By Andrew Mitchell & Steven Ng

Co-founders and Senior Portfolio Managers

Our main focus during August and September is the Australian company reporting season which is both an exciting and restless time for us as investors.

Dear Fellow Investors,

Welcome to the July 2019 Ophir Letter to Investors – thank you for investing alongside us for the long term.

Month in review

Global equity markets were relatively subdued in July with the MSCI Developed Markets Index edging 0.5% higher. Despite many global equity markets hitting record highs during July including the S&P 500 and NASDAQ, the Federal Reserve cut interest rates for the first time in more than a decade reducing the benchmark by 25 basis points. The Fed was responding to fears of a slowing US and global economy as US President Trump’s trade wars start to take a toll. With central banks globally committing to more accommodative monetary policy and fixed income and cash offering very low rates of return, in our view equity markets will continue to benefit with money looking for yield and growth.

On local shores the S&P ASX 200 Accumulation Index rose 2.94% reaching an all-time high of 6845 on July 30 finally cracking its November 2007 high. This marks the 7th consecutive month of gains for the index which was fuelled by the RBA’s decision on July 2 to reduce the cash rate by a further 25 basis points to a new record low of 1.00% after also cutting by 25 basis points in June. Across the smaller company space, the ASX Small Ordinaries Accumulation Index climbed 4.5% in July helped by strong gains in the Materials and Information Technology sectors.

| 1 Month | 1 Year | 5 Year (p.a.) | Inception (p.a.) | Since Inception | |

| Ophir Opportunities Fund (Gross) | 4.7% | 21.3% | 24.0%p.a. | 33.7%p.a. | 664.1% |

| Benchmark* | 4.5% | 7.6% | 9.2%p.a. | 8.3%p.a. | 74.3% |

| Gross Value Add | 0.2% | 13.7% | 14.8%p.a. | 25.5%p.a. | 589.8% |

| Ophir Opportunities Fund (Net) | 4.6% | 17.5% | 19.6%p.a. | 25.4%p.a. | 426.5% |

* S&P/ASX Small Ordinaries Accumulation Index (XSOAI)

| 1 Month | 1 Year | 3 Year(p.a.) | Inception (p.a.) | Since Inception | |||||

| Ophir High Conviction Fund (Gross) | 6.7% | 15.5% | 16.0%p.a. | 27.0%p.a. | 160.1% | ||||

| Benchmark* | 4.7% | 7.5% | 10.1%p.a. | 12.9%p.a. | 62.4% | ||||

| Gross Value Add | 2.0% | 8.0% | 5.9%p.a. | 14.1%p.a. | 97.7% | ||||

| Ophir High Conviction Fund (Net) | 6.3% | 12.8% | 13.4%p.a. | 22.1%p.a. | 122.2% | ||||

| ASX:OPH Share Price Return | 4.8% | n/a | n/a | n/a | n/a | ||||

* 50% S&P/ASX Small Ordinaries Accumulation Index (XSOAI), 50% S&P/ASX Midcap 50 Accumulation Index (XMDAI)

The Ophir Opportunities Fund returned 4.6% after fees, outperforming the ASX Small Ordinaries Index by 0.1%.

The Ophir High Conviction Fund investment portfolio returned 6.3% after fees, outperforming its benchmark by 1.6%. The Ophir High Conviction share price returned 4.8% after fees, outperforming its benchmark by 0.1%.

Business update

We are delighted to announce that Michael Goltsman has joined our investment team as a Portfolio Manager. Michael joins us from London where he led the number one ranked Citi Global Investment Research European Small and Mid Cap team. We have known Michael for many years and rate him as one of the best stock picking analysts globally. Michael’s arrival further strengthens our investment team and importantly enhances our global perspective as Australian small and mid-cap companies increasingly seek growth offshore. We are excited that someone of Michael’s calibre has chosen to join Ophir.

