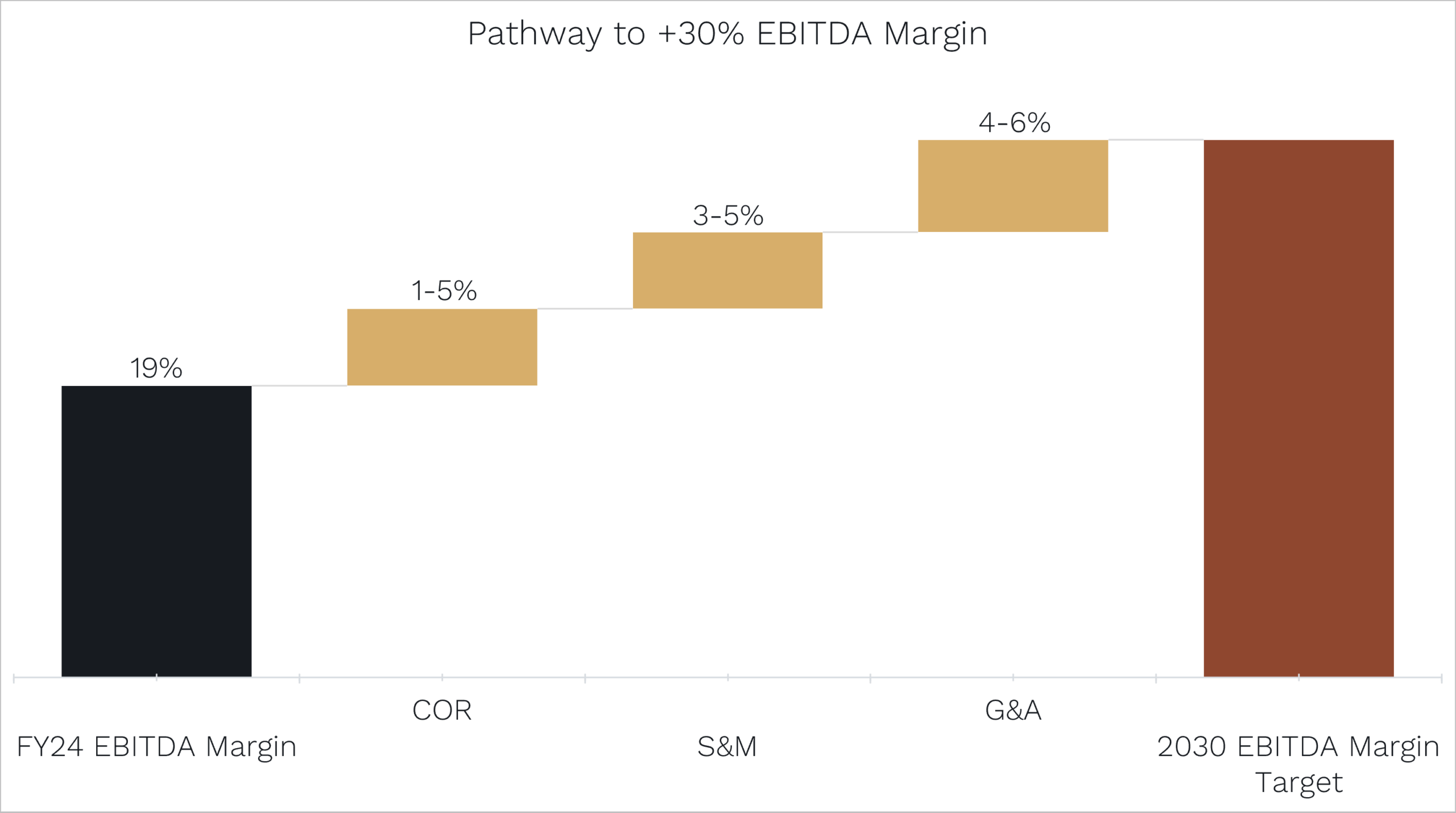

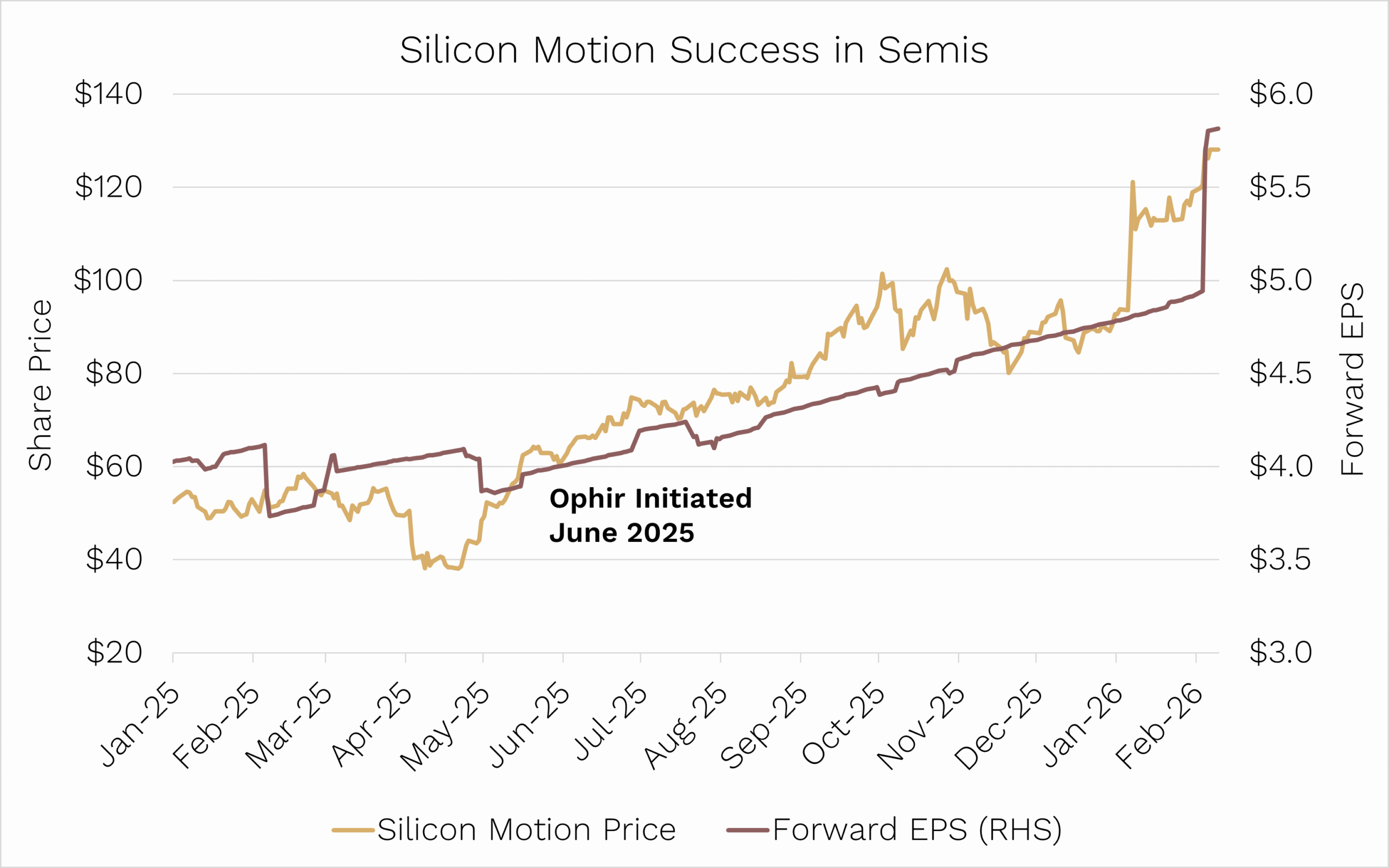

Silicon Motion Technology Corp (Nasdaq: SIMO)

A key holding for us in the storage space is Silicon Motion (SIMO), which performed strongly in January following CES.

The company is a global leader in the semiconductor industry, specifically acting as the ‘brains’ behind modern storage.

Silicon Motion is a ‘fabless’ company, which means they design the hardware and software but outsource the actual manufacturing to foundries like TSMC.

The company designs NAND flash controllers. A controller is a small processor that manages how data is stored, retrieved, and protected on NAND flash memory (the chips found in SSDs and smartphones).

Silicon Motion’s products are found in:

- Solid State Drives (SSDs): Used in PCs, laptops, and data centers.

- Mobile Storage: eMMC and UFS controllers used in smartphones and IoT devices.

- Specialty Solutions: Industrial-grade and automotive storage (e.g., in-vehicle infotainment and ADAS).

Source: Ophir. Bloomberg.

Managing Exposure Across the Stack

So how is Ophir playing this dynamic?

From our seat, this isn’t just about picking winners amidst an ever-shifting debate and material share price movements.

It’s about managing risk and not doubling down when stocks could de-rate further.

We believe in application-layer AI, but the market will take time to separate the winners and the survivors from the losers and the disrupted.

And while we remain exposed to some AI infra winners, we’re conscious that ‘earnings certainty’ trades rarely last forever as the market eventually overcapitalises future earnings and pays too high of a multiple.

While we will selectively invest in SaaS names that have cash flow support and have catalysts to reduce uncertainty, we won’t be relying on a recovery in software or a continuation of semi strength to drive future performance.