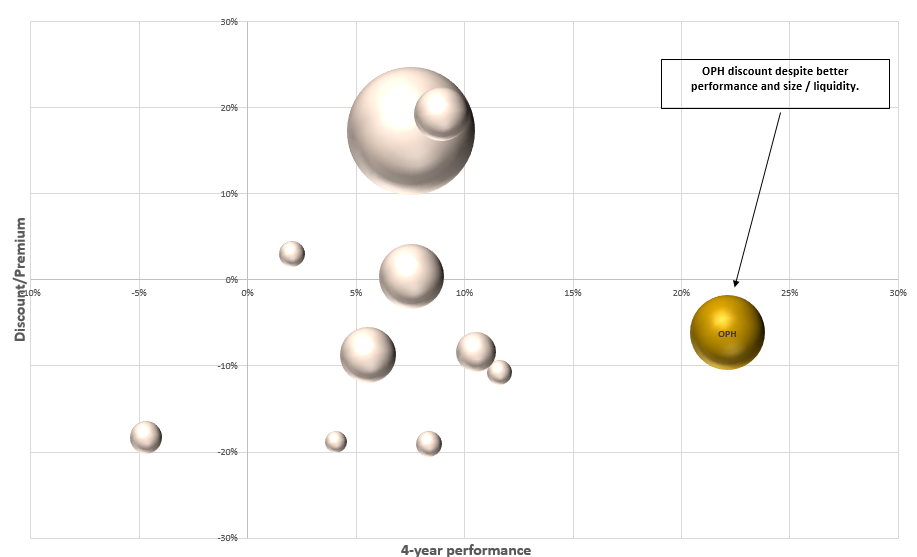

We remain pleased with the performance of the High Conviction Fund since listing on 18th December with the investment portfolio increasing by 28.8% and the share price increasing by 20.9% up until July 31. After trading at a premium for the first 3.5 months, we acknowledge the concerns of some investors that for the last 4 month it has traded at a discount. Whilst we would hope our investors will judge us over the long term, we would like existing investors to be able to liquidate their investment should they chose to at or around the NAV.

To drive further buying support for the Fund we have hired 2 x additional distribution resources to work alongside our Investment Director, George Chirakis. Alicia Cook joined during June as Investor Relations and Marketing Associate and a senior hire will be joining our distribution team in September to focus on increasing our engagement with financial advisers, a group that we have not largely engaged historically. Our experience to date is the discount to NAV has closed to around zero when we have engaged with advisers. We are hoping that by adding a dedicated resource to this channel we can close the current 4.5% discount (i.e. as at August 12).

Our analysis suggests that performance and size are key variables in ensuring strong demand for the units in the Fund. In our view the current discount represents a strong buying opportunity for investors given the Fund’s strong long term performance and size relative to its listed Australian small and mid-cap competitors. This is highlighted in Figure 1 below.

Previewing reporting season: Avoiding the downgrades

Our main focus during August and September is the Australian company reporting season which is both an exciting and restless time for us as investors. It is a crucial period which separates fact from fiction in terms of our portfolio companies’ prior 6 month earnings figures and future outlook.

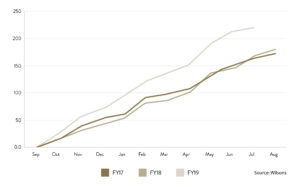

Whilst we remain confident that some of portfolio companies will beat market expectations, avoiding downgrades will be as, if not more, important during this reporting season. During the previous 3 months 76 ASX listed companies have issued earnings downgrades versus 19 upgrades. This 4:1 ratio is very high historically and suggests a tough reporting season lies ahead. Figure 2 outlines the rate at which downgrades during the previous 12 months have outpaced the equivalent period during 2016/17 and 2017/18.

We anticipate that downgrades will be a theme of the upcoming reporting season and over the next 12 months. This is because firstly, the Australian economy remains sluggish as a result of factors such as the housing downturn and tighter credit conditions. Secondly, the market’s expectations for growth are too high. For instance, the Small Industrials market is currently trading on 18x price to earnings one year forward and the market is expecting 9% growth for the coming year. We view this as overly optimistic. We believe that 5% growth is a more reasonable level.

We have observed these factors at play for some time and have been recycling capital out of companies exposed to the Australian economic cycle, positioning our portfolios to focus on those companies that can grow irrespective of economic conditions. As always, our focus has remained on companies that are winning market share in their relevant industry vertical and have a strong balance sheet to take advantage of any opportunity that presents itself. For these reasons we enter reporting season comfortable with the make-up of our portfolios.

A company we hold within the High Conviction Fund which displays all of these characteristics is ResMed (ASX:RMD). During our May Letter to Investors we outlined our investment thesis for ResMed and pleasingly on July 25 the company announced its fourth quarter and full year results revealing revenue growth of 15%.

This has been driven by its continued market share gains in the USA, particularly in its CPAP masks. Contributing factors include increasing product awareness by referrers and the company’s continued focus on resupply (i.e. patients reordering masks). While no specific details were provided on the performance of the company’s recent acquisition in the related Chronic Obstructive Pulmonary Disease market, it represents a significant longer term growth opportunity for the company to expand into new markets. Having invested over $1 billion on acquisitions in this area in the 2019 financial year, we will be closely monitoring the company’s progress and its strategy to earn a sufficient return on its investment. The company’s share price has risen by nearly 30% in the last 3 months and we continue to see a long runway for further growth.

We look forward to providing further updates on the performance of our portfolio companies during the upcoming reporting season.

As always, thank you for entrusting your capital with us.

Kindest regards,

Andrew Mitchell & Steven Ng

Co-Founders & Portfolio Managers

Ophir Asset Management

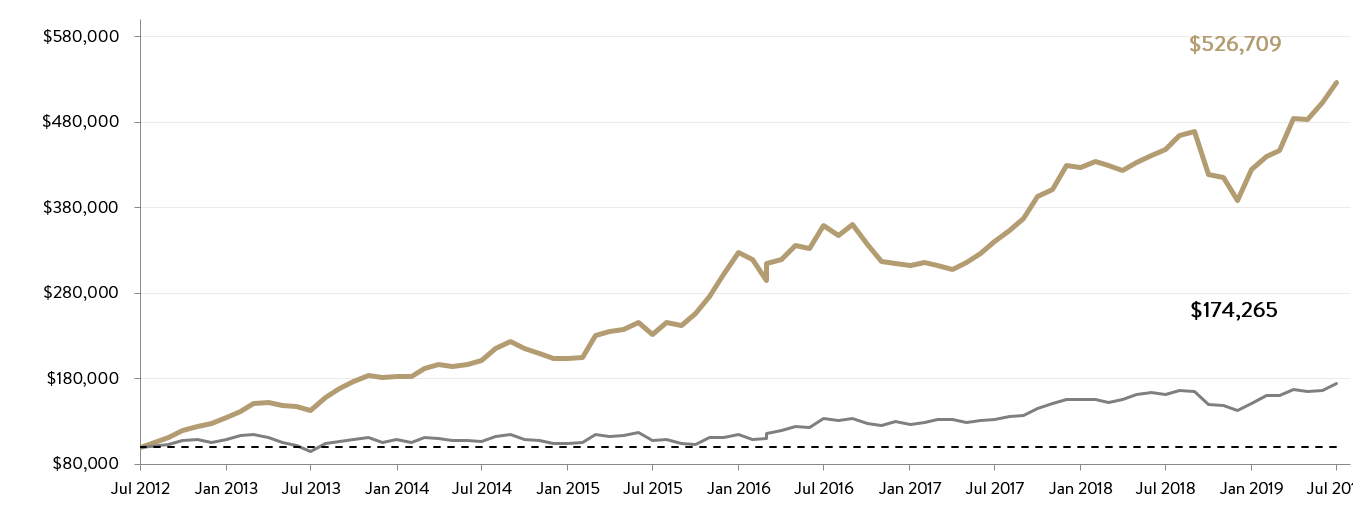

The Ophir Opportunities Fund

Growth of A$100,000 (after all fees) since Inception

The Ophir Opportunities Fund returned +4.6% for the month after fees, outperforming its benchmark by 0.1%. Since inception, the Fund has returned +26.8% per annum after fees, outperforming its benchmark by 18.5%.

| 1 Month | 1 Year | 5 Year (p.a.) | Inception (p.a.) | Since Inception | |

| Ophir Opportunities Fund (Gross) | 4.7% | 21.3% | 24.0%p.a. | 33.7%p.a. | 664.1% |

| Benchmark* | 4.5% | 7.6% | 9.2%p.a. | 8.3%p.a. | 74.3% |

| Gross Value Add | 0.2% | 13.7% | 14.8%p.a. | 25.5%p.a. | 589.8% |

| Ophir Opportunities Fund (Net) | 4.6% | 17.5% | 19.6%p.a. | 25.4%p.a. | 426.5% |

* S&P/ASX Small Ordinaries Accumulation Index (XSOAI)

| Buy Price | Mid Price | Exit Price | |

| June 2019 Cum Unit Price – Opportunities Fund | 2.1649 | 2.1573 | 2.1498 |

Key contributors to the Opportunities Fund performance this month included Austal Limited (ASB), IMF Bentham Limited (IMF) and a2 Milk Company Ltd (A2M). Key detractors included Next Science Ltd (NXS), Integrated Research Limited (IRI) and Sundance Energy Australia Limited (SEA).

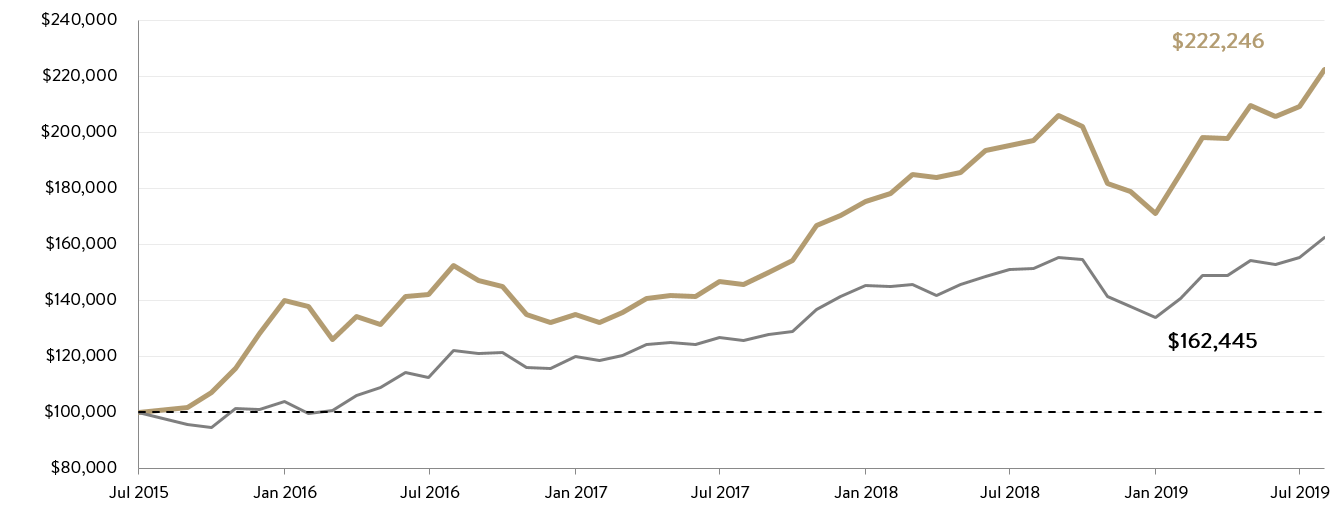

The Ophir High Conviction Fund

Growth of A$100,000 (after all fees) since Inception

The Ophir High Conviction Fund investment portfolio returned +6.3% for the month after fees, outperforming its benchmark by 1.6%. Since inception, the Fund’s investment portfolio has returned +22.1% per annum, outperforming its benchmark by 9.2% per annum. The Ophir High Conviction share price returned 4.8% after fees, outperforming its benchmark by 0.1%.

| 1 Month | 1 Year | 3 Year(p.a.) | Inception (p.a.) | Since Inception | |

| Ophir High Conviction Fund (Gross) | 6.7% | 15.5% | 16.0%p.a. | 27.0%p.a. | 160.1% |

| Benchmark* | 4.7% | 7.5% | 10.1%p.a. | 12.9%p.a. | 62.4% |

| Gross Value Add | 2.0% | 8.0% | 5.9%p.a. | 14.1%p.a. | 97.7% |

| Ophir High Conviction Fund (Net) | 6.3% | 12.8% | 13.4%p.a. | 22.1%p.a. | 122.2% |

| ASX:OPH Share Price Return | 4.8% | n/a | n/a | n/a | n/a |

* 50% S&P/ASX Small Ordinaries Accumulation Index (XSOAI), 50% S&P/ASX Midcap 50 Accumulation Index (XMDAI)

| 31 July 2019 NAV – ASX:OPH | $2.77 |

Key contributors to the High Conviction Fund performance this month included A2 Milk Company Ltd (A2M), Austal Limited (ASB) and Evolution Mining Ltd (EVN). Key detractors included Freedom Foods Group Limited (FNP), Seven Group Holdings Limited (SVW) and Contact Energy Limited (CEN).

This document is issued by Ophir Asset Management (AFSL 420 082) in relation to the Ophir Opportunities Fund & the Ophir High Conviction Fund (the Funds) and is intended for wholesale investors only. The information provided in this document is general information only and does not constitute investment or other advice. The content of this document does not constitute an offer or solicitation to subscribe for units in the Funds. Ophir Asset Management accepts no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. Any investment decision in connection with the Funds should only be made based on the information contained in the Information Memorandum and/or Product Disclosure Statements.